The economic releases of the past few days are putting the lie to the Keynesian escape velocity myth. The latter is not just around the corner—-and 2014 is now virtually certain to mark the fifth year running when the boom predicted by Wall Street economist at the beginning of the year fizzled as actual results unfolded.

In that context, yesterday’s punk number on personal consumption expenditures during May was the inflection point. Not only did American consumers not come bounding out of their winter ice caves as predicted by virtually every “sell side” economist, the number actually embodied a case of groundhog economics. That is, the May constant dollar PCE (personal consumption expenditure) print of $10.881 trillion suggested that consumers went back into hibernation! It was nearly the same as that during frigid February and actually below the March level of $10.916 trillion. Stated differently, the American consumer is dropping, not shopping, and the winter weather—-that surprising thing called snow and cold—had nothing to do with it.

So this is the time to call out the Wall Street amen chorus. Its impudent insistence that the Fed’s mad money printing campaign is the magic elixir that will revive the main street economy has gone altogether too far.

In that context, a bubblevision guest on Wednesday dismissed the shocking Q1 GDP shrinkage as stale news that reflected events……well, 100 days ago! Only in a world were Wall Street stock peddlers masquerading as economists think the world turns on the weekly maneuvers and word clouds of the Fed could 100 days ago be considered irrelevant ancient history. But the young man in question—-one Dan Greenhaus, chief investment strategist of BTIG—-had an even more preposterous point. Based on the sentiment surveys and other factoids, he had divined that the negative Q1 number reflected January and February results and that the US economy had strongly rebounded in March.

In other words, he had done what amounted to an intra-quarter seasonal adjustment and explained away the following true facts. There have been 265 quarterly GDP prints since 1947; only 18 of these posted a number below the -2.9% recorded for Q1; and in only one of these 18 deeply down quarters was the US economy not in recession. To spot a four-week run rate of sunshine economics hidden in that 13-week stretch of badly slumping activity is surely evidence of too much time at the Kool-Aid dispenser.

Here is the more sober take on the matter. After two months, Q2 real PCE is running at $10.889 trillion, and is therefore clocking in at a 1.2% annualized rate of gain on Q1. Moreover, even if June’s nominal PCE prints at a 0.8% monthly gain—-a rate that has not been realized in years—-Q2 real PCE would still come in well below 2%. And since the Keynesian case requires consumers to come screaming out of the blocks pulling the 70% of GDP accounted for by PCE behind them, the distinct possibility exists that Q2 results will come in below 3%. That means that by mid-2014 the US economy will have barely attained the level posted for Q4 2013.

After all, there are no signs that the other components of Q2 GDP are on any kind of tear. Housing starts are actually below Q1 after two months. Likewise, real fixed business investment has been decelerating over the last few quarters—and there is no indication of a reversal. Likewise, quarter-to-date global trade data offer no hope of a sudden boom in US exports; nor has there been any evident acceleration of government sector consumption and investment. Even if inventory accumulation picks up, there are only three quarters in the last 45 that have added more than 2.0% to the quarterly GDP print.

The truth is, the “consumer is back” narrative is getting pretty tiresome because it is belied by the facts. The May print, for example, reflected only a 1.8% real PCE gain over May 2013. And delving further back into the so-called recovery, it is obvious that real consumer spending growth has been decelerating, not fixing to explode. Thus, the Y/Y gain in May 2013 was 1.9%, and that compared to 2.4% the prior year, and 2.6% the year before that (i.e. the years ending in May 2010). Overall, real PCE has expanded at a only a 1.2% annual rate since its cyclical peak in the spring of 2008.

![]()

That trend rate is in the sub-basement of modern history. During the prior six-year cycle, for example, real PCE had expanded at a 2.5% rate from the October 2001 peak—or by more than double the rate of the current cycle.

![]()

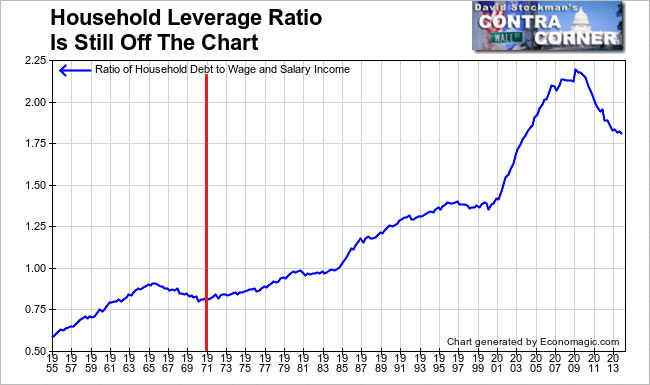

Moreover, the latter had the benefit of the Fed’s last push of US households into the stratosphere of peak debt. And it cannot be emphasized enough that era is over. Real PCE growth, therefore, is a function of wage and salary income growth, and it is evident that that latter is not happening. Indeed, the Fed’s wealth effects policy is undoubtedly having a perverse effect. Corporate boards and CEOs are being rewarded for stock buybacks and restructuring charges. So they borrow more and hire less.

The Household Leverage Ratio Is Still Off The Charts – Click to enlarge

The truth of the matter is that we are now living on borrowed time. Shortly, we will enter month 61 of the current so-called recovery, meaning that the present cycle is already long-in-the-tooth compared to the 55 months average of 10 cycles since 1949. Yet there are two headwinds that the Kool-Aid drinkers constantly deny.

First, even CPI inflation is back in the two percent zone and possibly accelerating. That means that real wage and salary incomes are stalling, as is now the case on a year-on-year basis.

Secondly, even the tepid recovery of PCE that we have had—-was achieved at the expense of drawing down the household savings rate to nearly rock-bottom levels, as shown below. Why in the world do Keynesians think that an aging population will defer saving for retirement indefinitely? More importantly, why would monetary policy be designed to punish savers with zero deposit rates for seven years running?

![]()

The answer is self-evident. The Wall Street hockey sticks are designed to elicit bullish impulses on main street. Zero interest rates are designed to prop-up risk asset markets—-so that the sheep can once again be led to the slaughter.