“

Well, that didn’t take long to come to fruition.

In this past weekend’s commentary, I discussed the likelihood of Central Banker’s leaping into action to stabilize the financial markets following the British referendum to leave the E.U. To wit:

“Of course, the reality is that we will likely see a globally coordinated Central Bank response to the financial markets over the next few days if the selling pressure picks up steam. This will come in the form of:

- Further interest rate reductions

- Deeper moves into negative rate territories

- Increased/accelerate bond purchases by the ECB

- A potential short-term QE program by the Federal Reserve

- A pick up of direct equity/bond buying by the BOJ.

- Liquidity supports through FX swaps or direct intervention

- Lot’s and Lot’s of “Verbal Easing”

Not to be disappointed, Mario Draghi sprung into action on Tuesday suggesting a greater alignment of policies globally to mitigate the spillover risks from ultra-loose monetary measures.

“We can benefit from the alignment of policies. What I mean by alignment is a shared diagnosis of the root causes of the challenges that affect us all; and a shared commitment to found our domestic policies on that diagnosis.” – Mario Draghi at the ECB Forum in Sintra, Portugal.

Furthermore, as noted by John Plassard, a senior equity-sales trader in Geneva at Mirabaud Securities via Bloomberg:

“Stocks are rebounding on the expectation that there will be a coordinated intervention by central banks. What central banks can do is put confidence back in the market by telling everyone that they are here and ready to act. If we don’t get that sort of support, we’ll see further declines.”

What Do They Know?

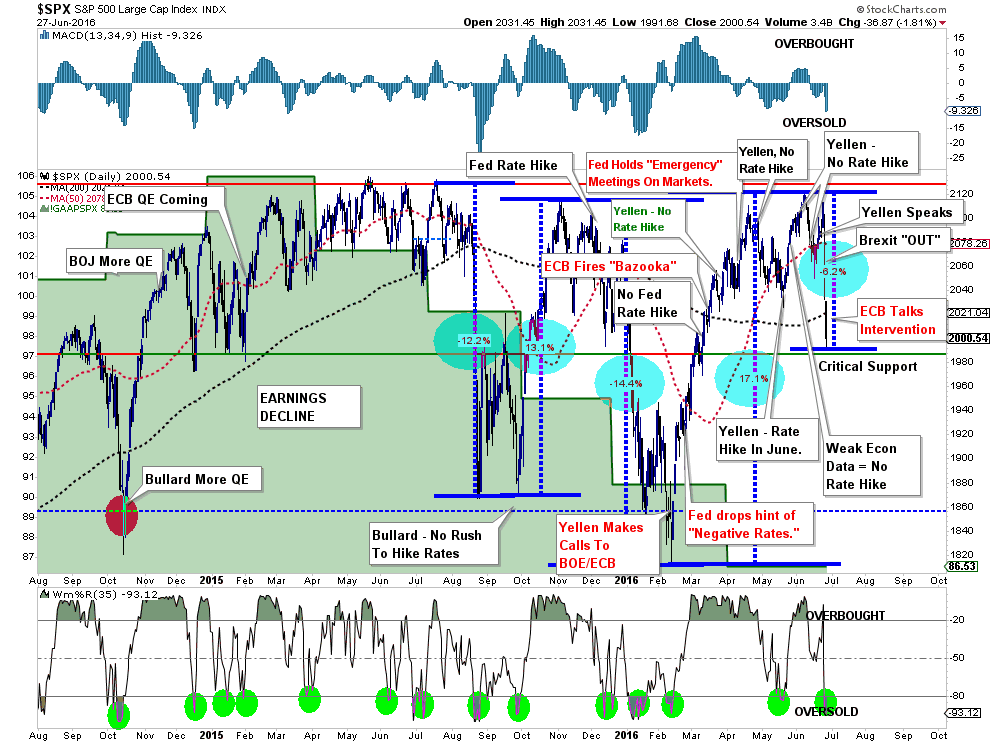

While I am not surprised by global Central Banker’s rush to action, it is important to keep things in perspective. Take a look at the chart below.

The highlighted blue circles are what I want you to focus on.

Since the end of QE3 in October of 2014, the markets have made little real progress despite a marked pickup in price volatility. Almost like clockwork, as the markets approach short-term “oversold” conditions the market reverses course and rises back to “overbought” levels before the next decline. Tick. Tock.

Against a backdrop of weakening fundamentals and economic data, the markets have drifted from one Central Bank action to the next. As shown above, the drop last summer of -12.2% spurred Fed members to assure markets there was no rush to hike interest rates. The “relief rally” that ensued drove markets higher by 13.1% only to be tripped up by the rate hike Bullard said the Fed was in no rush to do.

The tightening of monetary accommodation, and threats of four more in 2016, led to a rebalancing of risk at the beginning of 2016 and a decline of -14.4%. That decline spurred the Fed in February to coordinate with the ECB and BOE to coordinate monetary support, combined with the coming ECB’s monetary “bazooka” in March that drove markets higher by 17.1%.

Despite the increased size of advances and declines, each rally and decline remain confined within the continuing range of October 2014 lows and the May 2015 highs.

Here is the point. It took previous declines in excess of 10% before global Central Banks took action to support prices. Following the “Brexit,” it only took a -6.2% decline before Central Banks went to work.

The “invisible hand” of Central Bank interventions has been clearly evident since the end of QE3. With global interest running at, or below, the zero bound, there are few policy tools available to support already anemic economic growth.

The question that should be asked is “what do they know that we don’t?”

Technical Deterioration

Stepping back from the fundamental/Central Bank discussion for a moment, a look at recent price action denotes an increased risk for investors currently. This past weekend, (subscribe for FREE E-delivery) I laid out critical support levels and actions to take:

“While I stated above that you should ‘do nothing’ over the next day or two until the initial ‘panic’ subsides, it is prudent that over the next few days you continue to take prudent portfolio and risk mitigation actions.

Continue with the steps laid out in the “Monday Morning Call” Section a couple of weeks ago:

- Tighten up stop-loss levels to current support levels for each position.

- Hedge portfolios against major market declines.

- Take profits in positions that have been big winners

- Sell laggards and losers

- Raise cash and rebalance portfolios to target weightings.

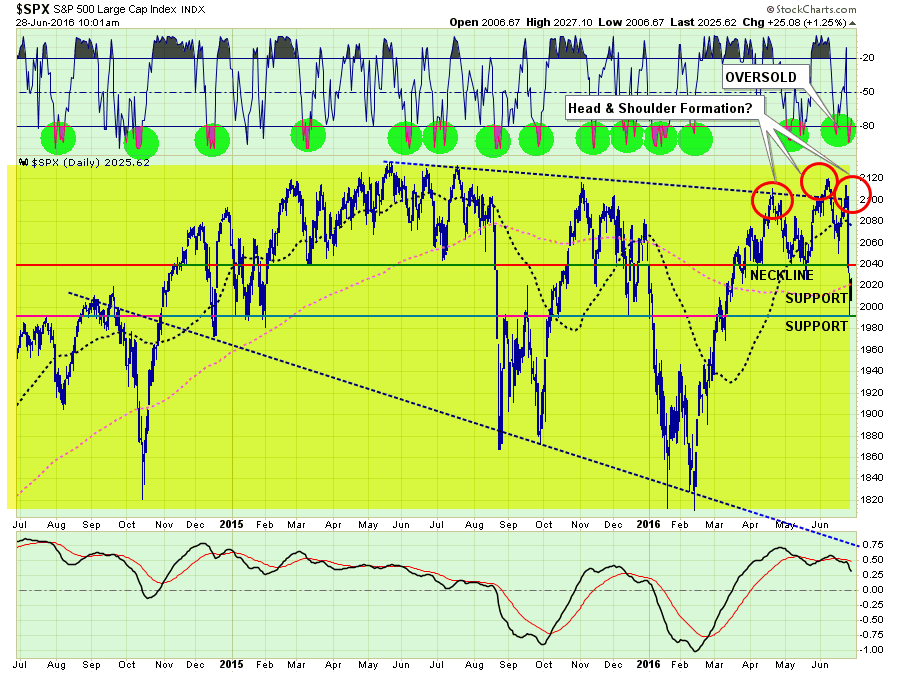

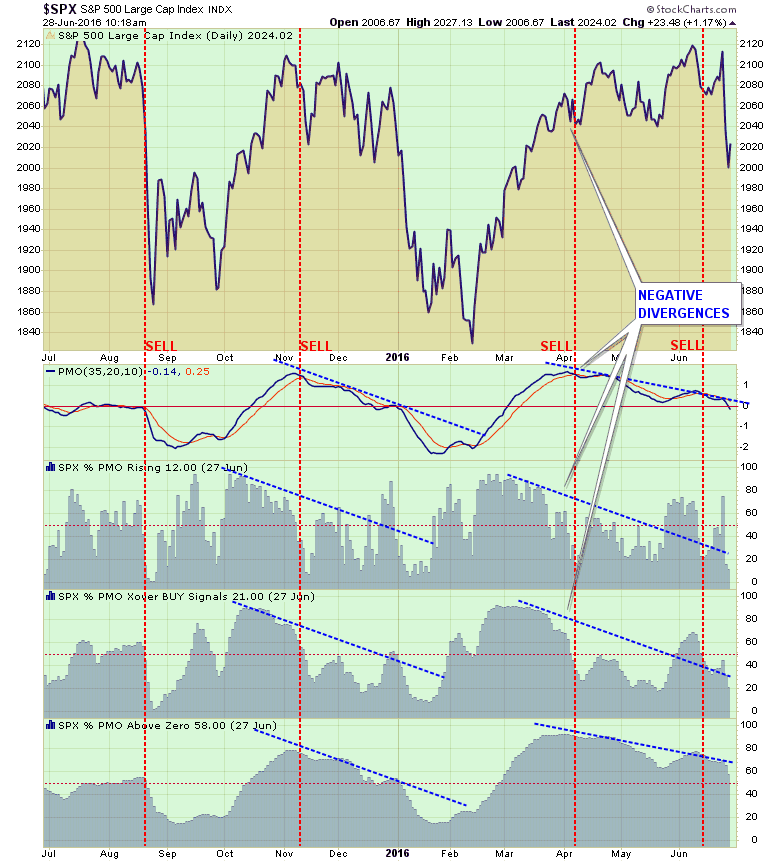

Importantly, two things have currently occurred worth paying close attention to. The “head and shoulder” technical formation on a short-term basis has now been violated.

With the market oversold on a short-term basis, the rally today was not unexpected. However, with “sell signals” in place and neckline support at 2040 now violated, the downside risk currently outweighs the reward. Therefore, the recommendations to rebalance and reduce risk remain intact for this rally.

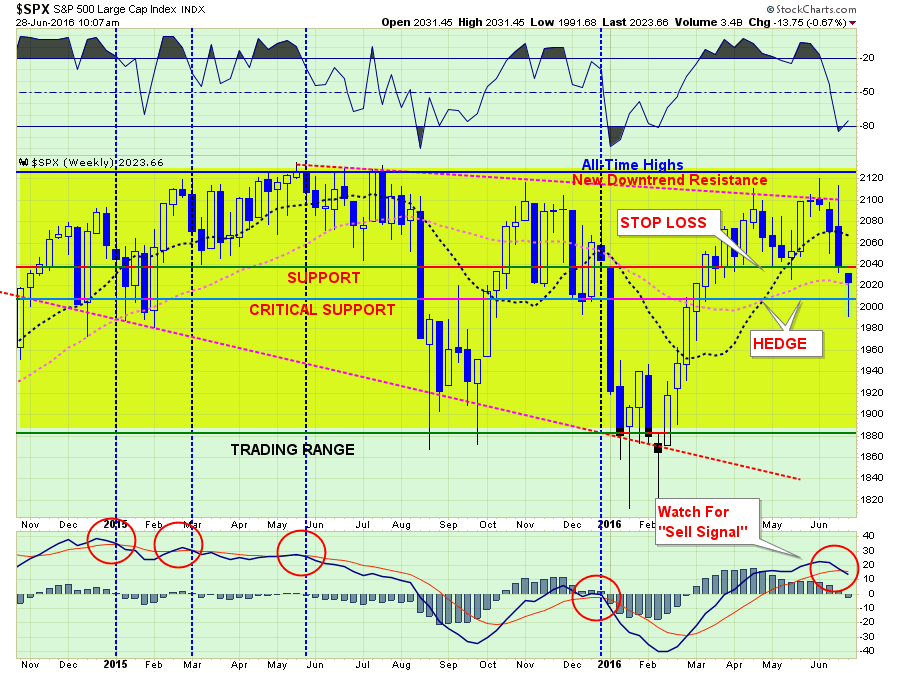

From a portfolio management perspective, I use WEEKLY price charts to reduce the day to day volatility of market swings to reduce the occurrence of “head fakes” and portfolio turnover. As shown in the weekly price chart below, the markets are currently holding support at the intermediate-term moving average. While stop loss levels were violated on Monday, we will now use any subsequent rally to reduce equity risk by following the rules above. However, with the market holding support currently, negative hedges will remain on hold for now. Where the market finishes on Friday will determine the next set of actions.

Lastly, and importantly, it is worth noting that price momentum has turned decisively negative against a backdrop of negative divergences from the index itself. Historically, when momentum declines as prices rise, the outcome for investors have been less than favorable. The chart below shows several variations of price momentum and the previous outcome of the negative divergence.

While the markets are bouncing today, caution is highly warranted. This is likely NOT a “buy the dip” opportunity as bond yields are currently unchanged.

The next few days will begin to “tell the tale.” Importantly, however, the ongoing disregard for underlying fundamentals is something that has only been witnessed at major market peaks historically.

Furthermore, it is virtually assured the Federal Reserve will not hike rates now. In fact, the Fed will likely not hike rates at any point in 2016.

Here are the big risks I am watching going forward as money shifts from the instability of Europe to the “safety” of the U.S.

- International and Emerging Market performance will suffer relative to domestic markets.

- USD will strengthen from currency inflows.

- Bond prices will rise (interest rates will fall further)

- Oil prices will decline towards $30/bbl.

- Utilities, REIT’s, Healthcare, and Staples should outperform the S&P 500. (This just means they won’t decline as much as the index)

- Financials, Technology, Discretionary will lag as recessionary forces pick up steam.

- Imports / Exports will continue to suffer weighing on corporate profits (fuggeta’bout hockey stick earnings recovery.)

This is just some initial outlooks. I will continue to monitor and report on these specific areas each week from a price trend basis and make adjustments/recommendations accordingly.

Caution is highly advised.

“Better to preserve capital on the downside than outperform on the upside.” – William Lippman

Lance Roberts

Lance Roberts is a Chief Portfolio Strategist/Economist for Clarity Financial. He is also the host of “The Lance Roberts Show” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, and Linked-In