Japan has faded from the front page, but the economic disaster continues to bother. The Bank of Japan has been forced back from its first target “against” the “deflationary mindset” that launched QQE back in April 2013. The goal then was not to achieve 2% “inflation”, but rather a stable and sustained 2% rate. Needless to say, oil prices are not being helpful in that regard so the central bank is simply ignoring them for now (keeping QQE on its current expanded pace, but not adding) and reverting back to its “fingers crossed” strategy learned so well from the Federal Reserve (“transitory”).

Given the decline in oil prices, Kuroda has no choice but to adjust his timeframe, said Hideo Kumano, an economist at Dai-ichi Life Research Institute and a former BOJ official.

“Today’s comments suggest the two-year period isn’t as rigid as it was perceived to be in the market,” said Kumano. “The BOJ is unlikely to boost stimulus anytime soon.”

Nothing is “rigid” in the world of central banking and redistribution because the actual economy is not a regression equation. When QQE was announced, the Bank of Japan actually stated the two-year horizon as a benchmark:

The Bank will achieve the price stability target of 2 percent in terms of the year-on-year rate of change in the consumer price index (CPI) at the earliest possible time, with a time horizon of about two years.

Some will argue that the inclusion of the word “about” softens the failure but the fact that the Bank’s own economists now expect full and sustained “inflation” by April 2016 instead (+2.2% the current projection, FWIW) is a definite miss to expectations. That would include the language in that statement that sounded an awful lot like exuded confidence in the abilities of redistribution: “earliest possible time” makes it sound like the 2-year standard is the latest of expectations. However, like the ECB, the lack of meeting one’s own inflation target is an indication of simple theory not suitable for realistic complexity.

It was also posited, quite assuredly, that the export sector would be the leading edge of positive redistribution (as if such a thing existed). The weakened yen was supposed to unequivocally re-orient the productive abilities of the Japanese export economy back toward something like its more glorious years before it all fell apart the first time in 1989. Koji Ishida, Member of the Policy Board at the BoJ, expressed exactly that position, which has been the official position throughout, in a speech he gave back in September 2013 only a few months after launch:

Japan’s economy is expected to continue a moderate recovery against the background of firm domestic demand and the pick-up in overseas economies. Specifically, exports are expected to increase moderately due to a gradual pick-up in overseas economies, mainly in the United States, and the definite, cumulative effects of developments in foreign exchange rates since last year.

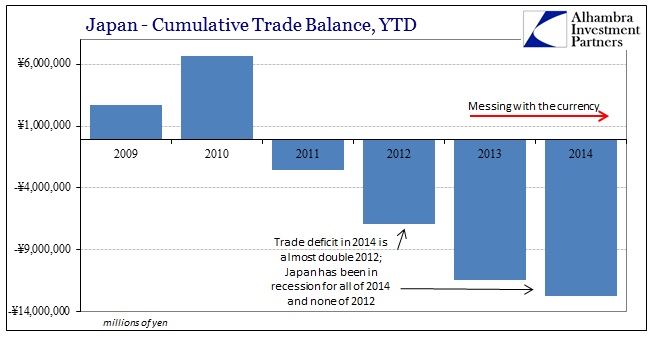

Outside of only nominal changes in local yen terms, exports haven’t done much of anything good toward reviving that “inflationary” trend (nor has the supposed pickup in the US – see below). Quite the opposite, as imports have failed to adjust with the currency, instead turning Japan’s trade balance into a nightmare of inefficiency. Only recently has the trade balance grown less disastrous, though that itself is simply confirmation of the same principle as that which is “delaying” the Bank of Japan meeting its inflation target: real economic decay.

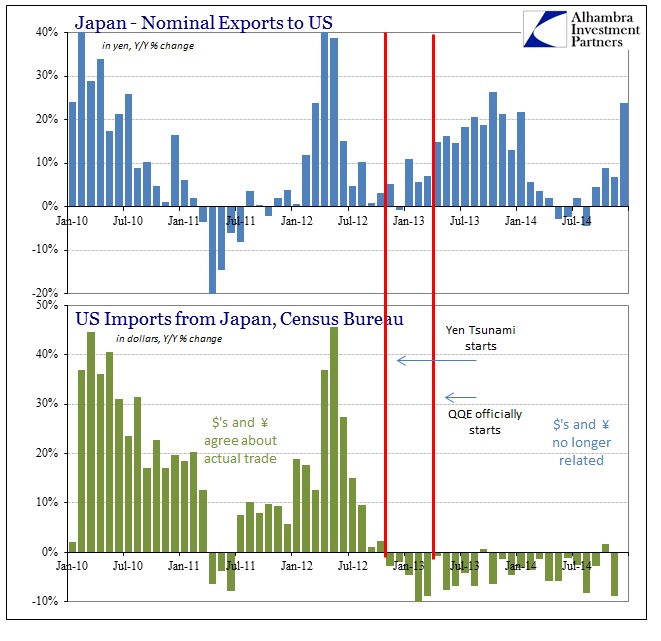

Exports to the US supposedly jumped nearly 24% in December from December 2013, but that doesn’t account for the almost 17% devaluation in the yen. Further, imports from the US to Japan increased by almost the same amount, +22.4%, suggesting that other factors are at work here. Instead, despite the increase in yen flowing for goods imported by the US, in actual dollar terms there is a consistent decline in good being received on this end. In other words, Japanese businesses get more revenue to produce fewer items (why would anyone hire more workers in that scenario?).

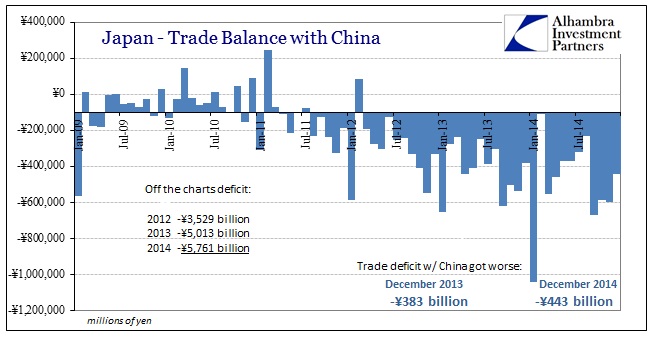

The same pattern was repeated with Chinese trade, an imbalance so persistent as to be a constant reminder of just how flawed redistribution theory can be taken. Instead of reviving Japanese productive capacity in the export sector, it has been productive capacity that continues to be “redistributed” out of Japan – with China as the main beneficiary so far.

Exports to China grew just 4.2% Y/Y, but imports increased almost 7%. The net result was a significant increase in the trade deficit with China in December in more monthly repetition. Given the dramatic decline in economic activity since the recession began, the continued expansion of the deficit with China shows just how durable the off-shoring has become under QQE.

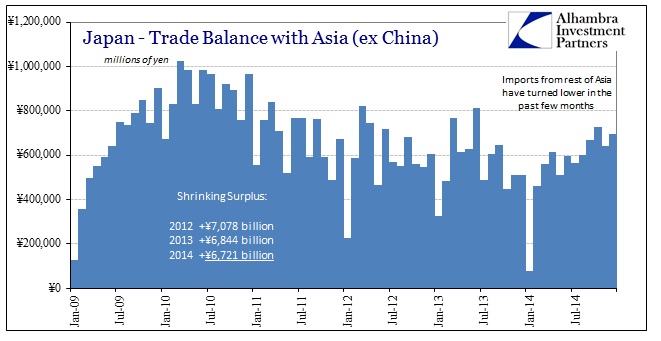

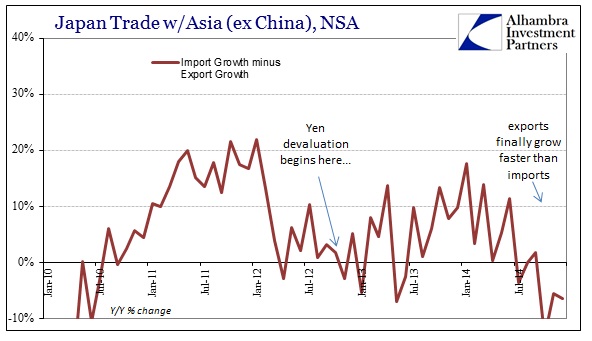

By contrast, the trade balance with the rest of Asia has improved, but only slightly. Imports have slacked in the second half of the year, and really since about October. That is both the price and the quantity of energy imported, which more than suggests that overall activity in Japan hasn’t found anything like a rebound into 2015 – just more changing of the benchmarks and standards that were once unquestioned and more than “realistic.”