What would we do without the Wall Street Journal? Do people actually pay for this lame-brained noise?

Retail Sales Surge as Consumers Rev Up Growth

Indicator Posts Best Monthly Growth Since September 2012

In fact, we are now entering the fifth season of head-fakes about “escape velocity” acceleration in as many years. Yet the Wall Street stock peddlers and their financial media echo boxes are so fixated on the latest “delta”—that is, ultra short-term “high frequency” data releases—that time and again they serve up noise, not meaningful economic signal. The former is perhaps good for a pre-open futures ramp by the algos upon the 8:30 AM headline release, but nearly useless as to the real direction of America’s struggling economy.

The WSJ headline writer quoted above might have at least noted the context in which the 1.1% seasonally mal-adjusted bounce for March was reported yesterday. It seems that even giving allowance to what the Fed believes to be the “insufficient” level of consumer inflation in recent months that the February starting point for yesterday’s report was down nearly 1% from its level last September. So when the winter storms are all said and done and the inflation adjusted retail number for March is published, it will be back to about $183 billion on the graph below—a level obtained around Columbus Day last fall. It’s a good thing summer’s coming!

![]()

The larger point here is that the Kool-Aid drinkers keep torturing the high frequency data because they are desperate for any sign that the Fed’s $3.5 trillion of QE has favorably impacted the Main Street economy. And that’s important not because it might mean some sorely needed income and job gains for middle America, but because its utterly necessary to validate the Fed’s financial bubble. Without “escape velocity” thru and sustainably above 3-3.5% GDP growth, there is no chance of a corporate earnings re-acceleration or the 20-30% gain in S&P 500 profits that are baked into the current forward PEs ($130 per share vs. reported LTM of $100).

{adinserter 1}Yet is it really not that hard to strain the noise out of the numbers. The starting point is to recognize that the Keynesian economists’ almost maniacal focus on monthly releases and quarterly GDP numbers has always been a giant mistake— and not only because they are so consistently and significantly revised after the fact owing to plugs, guesses and imputations in the early releases. The real problem is structural because quarterly GDP numbers are based on 90-day rates of “expenditure”. The latter contains huge oscillations in the economy’s inventory stocking and destocking function, and therefore can drastically mis-convey the underlying trends.

During the past 18 quarters for example, real inventory change has ranged from -$207 billion to +$127 billion, with points up and down the range during the interim. So a far more sensible use of even the flawed GDP data is to look at the year-over-year numbers for real final sales. That captures the trend and thereby filters out the four fake GDP accelerations that Wall Street has been gumming about since the end of the recession.

Here are the numbers. During the year ending in Q4 2010—the first year of “recovery”—real final sales expanded at a 2.0% rate. The next year there was no acceleration. Real final sales in the year ended in Q4 2011 was 1.8%—then it slightly bounced to 2.5% in 2012. And then, despite the initially reported big GDP acceleration in the second half of 2013, no such thing actually happened.

In fact, the four quarter gain in real final sales as of the most recent reporting on Q4 2013 was just 1.9%; and given the weak spending data already in for Q1 2014, its virtually certain to weaken even further during this quarter. In short, based on any reasonable and adult assessment of the numbers for the last 51 months, there has been no acceleration whatsoever. The economy is bumping along the bottom at 2% and that’s it.

Moreover, the problem with the 2% trend who’s name cannot be spoken is that it invalidates the entire bubble recovery scenario in which the inhabitants of the Eccles Building and their Wall Street overlords are completely invested. What has actually happened since the fall-winter 2008 crisis is that there was a drastic and unavoidable one-time liquidation of excess business inventories and phony jobs that had built-up during the Greenspan housing and credit bubble years, but that was nearly over by June 2009. This is documented in detail in Chapter 28 of my book, The Great Deformation (see pp 583-588, “The False Depression Call That Petrified Washington”).

Since then, the natural regenerative forces of our $17 trillion capitalist economy have been slowly inching output, income and employment forward at the aforementioned 2% rate— if you believe the official inflation data, and well less than that in reality. But the Fed’s massive money printing spree has nothing to do with it because the credit expansion channel of monetary policy transmission is broken and done.

As I have repeatedly mentioned, once “peak” business and household leverage ratio where reached in 2007-2008, the Fed’s massive liquidity injections operated almost exclusively through the Wall Street speculation channel. And that is exactly what has lead to forlorn quest for “escape velocity”.

The trailing 12 months reported EPS for the S&P 500 in Q4 2011 was about $90 per share, and today it is about $100. But while earnings have grown only 5%/year on a mechanical basis, and hardly at all after giving allowance to the massive, cheap-debt fueled stock buybacks in the interim, the broad market has bubbled upwards by more than 40%. In other words, its now extended out on the same peaks—about 19X trailing profits—that were obtained before the crashes of 2000-01 and 2008-09.

Nevertheless, the Wall Street talking heads can’t help themselves with the constant ridiculous refrain that the consumer is back, and its soon off the races:

The linchpin of economic growth, the consumer, is back,” said Chris Rupkey, chief financial economist at Bank of Tokyo-Mitsubishi.

Oh, really. Real wage and salary income is only 2% above its level 73 months ago when the economy last peaked. And after a salutary rebound in the savings rate during the Great Recession, the household savings rate has been drawn down to its unsustainable bubble lows. But pettifoggers like Rupkey just keep pouring the Kool-Aid.

So the Fed sponsored Wall Street bubble inflates to its final asymptote. When the inevitable bust occurs, it will trigger a sharp retrenchment in business inventories, investment and consumer spending, but the usual suspects will say its time to restart the Keynesian Clock. That being the one that is now permanently broken but never acknowledged by our rulers in the Wall Street-Washington corridor— who long ago threw sound money and the laws of economics to the winds in a desperate attempt to hang on to ill-gotten power and wealth.

![]()

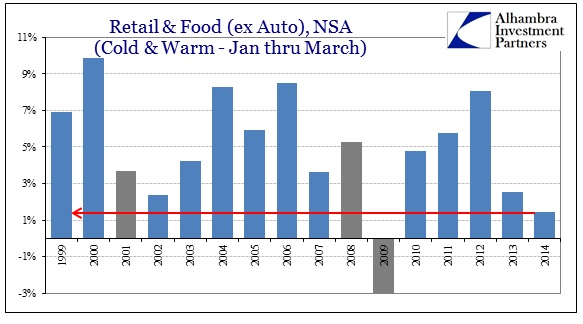

In any event, in today’s post by Jeffrey Snider, it is evident that we just had winter; that the three month retail spending average including the ballyhooed March bounce was the second weakest of this century, and that the fifth annual spring time leap into “escape velocity” is nowhere in sight.