“

Biggest Rallies Occur In Bear Markets

As expected, the market was oversold enough going into last Friday to elicit a short-term reflexive bounce. Not surprisingly, it wasn’t long before the “bulls” jumped back in proclaiming the correction was over.

If it were only that simple.

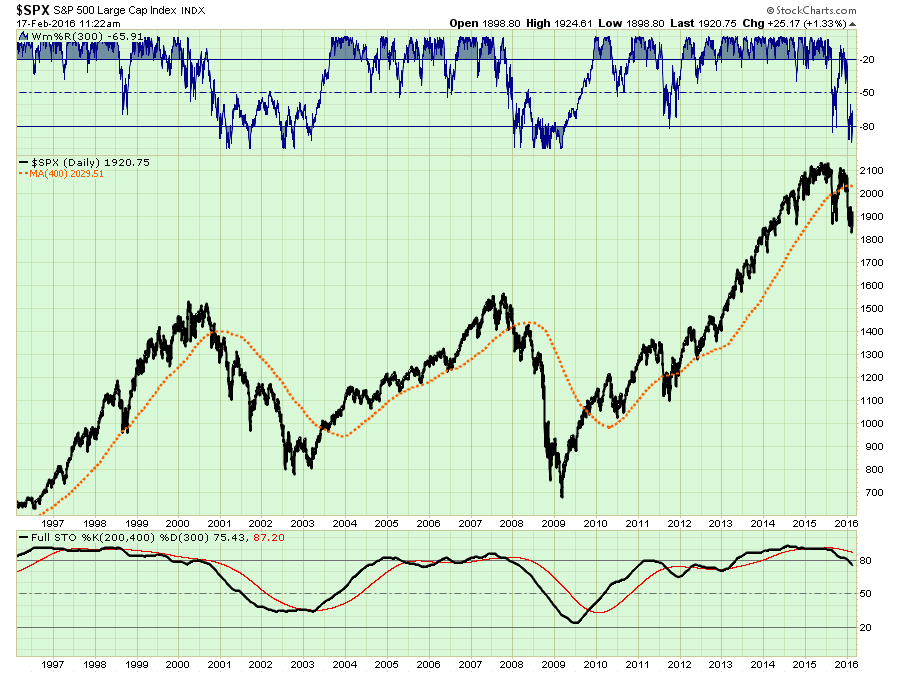

First, as I have discussed in the past, market prices remain in a “trend” until something causes that trend to change. This can be most easily seen by looking at a chart of the S&P 500 as compared to its 400-day moving average.

As you will notice in the main body of the chart, during bull markets, prices tend to remain ABOVE the 400-dma (orange-dashed line). Conversely, during bear markets, prices tend to remain BELOW the 400-dma.

The one event in 2011, where all indicators suggested the market was transitioning back into a bear market, was offset by the Federal Reserve’s intervention of “Operation Twist” and eventually QE-3.

During cyclical bear markets, bounces from short-term oversold conditions tend to be extreme. Just recently Price Action Lab blog posted a very good piece on the commonality of short-term rebounds during market downtrends:

“The S&P 500 gained 3.63% in the last two trading sessions. About 75% of back-to-back gains of more than 3.62% have occurred along downtrends. Therefore, a case for a bottom cannot be based solely on performance.”

“It may be seen that 73.85% back-to-back gains of more than 3.62% have occurred along downtrends, i.e., this performance is common when markets are falling. The sample size consists of 195 back-to-back returns greater than 3.62%.

Therefore, strong rebounds along a downtrend cannot be used to support a potential bottom formation.”

After a rough start to the new year, it is not surprising that many are hoping the selling is over.

Maybe it is.

But history suggests that one should not get too excited over bounces as long as the downtrend remains intact.

I Bought It For The Dividend

One of the arguments for “buy and hold” investing has long been “dividends.” The argument goes this way:

“It really doesn’t matter to me what the price of the company is, I just collect the dividend.”

While this certainly sounds logical, in reality, it has often turned into a very poor strategy, particularly during recessionary contractions.

A recent example was Kinder Morgan (KMI). In late-2014, as I was recommending that individuals begin to exit the energy sector, Kinder Morgan was trading around $40/share. The argument then was even if the share price of the company fell, the owner of the shares still got paid a great dividend.

Fast forward today and the price of the company has fallen to recent lows of $15/share (equating to a 62.5% loss in value) and the dividend was cut by 80%.

Two things happened to the investor’s original thesis. The first, was that after he had lost 50% of his capital, the dividend was no longer nearly as important. Confidence in the company eroded and the individual panic sold his ownership into the decline. Secondly, when a company gets into financial trouble, the first thing they will do is cut the dividend. Now you have lost your money and the dividend.

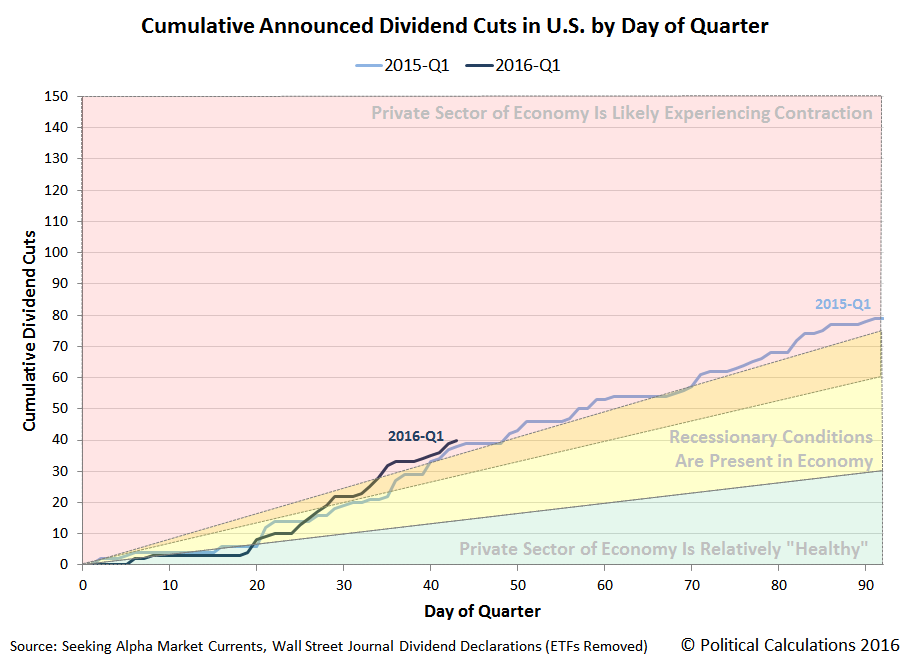

But it is not just KMI that has cut dividends as of late. Many companies have been doing the same to shore up internal cash flows. As pointed out recently by Political Calculations:

“Speaking of which, the pace of dividend cuts in the first quarter of 2016 has continued to escalate. Through Friday, 12 February 2016, the number of dividend cuts has risen into the “red zone” of our cumulative count of dividend cuts by day of quarter chart.”

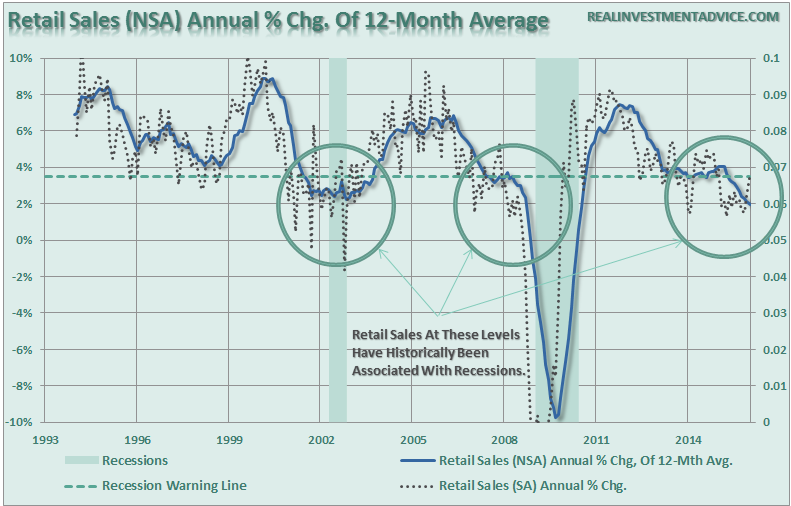

Importantly, while the media keeps rambling on that we are “nowhere” close to a recession, it is worth noting the following via NYT:

“The only year in recent history with more dividend cuts was 2009, when the world was staggering through a great financial crisis. A total of 527 companies trimmed dividends that year, Mr. Silverblatt’s data shows. Coca-Cola and other dividend-paying blue chips like IBM and McDonald’s were under severe stress in those days, too, but their financial resources were deep enough to allow them to keep the dividend stream fully flowing.”

Buying “dividend yielding” stocks is a great way to reduce portfolio volatility and create higher total returns over time. However, buying something just for the dividend, generally leads to disappointment when you lose your money AND the dividend. It happens…a lot.

Preservation of capital is first, everything else comes second.

Empathy For The Devil

Danielle DiMartino Booth, former Federal Reserve advisor and President of Money Strong, recently penned an excellent piece that has supported my long-held view on the fallacy of “consumer spending.” To wit:

“As for the strongest component of retail sales, it’s not only subprime loans that are behind the 6.9-percent growth in car sales over 2015. Super prime auto loan borrowers’ share of the pie is now on par with that of subprime borrowers – each now accounts for a fifth of car loan originations. What’s that, you say? Can’t afford that new set of wheels? Not to worry. Just lease. You’ll be in ample company — some 28 percent of last year’s car sales were made courtesy of leases, an all-time high. ”

What has been missed by the vast majority of mainstream economists is that in a country driven 68% by consumer spending, there are limits to that consumption. A consumer must produce (work) first to be paid a wage with which to consume with. Each dollar is finite in its ability to create economic growth via consumption. A dollar spent on a manufactured good has a greater multiplier effect on the economy than the same dollar spent on a service. Likewise, a dollar spent on a manufactured good or service has a greater economic impact than a dollar spent on paying taxes, higher healthcare insurance costs, or interest payments.

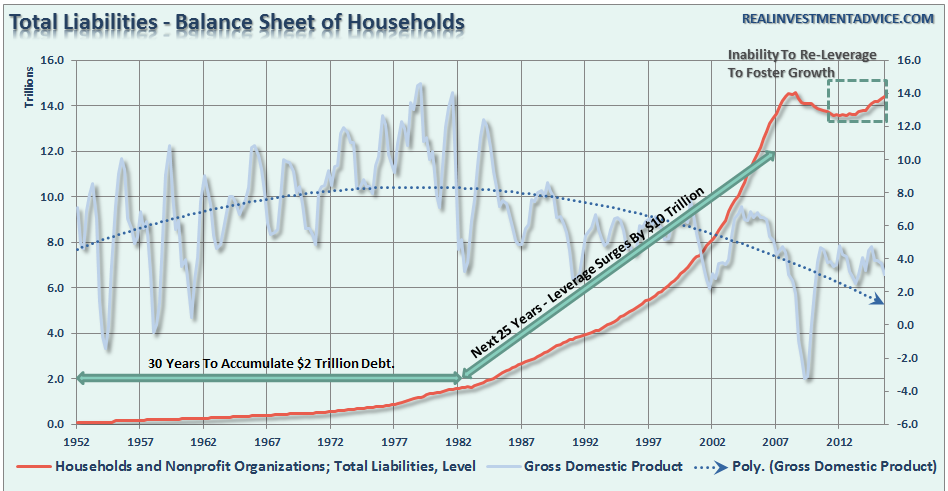

The only way to increase the level of spending above the rate of income is through leverage. However, rising debt levels also suggests more of the income generated by households is diverted to debt service and away from further consumption. The chart below shows the problem.

Over the 30-year period to 1982, households accumulated a total of $2 trillion in debt in an economy that was growing at an average rate of 8%. Wages grew as stronger consumption continued to push growth rates higher. Over the next 25-year period, households abandoned all fiscal responsibility and added over $10 trillion in debt as the struggle to create a higher living standard outpaced wage and economic growth. Since the turn of the century, average economic growth has been closer to 2%. See the problem here.

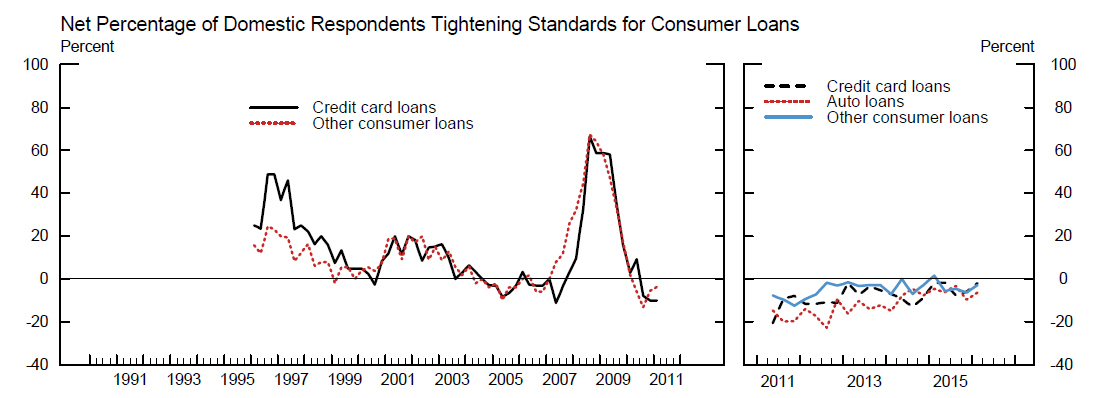

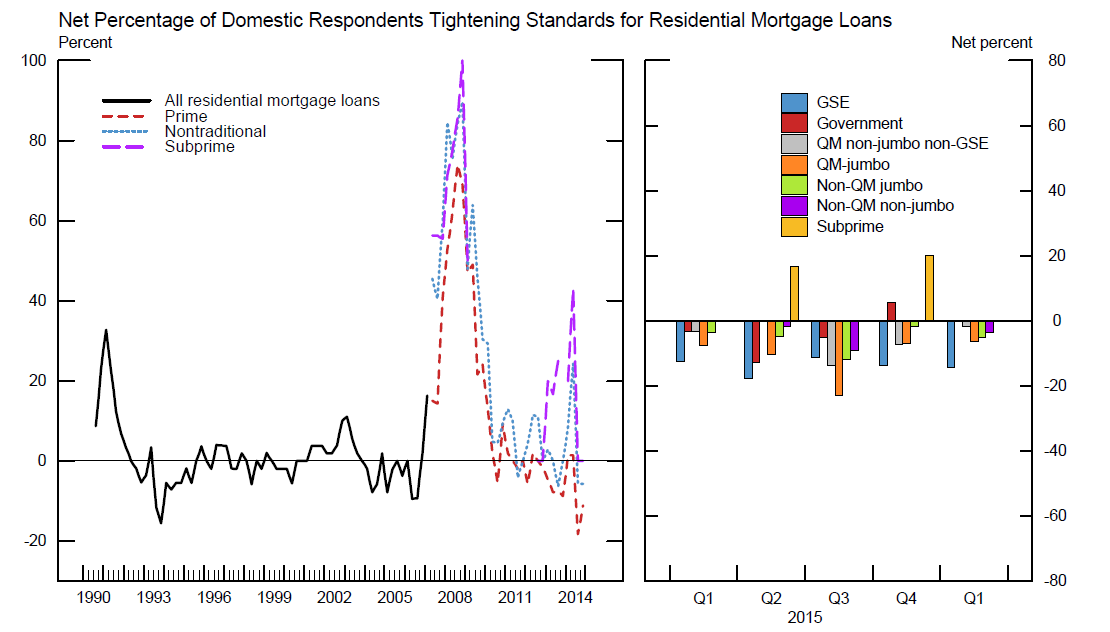

The bailouts following the financial crisis kept households from going through a much needed deleveraging. Likewise, since banks were taught they would be bailed out repeatedly for bad behavior, no lessons were learned there either. Not surprisingly, as shown by the recent Fed Reserve 2016 Loan Officer Opinion Survey, lending standards are now back to levels seen just prior to the financial crisis.

What could possibly going wrong? The problem is the consumer is all spent out and all leveraged up. While you shouldn’t count the consumer out, just don’t count on them too much.

Just some things to think about.

Lance Roberts

Lance Roberts is a Chief Portfolio Strategist/Economist for Clarity Financial. He is also the host of “The Lance Roberts Show” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, and Linked-In