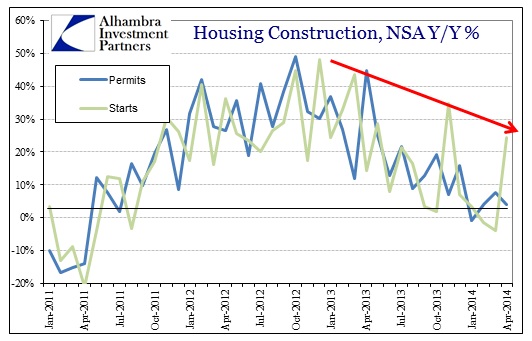

The latest home construction figures confirm both the durability of the downward trend and the theory that policymakers are getting nervous to the point of addressing it through additional measures.

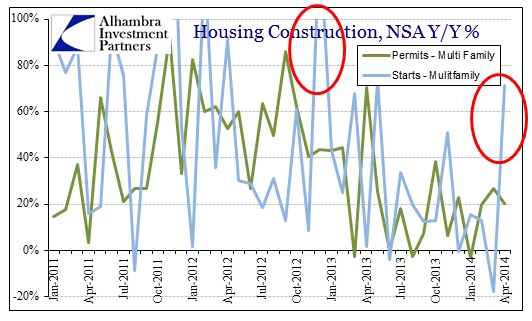

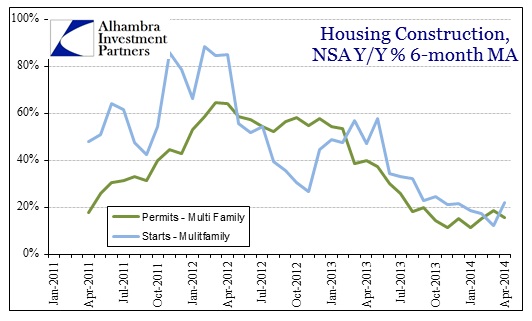

First, though, we need to sort out the noisy pieces. The data in multi-family construction is extremely volatile, so paying attention only to the month-to-month changes is highly misleading. The upward surge, particularly, in multi-family starts, is actually quite typical. What matters, ultimately, is the trend across several months that includes a full swing or short-term “cycle.”

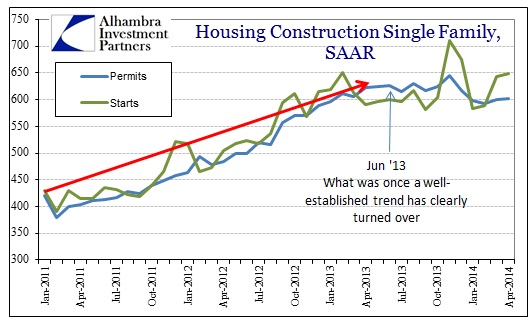

Overall starts in April surged, but only in the multi-family segments, while permits, the real leading indicator, continued to sink further. In terms of overall trend, despite the increase in starts, the rate is still below previous peaks in the volatility.

That short run instability in multi-family masks the growing deficiency in growth rates despite these impressive (in narrow isolation) figures.

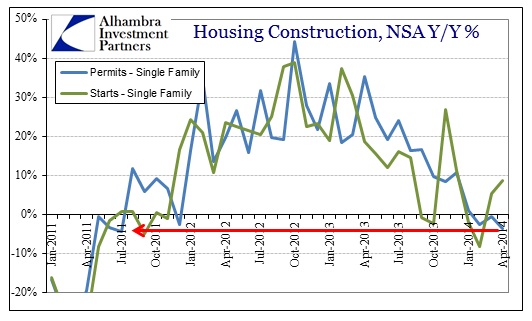

With that statistical noise aside, I think single family construction holds far more economic relevance. If the NAR-driven narrative of a shortage in homes is real and occurring, “explaining” the bubble-like rise in prices, then there should, again, be a rush to build more homes. Rising prices and a supply bottleneck is a producer’s dream situation as it amounts to a license to print profits. High demand and pricing power will always, absent a shortage of inputs, create fertile conditions for a supply surge.

It’s just not there – while starts have come up in the past few months, that is, once again, just normal volatility in the series amounting to a very clear trend of lower highs. Permits have actually contracted Y/Y for three consecutive months, with April being the worst showing since July 2011.

When you look at it from the standpoint of chronology, there is a very obvious inflection in early to mid-2013 that coincides with bubble-like price changes and then the drastic decline in mortgages. This would seem to confirm financial factors as a primary culprit, rather than the shortage idea. That is especially true since rising prices on the way up were “printed” via institutional cash purchases feeding back and apparently misleading construction signals – as if prices from institutional foreclosure auctions were indicative of actual demand for housing from people who want to live in a house (and can actually afford it). Instead, it looks pretty clear that the factors driving construction in 2011 and 2012, into early 2013, were nearly the same as those driving construction in the middle of the last decade.

This is, I believe, the evident corrosive nature of monetary intervention, where true price signals are co-opted in pursuit of economic control. In the chart immediately above, the left side moving in an almost straight line is the artificial part. The right side is the revelation of that through the apparent rejection of further resource misallocation – despite rising home prices builders are more than reluctant to build further. That has downstream impacts not just in construction, but sales and ultimately prices once again.

If there is a growing demand for multi-family, and I think that is the case relative to single family, it only reinforces the entrenchment of this misallocation as apartments will be needed longer term to house people that won’t be buying their own residences. That is unless the GSE’s can be successful at expanding mortgage leverage once more and attracting even more misallocation, though I think the downside is already becoming very plain.

Click here to sign up for our free weekly e-newsletter.

“Wealth preservation and accumulation through thoughtful investing.”

For information on Alhambra Investment Partners’ money management services and global portfolio approach to capital preservation, contact us at: jhudak@alhambrapartners.com