“

In this past weekend’s commentary, I discussed the failure of the market to hold its breakout above 2100 and the upcoming negative revisions to GDP. As of Friday, the market was flirting with breaking below important support at 2040.

However, Monday morning, that all changed. Over the weekend, the “Brexit” polls showed a surprising reversal as the “Leave” vote fell back to a neck-and-neck race with “Remain.” Of course, the primary concern for the markets over the last couple of weeks has been the impact of exit by Britain from the EU. (Which is arguably the best thing for them to do.) It all reminded me of the scene from “Breakfast at Tiffany’s:”

“Paul Varjak: Well, uh, [holds up ring from Cracker Jack box] We could have this engraved, couldn’t we? I think it would be very smart.

Tiffany’s salesman: [taking ring and examining it] This, I take it, was not purchased at Tiffany’s?

Paul Varjak: No, actually it was purchased concurrent with, uh, well, actually, came inside of… well, a box of Cracker Jack.

Tiffany’s salesman: I see…[continuing to look at ring] Do they still really have prizes in Cracker Jack boxes?

Paul Varjak: Oh yes.

Tiffany’s salesman: That’s nice to know… It gives one a feeling of solidarity, almost of continuity with the past, that sort of thing.”

Like the “ring in the cracker jack box,” the EU needs Britain much more than Britain needs the EU. For the EU, which is on the verge of self-destruction due to ongoing failed monetary policies, the need to maintain an image of “continuity” is critical. A recent Bloomberg Brief with billionaire Peter Hargreaves, the largest U.K. retail broker, with more than $84.1 billion equivalent in assets, crystallized this point.

“Every year in the EU it gets more political, it gets more legislative, more regulative; we don’t seem to get very much benefit from it. We will be far better out. The EU as an economic mark is declining in the world, when there were only nine countries in, it was 30 percent of the world’s GDP, now there are 28 it is only 17 percent. That’s some serious decline.

There’s a huge amount of vested interest, a lot people making these comments are politically motivated and also work for big banks that aren’t British. They’ve built these enormous dealing rooms and offices in the City of London and Canary Wharf and their bosses are saying we don’t want to endanger this huge investment of ours. I don’t think it will endanger that huge investment. You can’t move the City of London to anywhere else in Europe. It’s madness to suggest it. Frankfurt, the place everybody keeps talking about, only has a population of 700,000, it could not accommodate anything like the City of London.The City of London is absolutely guaranteed, it is bound to survive. The only center that could take over would be Zurich and that’s not in the EU either. It’s absolute drivel that the City of London will be affected. The City of London will go out and it will deal with these emerging economies in the Pacific Basin, Southeast Asia, Africa — they’re all going to want finance for different things. You can’t set up the City of London anywhere else. It takes years, and during that time the City of London will have grown.

The EU will disintegrate when we leave. They will realize there is nothing left. The political union is going to be a disaster and they’ll want a free-trade area. Do you know who’ll be the first country invited to that free trade area? The U.K.”

2100 Or Bust!

So, as I said, with the odds of “Brexit” swinging back strongly to the “Stay” camp, shares across the globe rallied Monday as the risk of an EU disruption seemingly fades.

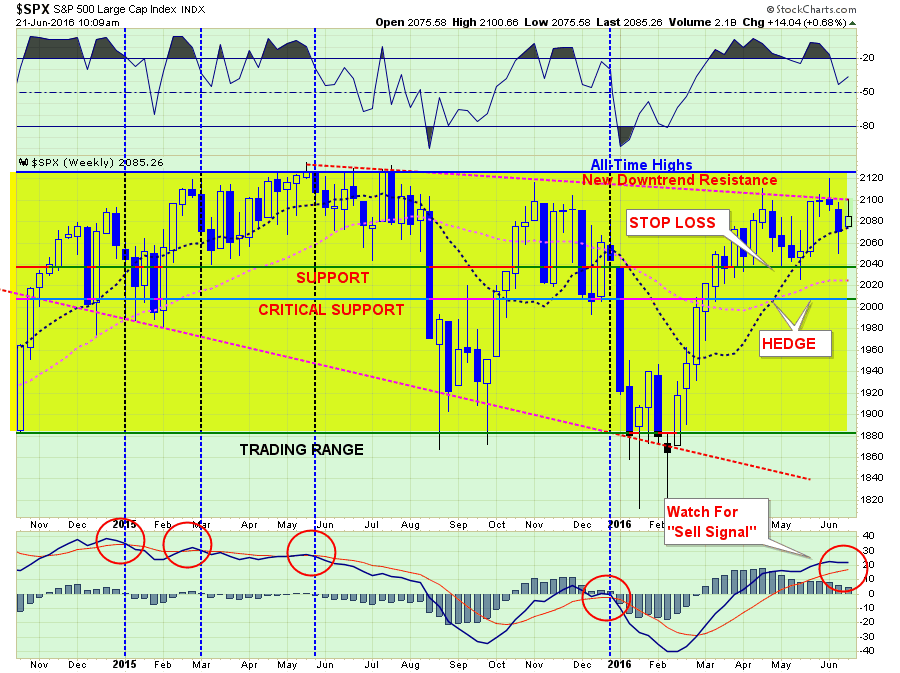

The immediate reaction for US stocks was to rally +1.4% out of the gate to retest 2100. Resistance proved formidable as hour by hour stocks handed back half of the gains to end the day at 2083.

The greater battle is still at the all-time highs at 2135, but we will deal with that resistance level when, and IF, we get there.

Of course, with Janet Yellen strolling up to Capitol Hill today for the beginning of the semi-annual Humphrey-Hawkins testimony, the markets will be glued to her comments for hints at continued “dovishness” with respect to monetary policy. As has been the case since the beginning of the year, the markets have migrated investment strategies to follow “Fed Speak” rather than fundamentals.

Of course, the market ignoring fundamentals and focusing on “Fed Speak” is not a new innovation but something seen at the peak of the last two major bull markets.

As I pointed out in this past weekend’s newsletter (subscribe for Free E-Delivery)

“As has been repeatedly been the case, with risk outweighing reward at the moment, a more cautious stance to portfolio management should be considered.

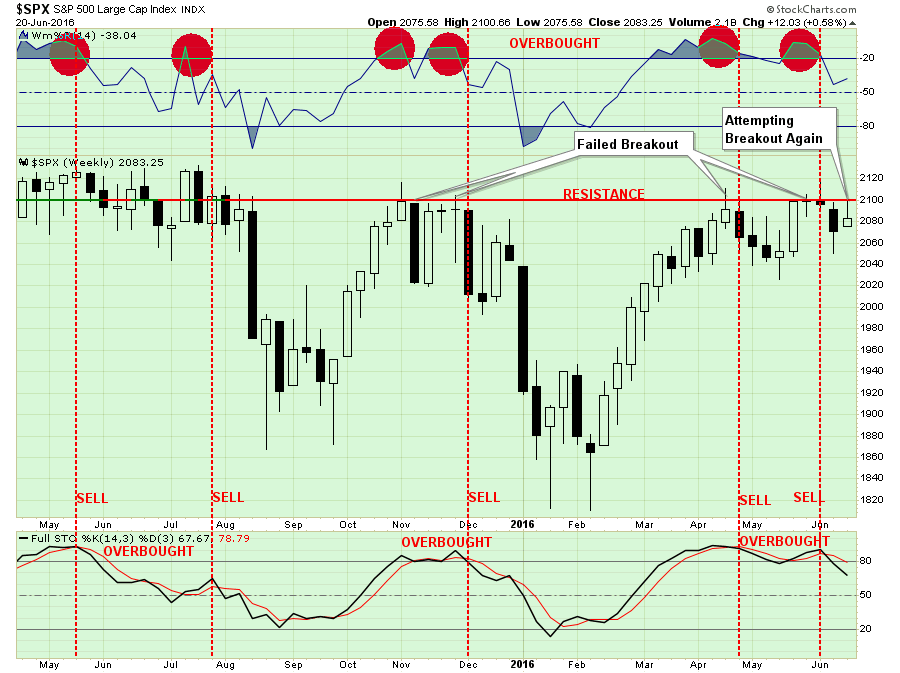

The next chart shows the now 13-month long sideways trading range of the market. However, most importantly, the downward trending price pattern remains in place. The recent failure at the downtrend resistance line remains a concern.

The vertical blue-dashed lines denote market sell signals where subsequent price action has been poor, to say the least. While a “sell signal” is NOT CURRENTLY in place, it will not require much further deterioration in price to trigger one.”

What is important to note is the compression that is building between the short-term moving average (blue dashed line) and the current “downtrend resistance.” That compression will resolve itself it soon and will lead to a breakout that will retest highs of 2135, or a break below support at 2040.

While anything is certainly possible in the current “Central Bank” driven environment, logic would dictate that most investors will not be comfortable pushing markets to new highs without proof of greater economic health from the early July economic data.If weakness, it will be hard for stocks to advance further on a longer-term basis. However, this continues to be a market focused more on short-term “hopes” rather than longer-term fundamental dynamics anyway.

The problem is that such short-term focuses have generally led to rather poor longer-term outcomes. As I penned yesterday:

“History is replete with market crashes that occurred just as the mainstream belief made heretics out of anyone who dared to contradict the bullish bias.

It is critically important to remain as theoretically sound as possible. The problem for most investors is their portfolios are based on a foundation of false ideologies. The problem is when reality collides with widespread fantasy.”

DO NOTHING

There are times in portfolio management where “doing nothing” is better than “doing something.” This is one of those times.

With portfolios already running at just 50% of total recommended equity exposure, portfolio risk is already substantially mitigated. This leaves us is the best place to be for the moment as we await the outcome of the “Brexit” vote on Thursday and the culmination of Yellen’s testimony on the “Hill.”

From that vantage point, we can then assess the markets and make a reasonable assumption about what to do next. Could we miss a bit of upside? Absolutely. But such a small lag is a much better outcome than trying to recoup a substantial loss if things go wrong.

Importantly, whatever the vote on Thursday turns out to be, the focus of the markets will once again turn back global economic realities which remain wanting at best. As Andrew Lapthorne noted from SocGen (via ZeroHedge):

“Whatever the outcome of the Brexit vote this week investors will still be facing the prospect of negative rates and negative yields on a huge range of bonds, massive corporate leverage with worryingly rising delinquencies and of course expensive equity markets and falling profits. To that extent these political events are a distraction from the main event, weak global economic growth and perverse asset markets. So whilst the market preference for the status quo might be celebrated in the short-term, actually when the fog clears all of the problems will still be there.“

Lance Roberts

Lance Roberts is a Chief Portfolio Strategist/Economist for Clarity Financial. He is also the host of “The Lance Roberts Show” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, and Linked-In