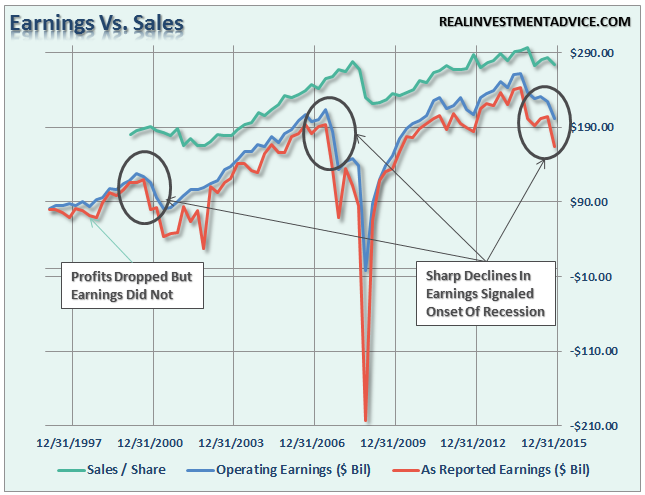

As the trumpets sound to signal the start of earnings season, the battle between fundamentals and “hope” begins. Despite weakening earnings, which on an as reported basis are far worse than the rather manipulated “operating” levels currently suggest, the bulls have remained steadfast in their belief that prices are on a one-way trip higher.

What all investors should remember is that it is what happens at the “top line” of income statements that is a true reflection of the underlying economy. As I discussed in this past weekend’s missive which covered the “profit backdrop.”

“Economic growth is a function of consumption. If economic growth is weak, then consumption must therefore also be weak. If consumption is weak, then corporate revenues will also be weak. As shown below, declines in revenue have been a strong precursor to economic recessions. Of course, while accounting gimmicks and share buybacks can buoy profits temporarily, it is not sustainable and the eventual downturn is inevitable.”

“The point here is that while prices have improved short-term, which have been a function of the “verbal easing”issued by the Fed, the underlying realities of the market are far different. As is always the case, estimates are likely to fall sharply as economic reality continues to take hold.

Why anyone pays attention for forward estimates is beyond me given a 90% miss rate. Remember that the next time someone tells you that “stocks are cheap based on forward estimates.”

Could prices maintain their current levels long enough for the economic cycle to turn and catch up? Possibly. It has just never occurred before in history….ever.”

In the longer-term it is only fundamentals that matter. What is happening between the economic and earnings data is all you really need to know if you are truly a long-term investor.

Unfortunately, you aren’t.

Despite all of the arm waving and foot stomping that you are a long-term investor, I will bet before you even read this article you have already logged checked on your investments at least once, looked at the markets both pre- and post-open, and have fretted over the level of your exposure.

The emotional biases of being either bullish or bearish, primarily driven by the media, keep you from truly focusing on long-term outcomes. You either worry about the next downturn or are concerned you are missing the rally. Therefore, you wind up making short-term decisions which negate your long-term views.

Understanding this is the case, let’s take a look at the technical case for the markets from both a bullish and bearish perspective. From there you can decide what you do next.

THE BULL CASE

1) The Fed Won’t Let The Markets Crash

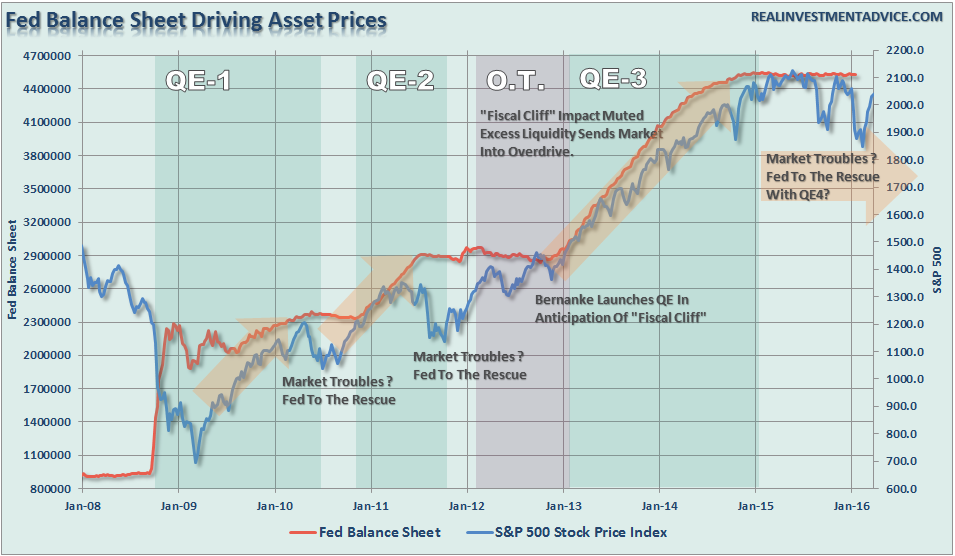

This is the primary support of the bullish case, and frankly, one that is difficult to argue with. Despite all of the hand-wringing over valuations, economics or fundamental underpinnings, stocks have been, and continue to be, elevated due either to “direct” or “verbal” accommodation.

I discussed this idea of “permanent liquidity” in deeper detail yesterday.

“But what ongoing liquidity interventions have accomplished, besides driving asset prices higher, is instilling a belief there is little risk in the markets as low interest rates will continue or only be gradually tightened.”

However, “verbal accommodations” have also been extremely supportive since the end of QE-3 in keeping asset prices elevated.

“Bad news is good news” has been the “siren’s song” for the bulls since the end of direct interventions as “low rates for longer” means the “chase for yield” continues.

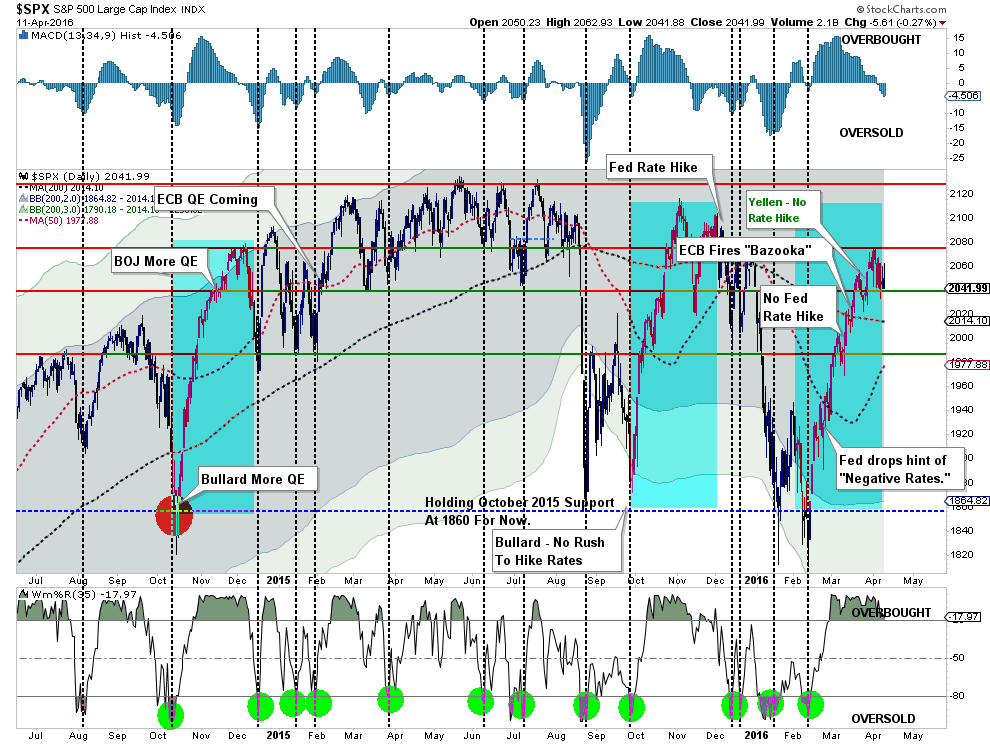

2) Stocks Have Made Successful Retest Of Lows

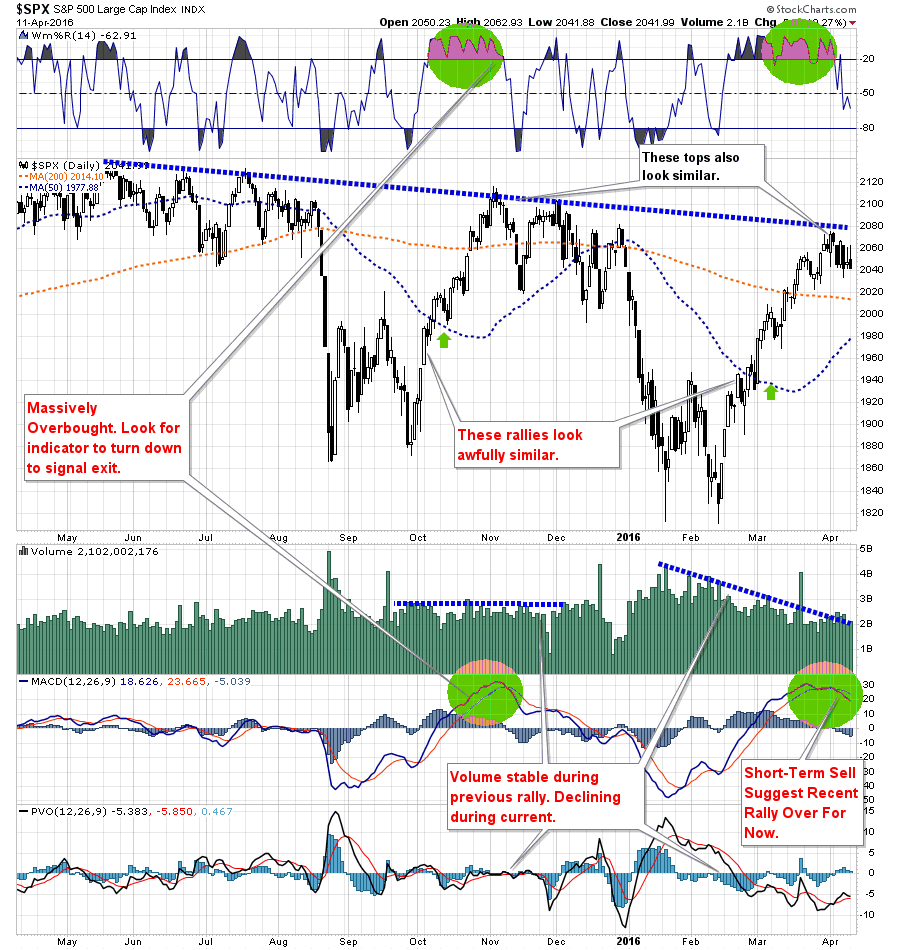

As I discussed in last weekend’s newsletter, there is a case being made for a further upside advance in the markets. The market has made repeated retest of the October, 2014 lows and the recent retracement rally has cleared both the 200 & 400-day moving averages.

Furthermore, the very short-term overbought condition has been almost worked off by the “back and forth” action of the market last week. This set up would suggest a consolidation period which could provide the “fuel” necessary for an advance to the next resistance levels at 2100.

However, it is worth noting that we saw very similar action following the “summer swoon” last year which failed at the beginning of this year. As we once again approach the “summer period,” particularly heading into a November election, any advance could be limited.

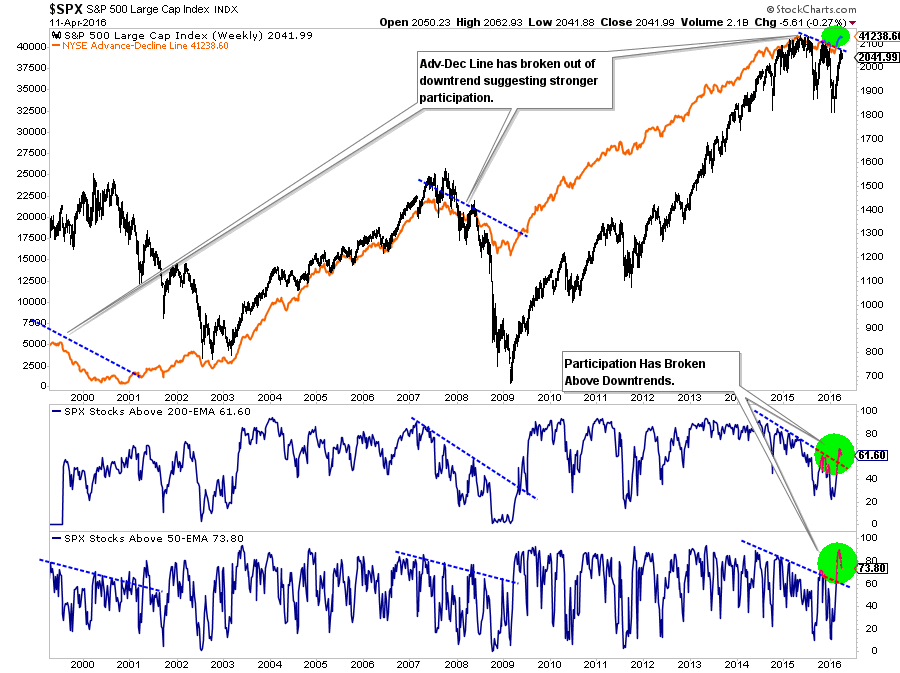

3) Advance-Decline Line Is Improving

The participation by stocks in the recent bullish advance has been strong enough to push the advance-decline line above the recent downtrend.

Such a rise in participation suggests the momentum behind stocks is supportive enough to push stocks to higher levels and should not be dismissed lightly.

As I have repeatedly stated:

“Currently, as shown above, the short-term dynamics of the market have improved sufficiently enough to trigger an early “buy” signal. This suggests a moderate increase in equity exposure is warranted given a proper opportunity. However, to ensure that the current advance is not a “head-fake,” as repeated seen previously, the market will need to reduce the current overbought condition without violating near-term support levels OR reversing the current buy signal.”

We are close to those conditions being satisfied.

WARNING:

Let me be VERY CLEAR – this is VERY SHORT-TERM analysis. From a TRADING perspective, there is a tradable opportunity being developed. This DOES NOT mean the markets are about to begin the next great secular bull market. Caution is highly advised if you are the type of person who doesn’t pay close attention to your portfolio or have an inherent disposition to “hoping things will get back to even” if things go wrong rather than selling.

THE BEAR CASE

The bear case is more grounded in longer-term price dynamics – weekly and monthly versus daily which suggests the current rally remains a reflexive rally within the confines of a more bearish backdrop.

1) Short-Term: Market Rally On Declining Volume, Fails At Resistance

The recent market rally, while strong, occurred amidst declining volume suggesting more of a short-covering rally rather than a conviction to a “bull market” meme.

Furthermore, the rally has currently failed at the downtrend that began from the previous market highs in 2015. In order for the market to reverse the “bearish” context a breakout above that downtrend resistance will need to occur.

2) Longer-Term Dynamics Still Bearish

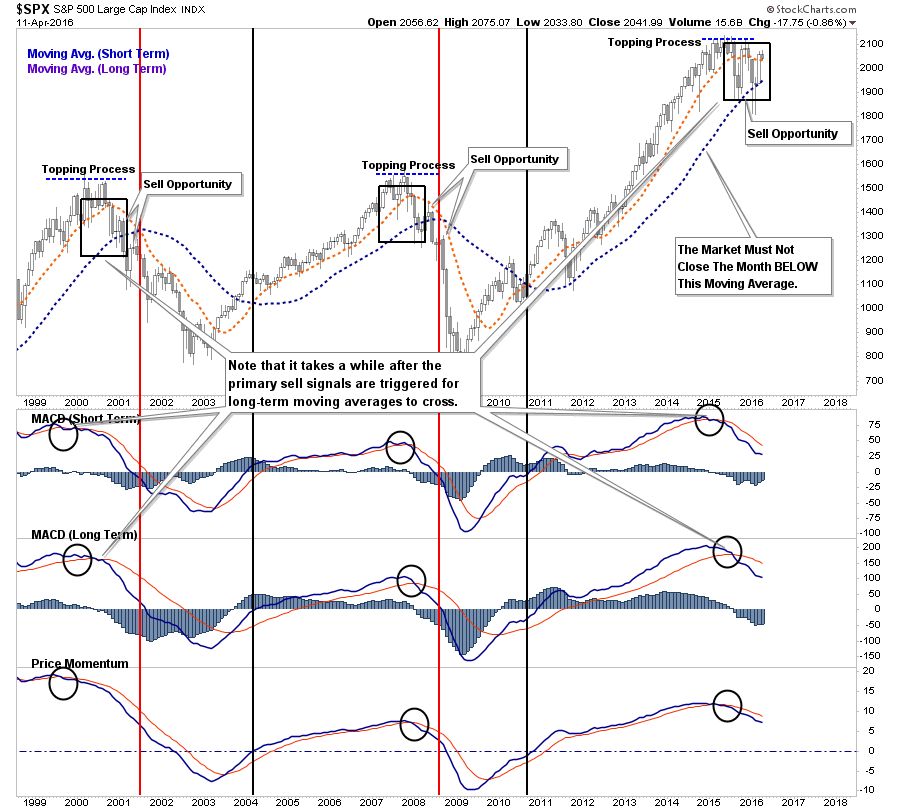

If we step back and look at the market from a longer-term perspective, where true price trends are revealed, we see a very different picture emerge. As shown below, the current dynamics of the market are extremely similar to those of the previous two bull market peaks. Given the deterioration in revenues, bottom-line earnings, and weak economics, the backdrop between today and the end of previous bull markets is consistent.

3) Bonds Ain’t “Buyin’ It”

If a “bull market” were truly taking place we should see a flight from “safety” back into “risk.” As shown below, the declines in the stock-bond-ratio has been coincident with both short and long-term market corrections.

Currently, we are not seeing “risk taking” being a predominate factor at the moment. Could this change, absolutely. But one particular point to note is the steady decline in the ratio since the beginning of 2014. While the decline is more protracted, it is similar to what was seen in 2007.

What you decide to do with this information is entirely up to you. As I stated, I do think there is enough of a bullish case being built to warrant taking some equity risk on a very short-term basis.

However, the longer-term dynamics are clearly bearish. When those negative price dynamics are combined with the fundamental and economic backdrop, the “risk” of having excessive exposure to the markets greatly outweighs the potential “reward. “

Could the markets rocket up to 2100, 2200 or 2300 as some analysts currently expect? It is quite possible given the ongoing interventions by global Central Banks.

The reality, of course, is that while the markets could reward you with 250 points of upside, there is a risk of 450 points of downside just to retest the previous breakout of 2007 highs

Those are odds that Las Vegas would just love to give you.

Lance Roberts

Lance Roberts is a Chief Portfolio Strategist/Economist for Clarity Financial. He is also the host of “The Lance Roberts Show” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, and Linked-In