“I would be open to the possibility” of reducing the fed funds rate “even further” and go negative, explained Minneapolis Fed President Narayana Kocherlakota on Thursday. Some folks just don’t get it.

Here are the results of seven years of global QE and zero-interest-rate policies:

Global demand is going from sluggish to even more sluggish. Emerging market countries are leading the way, it is said, and China is sneezing. Brazil and Russia have caught pneumonia. Japan is feeling the hangover from Abenomics. Even if there is some growth in Europe, it’s small. And the US, “cleanest dirty shirt” as it’s now called, is getting bogged down.

And here’s what this is doing to the shipping industry, the thermometer of global economic growth.

On one side: lack of demand.

Due to the “recent slowdown in world trade” shipping consultancy Drewry on Thursday slashed its forecast for container shipping growth, in terms of volume, to 2.2% for 2015 and lowered its estimates for future years. BIMCO, the largest international shipping association representing shipowners, issued its own, even gloomier reportalso on Thursday:

On the US West Coast, it’s been slow all year, starting with the labor disputes that weren’t resolved until mid-March. Since then, year-on-year growth in the second quarter was almost on par with 2014. But for the first half year alone, inbound loaded volumes dropped by 2% according to BIMCO data.

On the Asia to Europe trades, volumes were down by 4.2% in the first half of the year as 7.4 million TEU (Twenty-foot container Equivalent Units) was transported. Northern European imports fell by 3.6%, while the East Med and Black Sea imports fell by 4.8%.

Intra-Asia shipments remain a stronghold with ongoing positive growth around 4-5%, but the increased uncertainty surrounding the economic development in China adds doubt as to whether such a strong growth rate can be sustained for the full year.

At the same time, as shipping volumes struggle, freight rates have collapsed, and revenues with them.

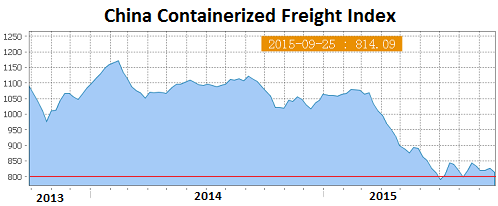

“The severe lack of exports from China” is reflected in the China Containerized Freight Index (CCFI), BIMCO pointed out. The index, which tracks freight rates from China to major ports around the world, plunged below 800 in early July for the first time in its history (it was set at 1,000 in 1998). It’s currently at 814. The red line marks 800:

On the other side: over-capacity.

Drewry estimates that an additional 1.6 million TEU of new capacity is being added to the container shipping fleet this year, and not enough ships are being scrapped. Hence a fleet growth rate of 7.7%:

As a result, Drewry’s Global Supply/Demand Index, a measure of the relative balance of vessel capacity and cargo demand in the market where 100 equals equilibrium, has fallen to a reading of 91 in 2015, its lowest level since the recession ravaged year of 2009.

But in 2016, another 1.3 million TEU of new capacity will be delivered. Drewry projects that its “Global Supply/Demand Index will fall to its lowest level on record over the next few years, indicating that the overhang of excess capacity will be even greater than that experienced in 2009.”

So freight rates have crashed globally. But graciously, the oil price crash led to lower bunker fuel prices, which has kept some, but not all shippers afloat.

Shipping lines have responded half-heartedly with idling some of their ships, but so far without great success in raising rates. And these ships are heavily leveraged, so idling them and not earning revenues while having to service their debts isn’t helping matters.

So shipping loans are a doozy.

Germany is a hotbed for shipping loans, to the point where Andreas Dombret, member of the Executive Board of the Bundesbank, highlighted them in February 2013 as one of the four risks to overall financial stability in Germany. He fingered two causes: plunging freight rates and overbuilding of ships of ever larger sizes, driven by “cheaply available financial means” – a direct reference to easy-money policies.

He waded into the bloodbath in Germany: shipping loan retail funds that blew up and were shuttered, banks whose shipping portfolios suffered heavy hits, an industry that was breaking down…. The Bundesbank was looking at it from a “broader perspective,” he said, with an eye “on the stability of the entire financial system.”

He knew what he was talking about.

A month later, the largest ship-financing bank in the world, HSH Nordbank, which had been bailed out in 2008, re-collapsed and was re-bailed out by its two main owners, the German states of Hamburg and Schleswig-Holstein.

The ECB, which now regulates the largest European banks and last year conducted the most intrusive stress tests in EU history, is putting pressure on HSH to finally clean up its bad loans, which still make up a stunning 23% of its total loan book, “sources” toldReuters in July. Even some Greek banks don’t have this much putrefaction hidden in their basements.

In the US, Citigroup sallied into shipping loans when it bought a “significant” part of Société Générale’s shipping loan book for an undisclosed price in June 2012.

“Citi is looking to increase their shipping exposure in the market, and it is easier to acquire loans rather than originate them from scratch,” the source told Reuters at the time. It would have “an edge” in dealing with the shipping loans because they’re mostly in dollars.

A year later, Citi converted about $500 million of loans to non-US shipping companies into complex structured securities in order to roll some of the risk off to other investors, for a price: a yield between 13% and 15%, “these people” told the Wall Street Journal. Not sure how the deal turned out and what happened to the remaining shipping loans on Citi’s books, but since then…

Here’s what’s been happening in bankruptcy court:

September 29, 2015: shipping company Daiichi Chuo KK filed for bankruptcy protection in Tokyo after four years in a row of losses, listing about $1 billion in liabilities.

February 2015: Copenship filed for bankruptcy in Copenhagen, Denmark, after losing its behind in the dry bulk market that has been struggling for a lot longer than the container market.

February 2015: China’s Winland Ocean Shipping Corp filed for Chapter 11 bankruptcy in the US.

“The combination of lower steel demand in China and the huge volume of new tonnage coming on line is what is causing panic and making this the worst bulk market since the mid-1980s,” explained at the time Hsu Chih-chien, chairman of Hong Kong and Singapore-listed shipper Courage Marine.

August 2014: Nautilus Holdings and subsidiaries filed for Chapter 11 bankruptcy in New York, listing $770 million in debts.

April 2014: Genco Shipping and Trading, owned by New York shipping tycoon Peter Georgiopoulos, filed for Chapter 11 bankruptcy in New York, listing about $1.5 billion in liabilities.

July 2013: Excel Maritime Carriers filed for bankruptcy.

There were other shipping companies that destroyed investor capital in a similar manner, and more will join. The dry-bulk fiasco started years ago, and the commodities rout has made it worse. Container shipping is just now getting put through the wringer, and the “financial pain,” as Drewry put it, will last for years.

This is what our dear soon-to-be professor Kocherlakota doesn’t get: When as a result of monetary policies, the cost of capital has been close to nil for the right folks for long enough, and desperate investors are out there blindly chasing whatever yields they can get, there are consequences: malinvestments.

And they beget overcapacity and over-supply, which beget the destruction of pricing power, which unleashes deflationary forces, which inflict heavy losses on companies in the sector, which finally seek refuge in bankruptcies, which finalize capital destruction. None of which beget a healthy economy.

So there are some issues in this distorted world, demonstrated by scary chart of a staggering reversal. Read… China, Russia, Norway, Brazil, Taiwan Dump US Treasuries