When the Reserve Bank of Australia cut its cash rate target to a record low of 2.0% this week, it specifically blamed the slowdown in China. It is the key market for Australia’s most important exports, such as iron ore, whose price has plunged due to slowing demand in China, dragged down by a number of factors, including weak exports of manufactured goods to slowing economies around the globe.

Trade moves in wobbly circles.

So today, China’s General Administration of Customs announced that imports had plunged 16.2% in April from a year ago, after they’d already plunged 12.7% in March (hence the fretting by the Reserve Bank of Australia). And exports dropped 6.4% from a year ago, after they’d plummeted 14.6% in March.

Analysts, who apparently never look at the collapsing shipping rates from China to certain parts of the world, had inexplicably expected exports to rise 2.4%. So the drop was “unexpected.”

The morose economic climate was unexpected apparently even at the very top in China: Reuters was told by “policy insiders” that China’s leaders were “caught off guard by the sharpness of the downturn.”

That hasn’t kept the Chinese stock market from soaring 75% over the past six months, despite the 5% swoon this week, the worst weekly loss in five years.

And so rumors of more stimulus of one kind or another have been circulating. Stimulating demand by creating more credit and building more high-speed rail lines and subway systems and allowing local governments to borrow more to build even more overcapacity is one thing. But stimulating demand in other countries is quite another. And that’s one of the sources of the China slowdown.

Exports to the US inched up 3.1% in April from a year ago, not exactly a dizzying pace. But exports to the EU plunged 10.4%.

The collapse of containerized freight rates from China to Europe have reflected that kind of drop in exports for two months, and I have been hammering on it [most recently a week ago]. And freight data released today are even worse.

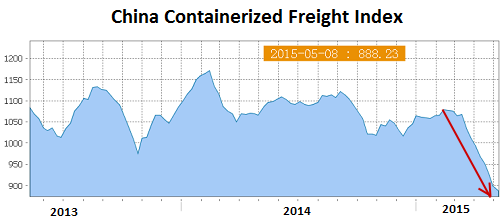

The China Containerized Freight Index (CCFI), operated by Shanghai Shipping Exchange and sponsored by the Chinese Ministry of Communications, tracks spot and contractual freight rates from Chinese container ports for 11 shipping routes across the globe, based on data from 16 global carriers. According to the SSE, it’s considered “the second world freight index” after the Baltic Dry Index.

And it skidded again. The index for the week just ended dropped another 11 points, or 1.2%, from the prior week to a new multi-year low of 888. It’s down 17% since mid-February. This is what the 2-month plunge looks like:

How ugly is this? The index was set at 1,000 on January 1, 1998. Today, the index is 11% below where it was 17 years ago, a journey it accomplished in two months!

Trade is a circular machine. Manufacturing and export economies, like China, import commodities and export manufactured goods. The plunge in imports is an all-around terrible reflection of demand in China, despite the still relatively glorious and most likely illusory 7% GDP growth bandied about by the government.

But the slowdown in exports is a sign of slowing demand in other parts of the world, particularly in Europe, where the purposeful devaluation of the euro is sinking in. Tough times ahead, not only for China.

As if a toggle switch had been flipped late last year, Americans suddenly gained confidence in the economy, to levels not seen since before the Financial Crisis. But now, it’s all unraveling. And the culprits are being lined up. Read… Confidence in the US Economy Plunges