By Tyler Durden at ZeroHedge

Peer-to-peer lending is probably a bad idea.

Securitizing peer-to-peer loans is definitely a bad idea.

Despite these virtually irrefutable truths, the P2P industry is thriving and Wall Street’s securitization machine couldn’t be happier about it. Aswe reported last May, P2P loan volume was set to surpass $76 billion in 2015 and one driver of the boom is demand from the likes of BlackRock, Morgan Stanley, and Goldman, who have all underwritten securitizations of loans originated on P2P platforms like LendingClub, the number one player in the space.

As we noted last summer, P2P loans create the conditions whereby borrowers can refi high-interest debt via personal loans, transferring credit risk from large financial institutions to private lenders in the process.

It’s not entirely clear what the implications of that shift might ultimately be, especially if the market continues to grow rapidly. “One thing,” we said, “is clear”: Using a relatively low-interest P2P loan to pay off a high-interest credit card is no different in principle than using a new credit card that comes with a teaser rate to pay off an old credit card.

In the end, the borrower will very often max out the old card again and thus end up with twice the original amount of debt.

The same dynamic applies to P2P lending. “So what’s to stop consumers from levering their credit cards back up?” Bloomberg asked last year. “Such behavior could spell bad news for investors in P2P loans if an interest rate hike or an unforeseen shock pressures borrowers,” Michael Tarkan, an equities analyst at Compass Point Research said.

“We’ve created a mechanism to refinance a credit card into an unsecured personal loan,” he added. “This may prove to be a superior model, but we just don’t know because it hasn’t been tested yet through a full credit cycle.”

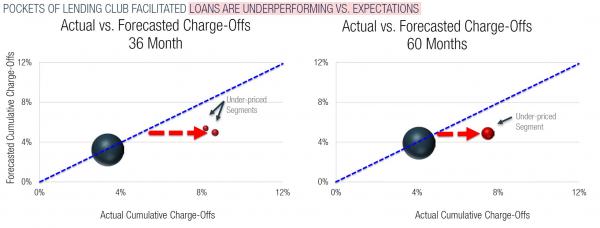

No, we “just don’t know”, but we may be about to find out because a new presentation from LendingClub indicates that the cracks are starting to show. “LC Advisors, an investment adviser owned by LendingClub that helps people buy loans arranged by the company, said last week in a presentation that some of the debt is ‘underperforming vs. expectations,’” Bloomberg wrote on Friday. “A chart on one of the slides shows that write-off rates for a portion of five-year LendingClub loans were roughly 7 percent to 8 percent, compared with a forecast range of around 4 percent to 6 percent.” Here’s the slide in question:

In other words, the algorithms LendingClub uses to assess credit risk aren’t working. Plain and simple.

“Their business is to take data and use that to underwrite risk,” the aforementioned Michael Tarkan told Bloomberg by phone. “If you’re an investor in the loans on the platform, this creates a concern around that underwriting model.”

It sure does, as does common sense. Matching up individual borrowers and lenders may sound like a good idea in principle, but effectively, you’ve got a brand new set of companies (the P2Ps) attempting to assess individual borrowers’ credit risk on the fly in cyberspace, an absurdly difficult proposition and one that obviously comes with myriad risks especially when those credits are sliced up and sold to investors.

Securitizations of these loans are just consumer ABS deals. That is, they’re no different than securitized credit card receivables or the nightmarish deals that emanate from Springleaf and OneMain.

What the slide above shows is that LendingClub is terrible at assessing credit risk. A write-off rate of 7-8% may not sound that bad (well, actually it does, but because P2P is relatively new, we don’t really have a benchmark), it’s double the low-end internal estimate. That’s bad.

Throw in the fact that LendingClub is raising rates “to prepare for a potential slowdown in the US economy” and the fact that 70% of the jobs created by America’s supposedly “robust” labor market are in the food and bev/ retail sector, and you can bet that charge-offs will skyrocket should the US careen into a recession.

Then again, it could be worse for LendingClub investors. The company could be run by Ding Ning.

Source: P2P Cracks Start to Show as LendingClub Write-Offs Double Forecasts – ZeroHedge