In business, the 80/20 rule states that 80% of your business will come from 20% of your customers. In an economy where more than 2/3rds of the growth rate is driven by consumption, an even bigger imbalance of the “have” and “have not’s” presents a major headwind.

I have often written about the disconnect between Wall Street and Main Street. As shown in the chart below, while asset prices were inflated by continued interventions of monetary policy from the Federal Reserve, it only benefited the small portion of the population with assets invested in the market. Cheap debt, excess liquidity and a buyback spree, led to soaring Wall Street and corporate profits, surging executive compensation and rising incomes for those in the top 10%. Unfortunately, the other 90% known as “Main Street” did not receive many benefits.

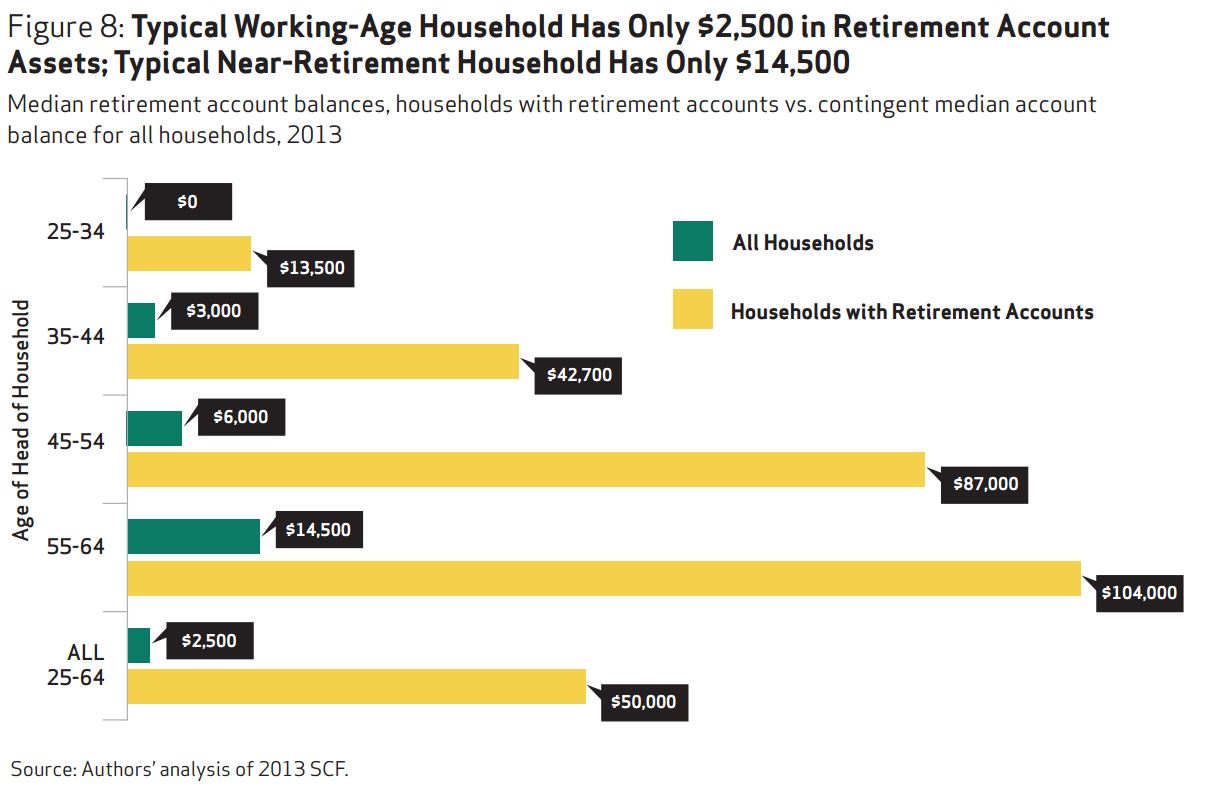

This divide is clearly seen in various data and survey statistics such as the recent survey from National Institute On Retirement Security which showed the typical working-age household has only $2500 in retirement account assets. Importantly, “baby boomers” who are nearing retirement had an average of just $14,500 saved for their “golden years.”

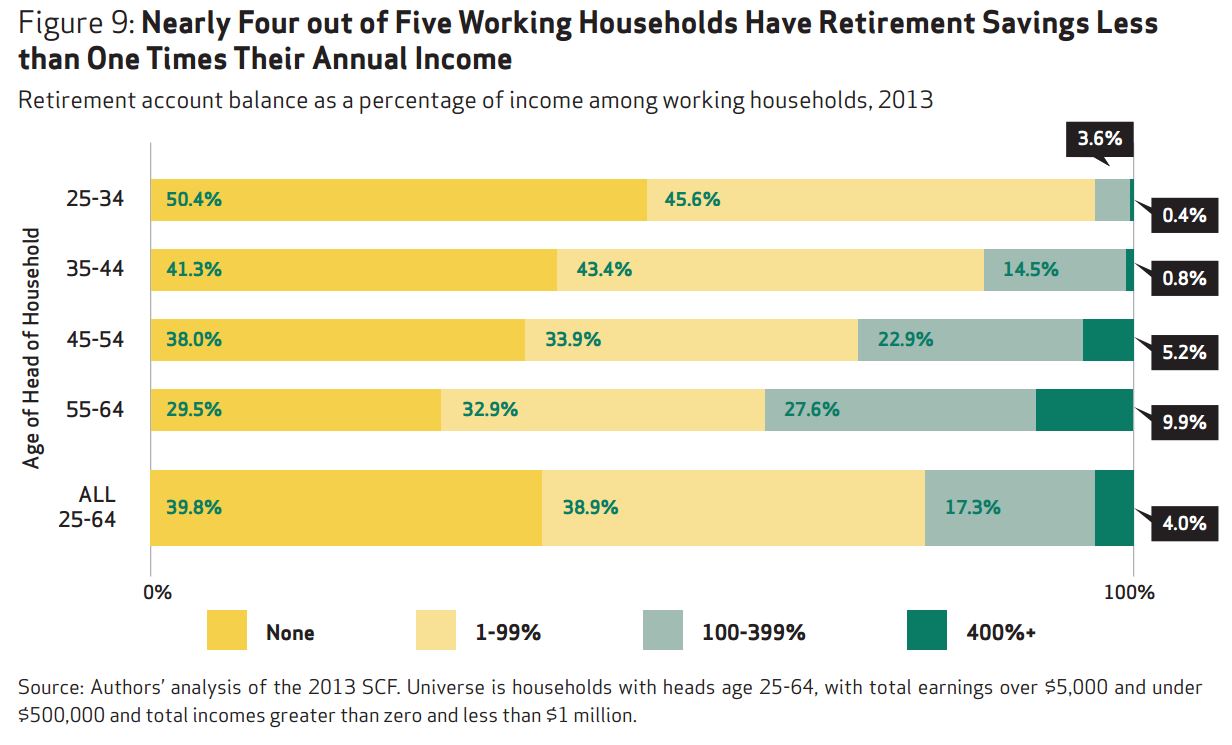

Further evidence of the failure of ongoing Central Bank interventions to spark a broad economic recovery that lifted “all boats” is shown in the chart below. 4-0ut-of-5 working-age households have retirement savings of less than one times their annual income. This does not bode well for the sustainability of living standards in the “golden years.”

Here is the problem that is unfolding for investors going forward. While the mainstream financial press continues to extol the virtues of investing in the financial markets for the “long-term”, the assumptions are based on historical data that is not likely to repeat itself in the future.

Jeff Saut, Liz Ann Sonders, and others have continued to prognosticate the financial markets have entered into the next great “secular” bull market. As I have discussed previously, this is not likely to the be case based upon valuations, debt and demographic headwinds that are currently facing the economy.

Let’s set aside valuations and look strictly at the main driver of economic growth – the consumer.

Demographics Don’t Add Up

One of the big problems for the “secular bull market” story is the transition of a large mass of individuals heading into retirement years from accumulation to spending mode. The chart below shows the number of elderly versus young in millions in the U.S. through the last OECD survey ending in 2014.

The gap between the young and elderly population has shrunk dramatically in recent years as the demographic trends have shifted. Old people are living longer and young people are delaying marriage and children. This means fewer people paying into a social welfare system, while more or taking out. Of course, the burden on the social safety net remains the 800-lb gorilla in the room no one wants to talk about. But with the insolvency of the welfare system looming in less than a decade, I am sure it will become a priority soon enough.

Of course, as we will discuss in a moment, the problem is that while the “baby boom” generation may be heading towards retirement years, there is little indication a large majority of them will be actually retiring. With a large majority of individuals being dependent on the welfare system in retirement, the burden will fall on those next in line.

Welcome to the “sandwich generation” when more individuals will be “sandwiched” between supporting both parents and children in the same household. It should be no surprise multi-generational households in the U.S. are at their highest levels since the “Great Depression.”

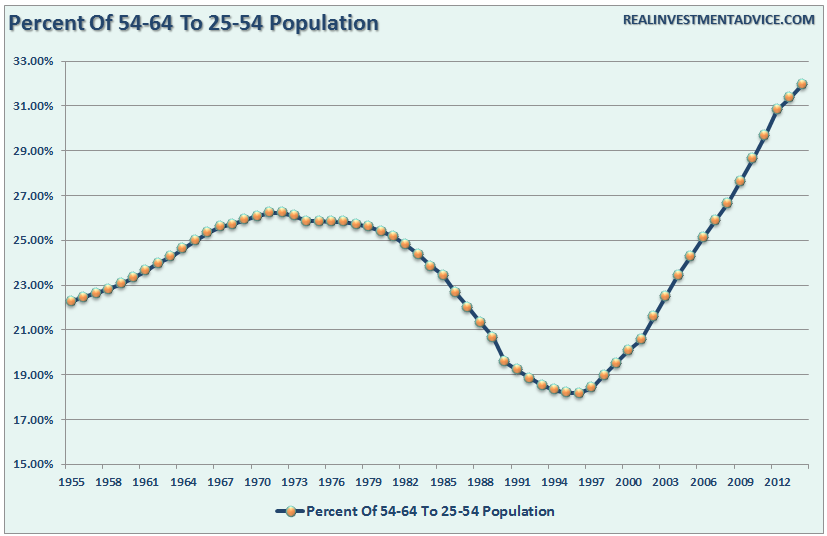

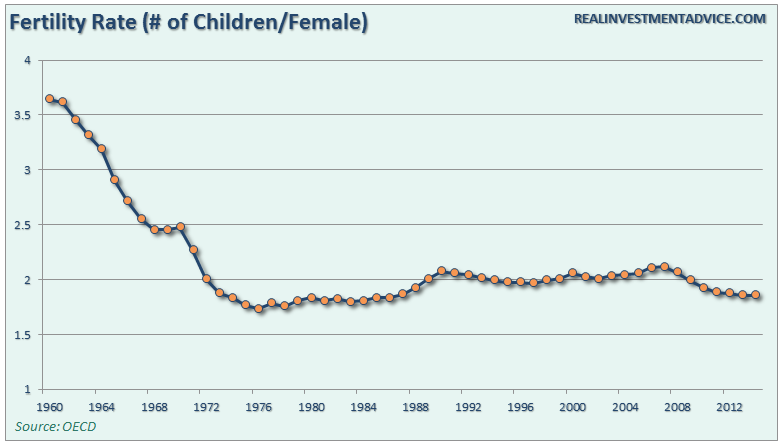

Given the sharp declines in fertility rates over the last 30-years, it is not surprising those over the age of 54 is now at its highest level, as a percentage of those between 25 and 54, in history.

This demographic problem is not going to be fixed anytime soon and has manifested itself in lower rates of household formations.More importantly, the drag from the elderly on the financial system is going to be a much bigger problem than most currently expect.

Employment Is A Problem

But let’s get back to that “secular bull market” theory for a moment. The consumer currently makes up almost 70% of economic growth. More importantly, that consumption is what drives changes in private and fixed investment, imports, and exports all of which feed into the economic growth story. However, in order for the consumer to do their part, they need a “job.” Consumption can not occur without production coming first. In other words, if you don’t have a J.O.B. – you don’t have a P.A.Y.C.H.E.C.K. with which to spend.

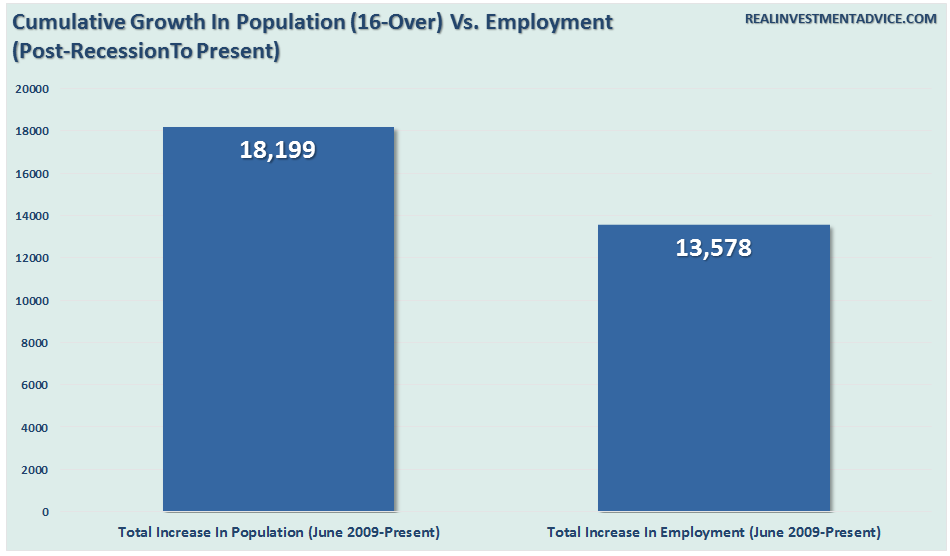

Recent employment increases, while encouraging, have been little more than a function of population growth. As the population grows, incremental demand increases caused by that increase in population will create employment needs in areas most impacted by that population growth. This is why job formation has been primarily focused in retail, service and hospitality areas.

The Census Bureau and Bureau of Labor Statistics provide some fairly comprehensive data about employment that can help us understand the current state of labor force participation. Is it really just an issue of masses of “baby boomers” retiring? Or is it something potentially more structural in nature.

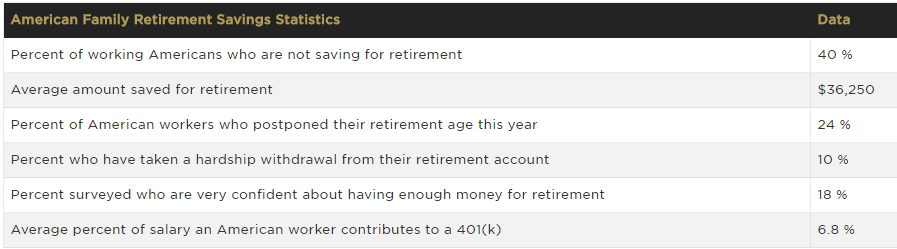

Let’s start with the retirement of the boomer generation. In addition to the survey above, recent statistics show the average American is woefully unprepared for retirement. On average, 40% of American families are NOT saving for retirement, and of those who are, it is primarily about one year’s worth of income. Furthermore, important to this particular conversation, one-fourth of those at retirement age postponed retirement with only 18% being confident of having enough saved for retirement.

For the purposes of this analysis, I am going to exclude all of the “seasonal adjustments” that tend to be a focal point of many of the arguments and utilize a simple 12-month average to smooth the non-adjusted data.

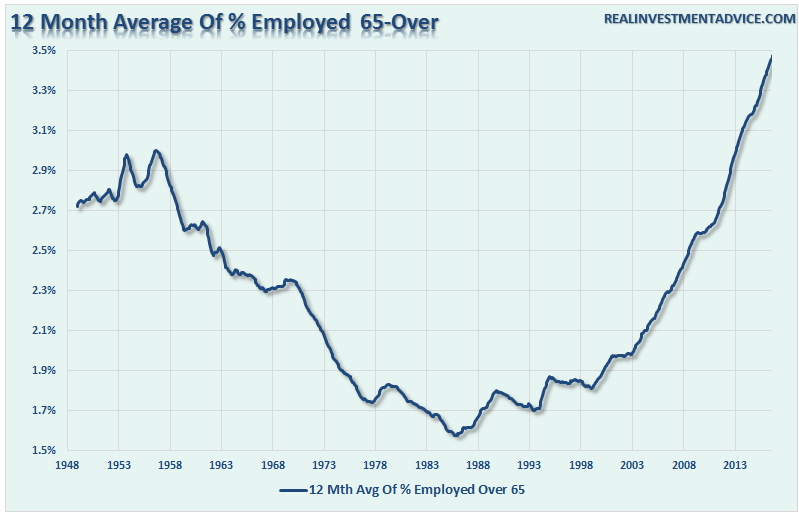

With 24% of “baby boomers” postponing retirement, due to an inability to retire, it is not surprising the employment level of individuals OVER the age of 65, as a percent of the working-age population 16 and over, has risen sharply in recent years.

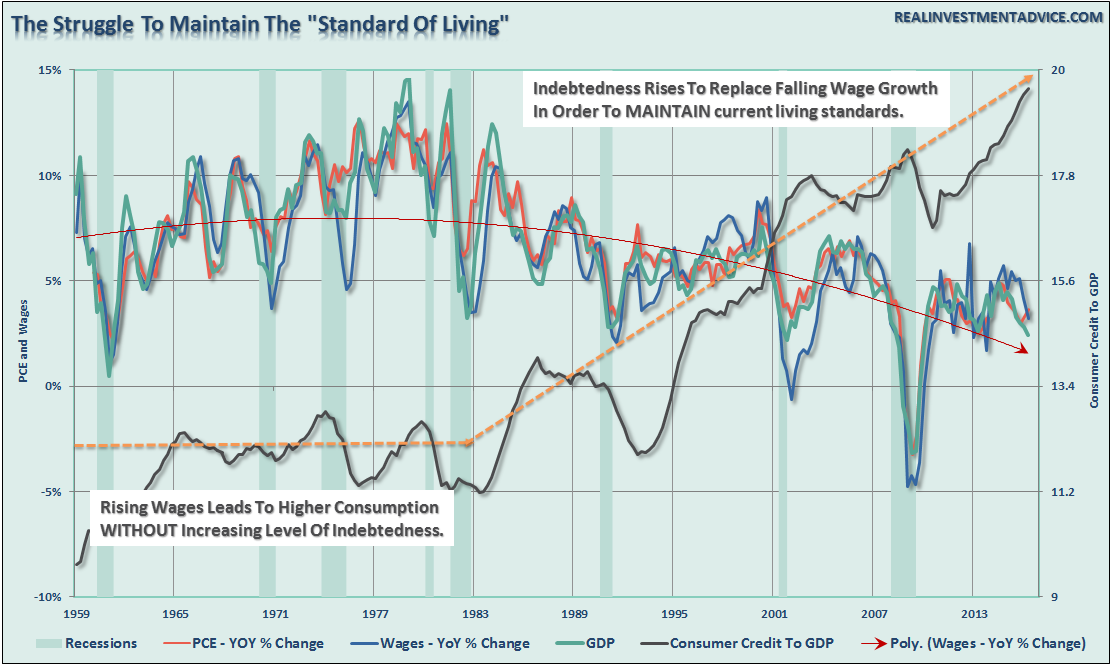

This should really come as no surprise as decreases in economic and personal income growth was offset by surges in household debt to sustain the standard of living. Notice the surge in 65-year and older employment corresponds with the decline of prosperity in the chart below.

During the last “secular bull market,” the “consumption function” was not driven by rising wages, higher interest rates, or strong economic growth. In reality, the economy has been in a weakening trend since 1980. The “illusion” of the last great secular bull market was driven almost entirely by the expansion of credit and financial engineering. In other words, people used credit to make up the difference between their standard of living and weakening levels of wage growth. We have now come to the end of that game.

The problem with the “secular bull market” thesis currently is solely the inability of the consumer to re-leverage another $11 Trillion to support economic growth. With corporations having levered back up to historic peaks to fund share buybacks, dividend payouts, and acquisitions, there is likely little fuel in the tank to support another massive leg higher in the equity markets.

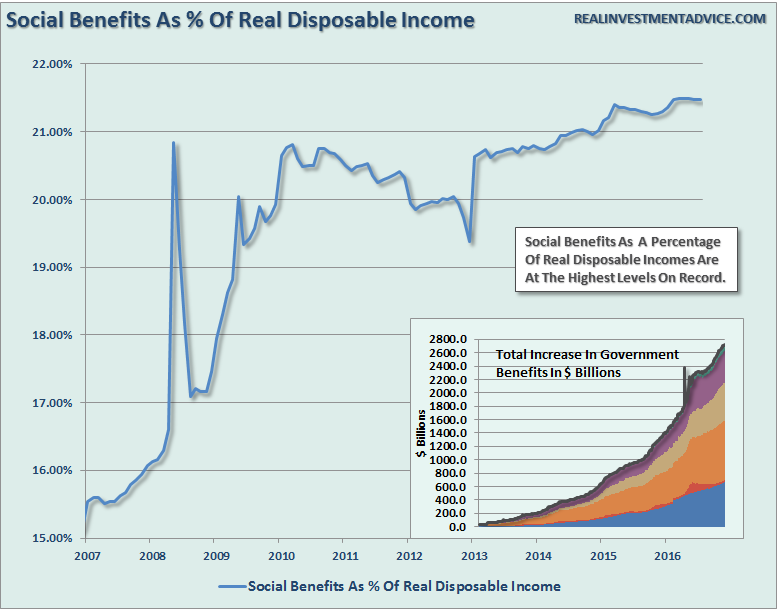

What seems to be missed by the majority of analysis, in my opinion, is whether the economic viability for the average American has improved? The fact social benefits as a percentage of real disposable incomes has risen to an all-time record certainly suggests that it has not.

It would seem to me this would be a much more salient question considering the importance of the consumer on the economic equation and, ultimately, corporate profits and asset prices.

While the Fed has inflated asset prices to the satisfaction of Wall Street, as shown in the first chart above, it has done little to improve real employment or consumption for the vast majority of Americans.

However, my concern is that despite much hope the current breakout of the markets is the beginning of a new secular “bull” market – the economic and fundamental variables suggest that this may not yet be the case. Valuations and sentiment are elevated and interest rates, inflation, wages and savings rates are all at historically low levels. These are the variables which are normally seen at the end of secular bull market periods rather than the beginning.

As stated above, the consumer, the main driver of the economy, will not be able to once again become a significantly larger chunk of the economy than today as the fundamental capacity to re-leverage to similar extremes is no longer available.

There is a huge difference between an organically driven secular bull market in stocks supported by underlying economic strength as opposed to an asset price inflation derived from direct liquidity injections. The former is sustainable, the latter is only sustainable as long as the ability to continue to “juice” the markets remain.

The last point is key. Central Bank interventions are finite. There is a limit to the number of bonds that can be swapped for cash before the credit market seizes entirely. There is also a limit to the ability of the world to operate within the context of a negative interest rate environment.

While stock prices can certainly be driven higher through more global Central Bank interventions, the inability for the economic variables to “replay the tape” of the 80’s and 90’s increases the potential of a rather nasty mean reversion in the future. However, it is precisely such a reversion that will create the “set up” necessary to start the next great secular bull market.

But as was seen at the bottom of the markets in 1942 and 1974, there were few individual investors left to enjoy the beginning of that ride. In the meantime, stop blaming “baby boomers” for not retiring – they simply can’t afford to.