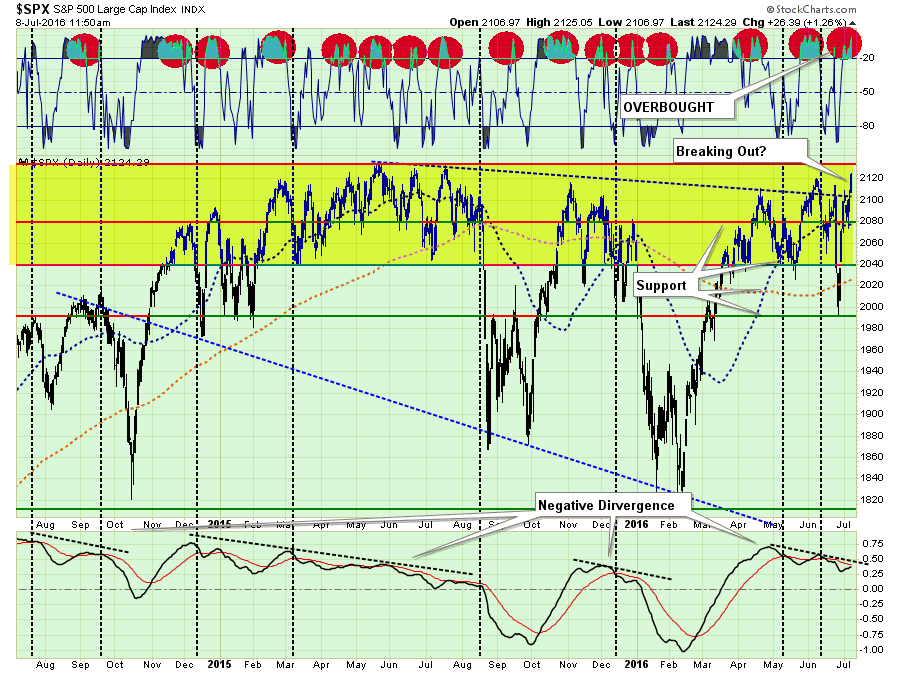

Here we go again. Another Friday. Another attempted breakout above the 2100 level on the S&P 500. Over the last couple of months, as shown below, this has become a regular occurrence.

While the market is once again extremely overbought on a weekly basis, the employment report on Friday which showed a historically abnormal surge in June jobs growth, despite a weaker than expected wage increase and further negative revisions to May’s report, sent investors scrambling into the market. That push on Friday was enough to trigger a short-term buy signal and set the market up for a push to all-time highs.

However, don’t get too excited just yet. There are several things that need to happen before you going jumping head first into the pool.

- We have seen repeated breakout attempts on Friday’s previously which have failed to hold into the next week. Therefore, IF this breakout is going to succeed, allowing us to potentially increase equity allocation risk, it must hold through next Friday.

- The overbought condition on a weekly basis needs to be resolved somewhat to allow enough buying power to push stocks above 2135 with some voracity. A failure at that resistance level could lead to a bigger retracement back into previous trading range of 2040-2100.

- Interest rates, as shown below, need to start “buying the rally” showing a shift from “safety” back into “risk” as seen following the April deviation. (Gold bars show declining rates correlated with falling asset prices. Green bars are rising rates correlated rising assets.)

- Volume needs to start expanding, second chart below, to confirm “conviction“ to a continuation of the “bull market.”

It is important to note, as shown in the chart above, that recent short-term “sell-signals” have been reversed temporarily. However, these are very short-term signals in nature and can be quickly reversed so caution is advised at getting overly excited at the moment.

As shown below, while the market is trying to breakout above 2100, it is doing so with the market, as stated above, extremely overbought and within the context of a negative divergence from longer-term price trends. As shown, these negative divergences have tended to be resolved, although they can take time, with a market correction. Support levels current reside at 2080, 2040, 2030 and 1990.

Importantly, this is not a “bearish” outlook, but rather one that simply suggests caution before adding to current levels of portfolio risk.

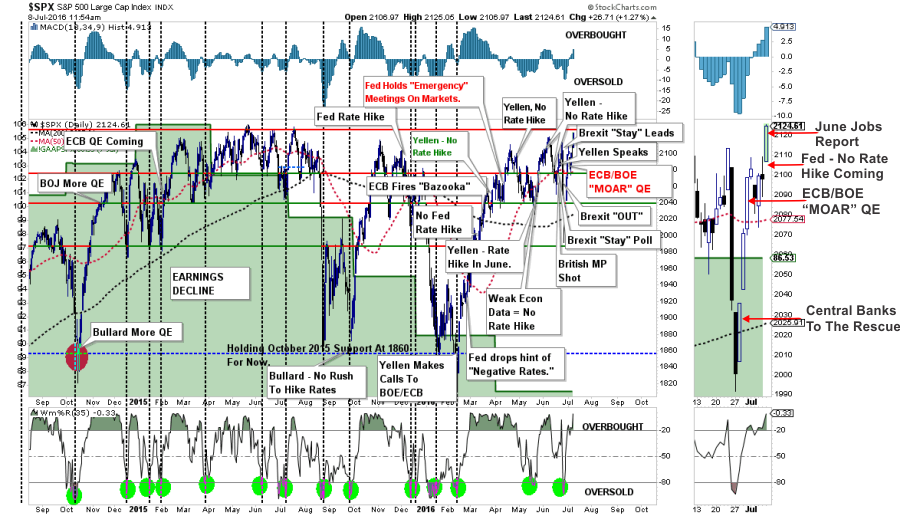

As shown in the chart below, the market has continued to vacillate between one event to the next. From central bankers to job reports, the markets have not been trading on fundamentals but rather or not there will be more support from global Central Bankers. The interesting thing about the jobs report on Friday is that it removes another excuse from the Fed NOT to hike rates in July. They won’t, of course, but according to their own data they should.

Just as a side note, the BLS publishes an adjusted employment number which more accurately reflects what is happening in the real economy. To wit from the BLS:

“For research and comparison purposes, BLS creates an ‘adjusted’ household survey employment series that is more similar in concept and definition to payroll survey employment. The adjusted household survey employment series is calculated by subtracting from total employment agriculture and related employment, the unincorporated self-employed, unpaid family and private household workers, and workers absent without pay from their jobs, and then adding nonagricultural wage and salary multiple jobholders. The resulting series is then seasonally adjusted. The adjusted household survey employment tracks much more closely with the payroll survey measure; nonetheless, occasional trend divergences occur.”

This measure of employment actually DECLINED by 119,000 in June.

As noted by David Rosenberg:

“What if I told you that employment actually declined 119,000 in June and has been faltering now for three months in a row? Yes, that is indeed the case.

It’s not as if the Household sector ratified the seemingly encouraging news contained in the payroll data as this survey showed a tepid 67,000 job gain last month and rather ominously, in fact, has completely stagnated since February.

Historians will tell you that at turning points in the economy, it is the Household survey that tends to get the story right.

The simple fact of the matter is that May and June were massive statistical anomalies. The broad trends tell the tale. Go back to June 2014 and the six-month trend in payrolls is running at a 2.2% annual rate and the three-month trend at 2.4%. A year ago, as of June 2015, the six-month pace was 1.9% and the three-month at 2.2%. Fast forward to today, and the six-month annualized rate is 1.4% and the three-month has slowed all the way down to a 1.2%. This is otherwise known as looking at the big picture.

When the Household survey is put on the same comparable footing as the payroll series (the payroll and population-concept adjusted number), employment fell 119,000 in June — again calling into question the veracity of the actual payroll report — and is down 517,000 through this span. The six-month trend has dipped below the zero-line and this has happened but two other times during this seven-year expansion.”

The chart below enhances David’s work by comparing the 6-month annual percentage change of the adjusted employment index as compared to the official payroll measure, the civilian household measure, and the Fed’s Labor Market Conditions Index. Importantly, on a trend basis, all measures have turned lower.

In other words, don’t put on the “party hats” just yet.

FEAR, NO FEAR

Complacency is back. A week ago, the world was awash in digital ink about how the “Brexit” spelled the demise of the world as we know it. As I stated two weeks ago, this was likely NOT to be the case. Now, the markets are acting as if “Brexit” never existed and fears of a market correction have evaporated.

It is worth noting, however, outside of the two exceptions where Central Banks were fully engaged in liquefying markets, when volatility levels have fallen below 15 it has normally coincided with short and intermediate-term market tops.

Does this mean the market will “crash” next week? Of course, not. However, it does suggest that the recent push higher is likely to “run out of gas” in fairly short order.

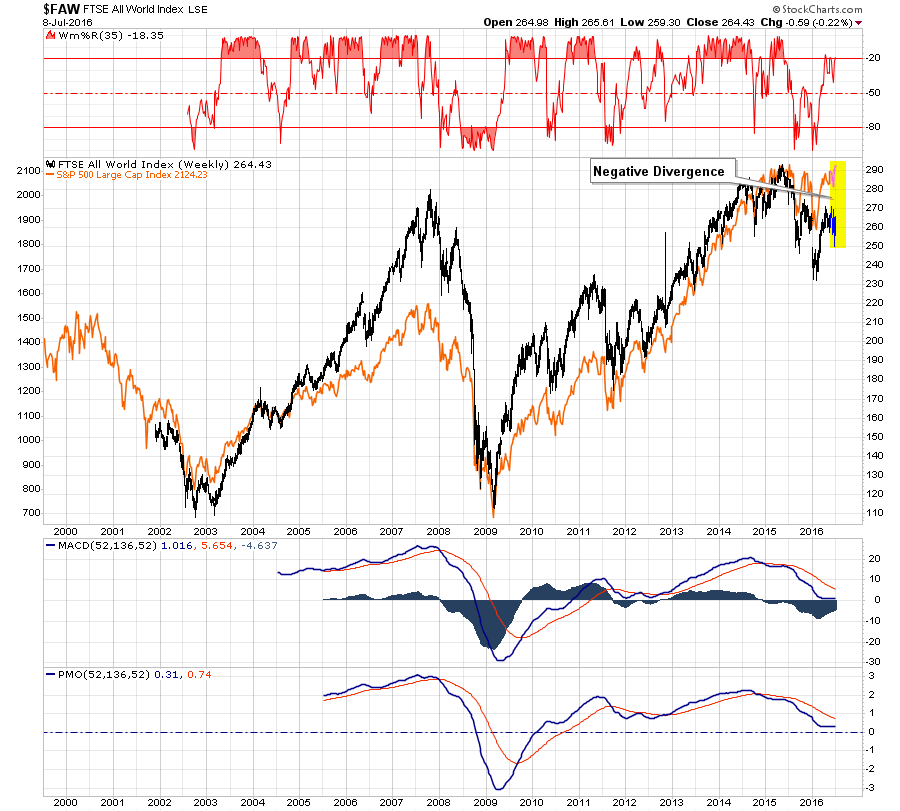

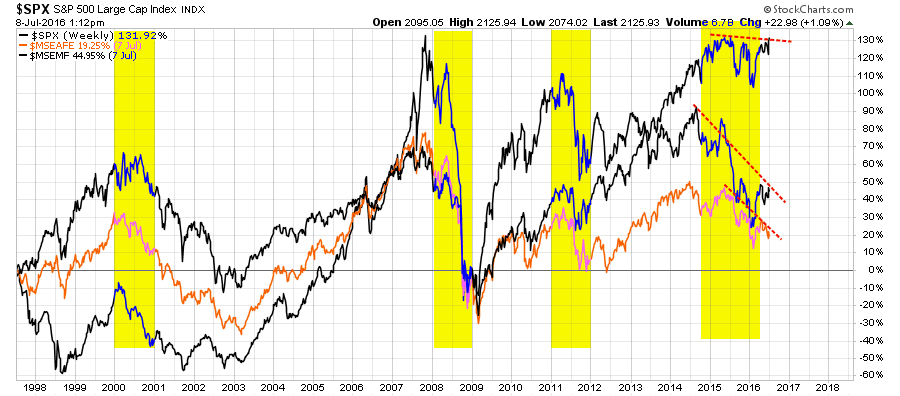

INTERNATIONAL DIVERGENCE

One other interesting point is the current divergence between international and domestic markets. With money fleeing Europe into the “safety” of U.S. denominated assets, the divergence between asset prices, interest rates (noted above) and international markets is not typical. The negative divergence currently being witnessed will likely not last long and either international markets will begin to garner traction or domestic asset prices will revert.

The same negative divergence is also witnessed between the S&P 500 and MSCI International and Emerging Markets indices.

Again, while this does not mean a market reversion is imminent, anomalies in historical correlations have tended not to be long lasting. It is just something worth considering as an investor.

SECTOR BY SECTOR

The analysis of the broad market index gives us some clues about the overall risks being undertaken by investors currently. However, this week, I want to take a look at individual sectors and major asset classes to determine what actions may need to be taken in the week ahead while we await confirmation of the market’s potential “breakout.”

To eliminate the “noise” of daily price movements, I am utilizing a “weekly” chart comprised of 24-months of price data.

Financials

Bank stocks remain in a down trend and continue to significantly under perform the broader market index. Given the current level of interest rates and underweight position in the sector, there is little expectation of substantial outperformance in the near term.

Buy/Sell/Hold/Add: Hold

Weighting: Underweight In Portfolio

Health Care

Health Care stocks broke out of their downtrend in May and made a successful retest of support and have now moved higher. With relative performance increasing the potential for continued outperformance in the near term is likely. Furthermore, this sector is part of the “yield chase” crowd and is pushing more extreme over-valuation levels. Some caution is advised.

Buy/Sell/Hold/Add: Hold/Add

Weighting: Portfolio Weight

Basic Materials

Basic Materials have already experienced an extremely strong run primarily based on the “yield chase” given the extremely weak nature of the global economy. While sector performance is increasing, caution is advised as much of this sector is pushing rather extreme valuation levels.

Buy/Sell/Hold/Add: Hold

Weighting: Portfolio Weight

Industrials

Industrials broke out to a new high this past week showing continued strength in the ongoing “yield chase.” The push high in this sector is not really a sign of an increased upturn in industrial activity as railcar and transportation readings are still exceptionally weak.

Buy/Sell/Hold/Add: Hold/Add On Opportunity

Weighting: Portfolio Weight (Will look to overweight on opportunity)

Consumer Discretionary

After a bit of struggle at the end of last year, the discretionary sector broke out of its downtrend and completed a successful retest of that downtrend over the last couple of weeks. As with industrials, if this sector can break out above overhead resistance there is a potential for further advances.

Buy/Sell/Hold/Add: Hold

Weighting: Portfolio Weight (Look to increase opportunistically on successful breakout.)

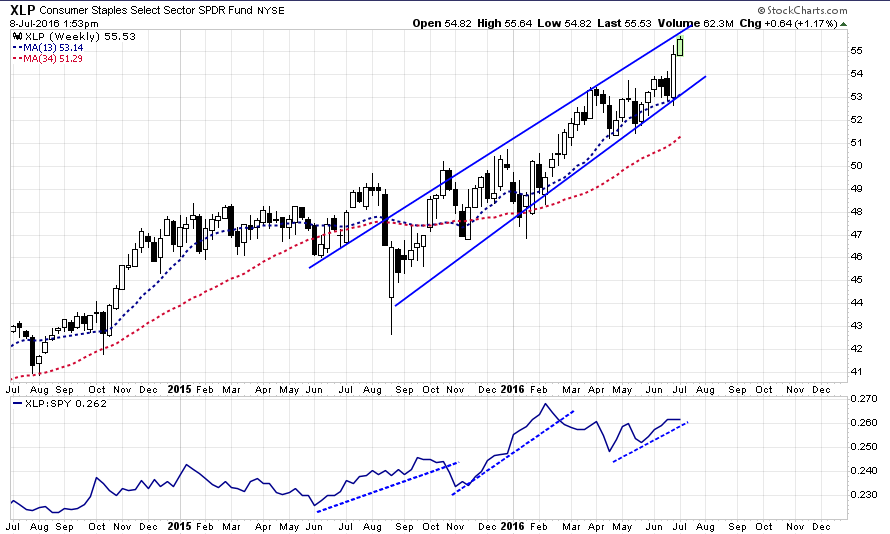

Consumer Staples

Staples continue to be a solid performer for investors. However, staples, like Utilities below, are EXTREMELY overvalued and overbought. Along with Industrials, the “yield chase” in these sectors have pushed prices to extremes. While technically these sectors should remain in portfolios, it comes with a Surgeon General’s Warning: “Chasing Yield Is Hazardous To Your Health.”

Buy/Sell/Hold/Add: Hold (Take Profits)

Weighting: Portfolio Weight

Utilities

As stated above, like Staples, the “Yield Chase” is at extremes. Continue to hold the sector for now, but reduce current positions back to original portfolio weights through prudent profit taking measures.

Buy/Sell/Hold/Add: Hold (Take Profits)

Weighting: Portfolio Weight

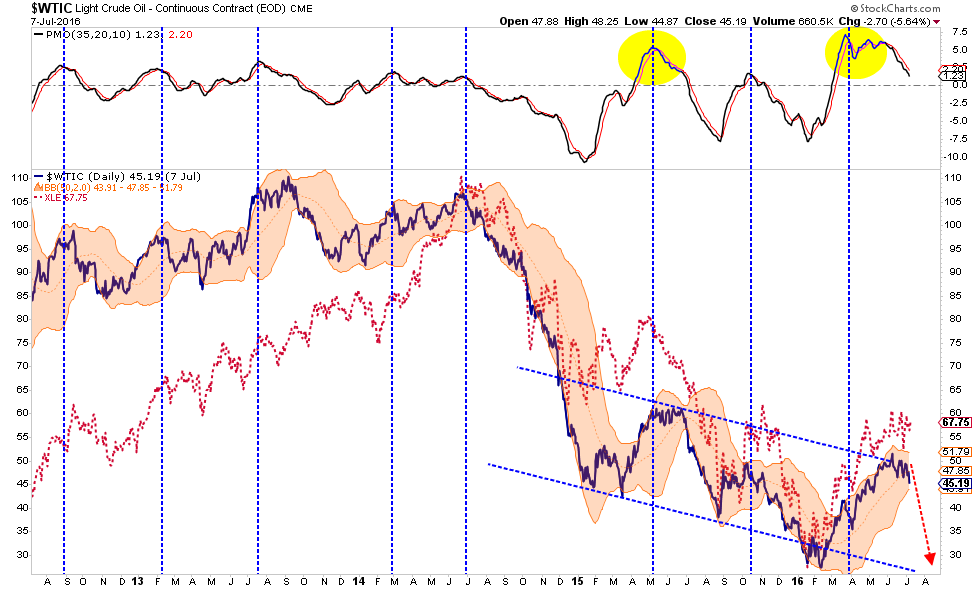

Energy

There are two things about the energy sector. While the push from the lows has been fairly strong in recent months, the ongoing downtrend remains intact. If the market does turn lower in the August/September period as expected the potential to retest lows is fairly high.

As shown in the longer term oil chart below, there is little to suggest a recovery back to old levels is in the offing anytime soon. With oil prices back to extreme overbought conditions, a retracement to $35 or $40/bbl would not be surprising particularly if, and when, the US Dollar strengthens. Remain underweight this sector as valuations for energy stocks have entered into “moon shot” territory.

Buy/Sell/Hold/Add: Hold (Take Profits)

Weighting: Underweight In Portfolio

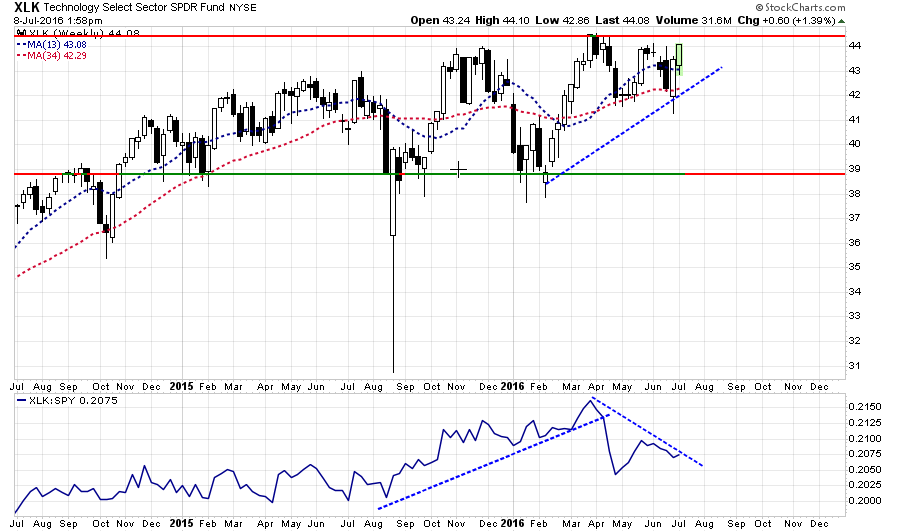

Technology

Like the Discretionary sector, Technology has been working a very quite uptrend. However, don’t get too excited just yet as this sector has been a weak performer as of late and remains encapsulated in a sideways trend. Hold positions for now and look for a breakout above resistance. If this happens we will re-evaluate our weighting recommendations.

Buy/Sell/Hold/Add: Hold

Weighting: Underweight In Portfolio

Real Estate

If the chart below looks like Utilities and Staples it shouldn’t surprise you. Another victim of the “yield chase” has been real estate which after breaking out above resistance has advanced sharply into extreme overbought territory. Take profits and reduce holdings back to original weighting levels.

Buy/Sell/Hold/Add: Hold (Take Profits)

Weighting: Portfolio Weight

Bonds

The real anomaly to all of this analysis comes to bonds. The recent surge higher in the markets should have taken the “wind” out of bond investors as money rotated from “safety” back into “risk.” That has not been the case which does “raise the hair” on the back of my neck.

The current “parabolic” advance is unsustainable and profits should be taken and positions reduced back to original weightings. (I seem to keep repeating myself) If you are long individual bonds with set maturities, you could consider using a “short interest rate” exchange traded fund to hedge your current bond portfolio as well.

Importantly, a push higher in both stocks and bonds is historically unsustainable. In other words, someone is going to be wrong. Let’s take some money off the table and wait and see who’s right.

Buy/Sell/Hold/Add: Hold (Take Profits)

Weighting: Portfolio Weight

Gold

In January 2013, I recommended selling Gold entirely out of portfolios. That has been a good call since then. The recent push higher in Gold, given the “Brexit” fears, has pushed prices back to the top of the long-term trend line. With the asset extremely overbought, long holdings should be trimmed back to original weights.

Furthermore, if the recent breakout in the markets holds, and the bull market does resume, then gold prices will fall back towards the bottom of the long-term trend channel. If gold does break out of the long-term downtrend, portfolio weightings will be reconsidered.

Buy/Sell/Hold/Add: Hold (Take Profits)

Weighting: Underweight In Portfolio

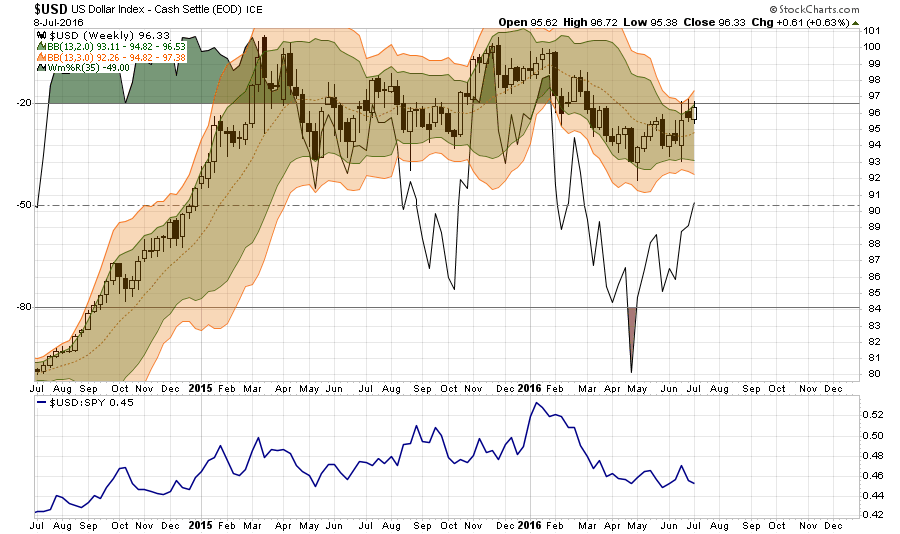

USD

The US Dollar is the key to potential outcomes. My expectations are that with the dollar coming off of oversold levels, a steady advance back to old highs is likely. This will particularly be the case as China, and its economy, slowly comes apart. This will negatively impact oil prices, energy stocks, corporate earnings and eventually the stock market itself. Pay attention to the dollar in the months ahead.