At the beginning of this year, I began discussing the technical weakness that was emerging in the markets. Since that time, the markets have remained under pressure leading to a continued cautious portfolio stance.

However, I have reiterated many times since then, interventions by Central Banks could change the shorter-term dynamic of the markets from bearish back to bullish. This past week saw exactly that as the European Central Bank not only intervened in the financial system but threw everything at its disposal at it. As noted by Ambrose Evans-Pritchard:

“Mr. Draghi pledged to flood the financial system with fresh liquidity for as long as it takes to keep the fragile economic recovery alive and prevent a deflationary psychology taking hold, yet there was a sting in the tail.

Marc Ostwald, from Monument Securities, said the ECB has bet everything on one last throw of the dice. ‘It’s a kitchen sink job, but at the same time Draghi is saying there is a limit to what they can do, that this is it, and there will nothing more,’ he said.”

The question, of course, is whether the ECB’s interventions will be able to change the longer-term dynamics in the Eurozone by creating inflationary pressures and sparking economic growth? That answer is likely “no” as it has failed to do so in the past, not only in the Eurozone but also in Japan and the U.S.

While I am going to spend most of this week’s missive re-evaluating the technical underpinnings of the market, I want to start with a quick review of the fundamentals.

EARNINGS STILL RECESSIONARY

As I noted earlier this week, corporate earnings continue to deteriorate.

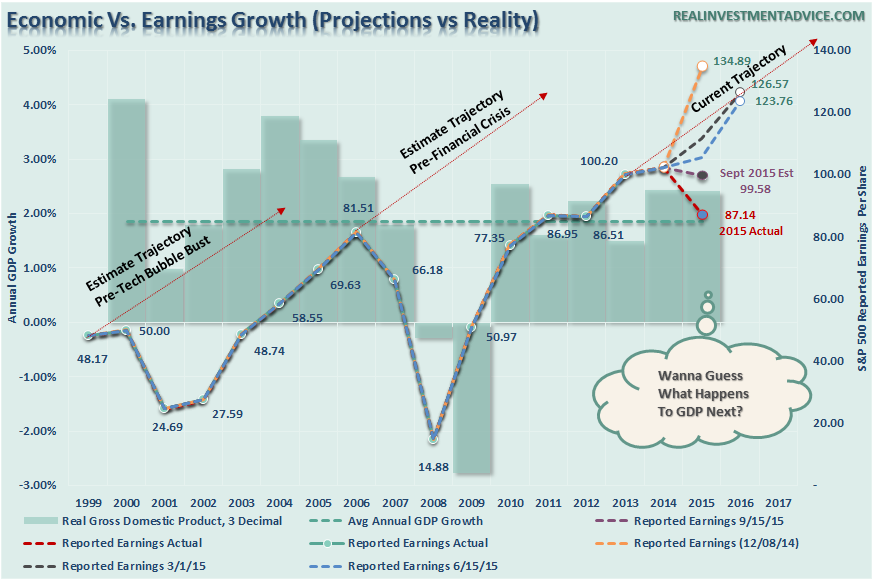

“The chart below compares economic growth to earnings growth. As shown above, Wall Street has always extrapolated earnings growth indefinitely into the future without taking into account the effects of the normal economic and business cycles. This was the same in 2000 and 2007. Unfortunately, the economy neither forgets nor forgives.”

“Unfortunately, it is only a function of time until the next economic downturn takes hold, particularly given the currently weak global outlook. As shown, earnings tend to cycle regularly between 6% peak to peak and 5% trough to trough growth in earnings. In 2014, expectations exceeded the current 6% peak to peak growth rate. I said then that it was only a question of what will trip up such overly optimistic picture. We now have that answer and real earnings have fallen far short of those original estimates.”

More importantly, despite ongoing Central Bank interventions which boost asset prices and acts as a huge wealth transfer tax from the middle class to the rich, corporate earnings are a direct reflection of what is happening in the actual economy.

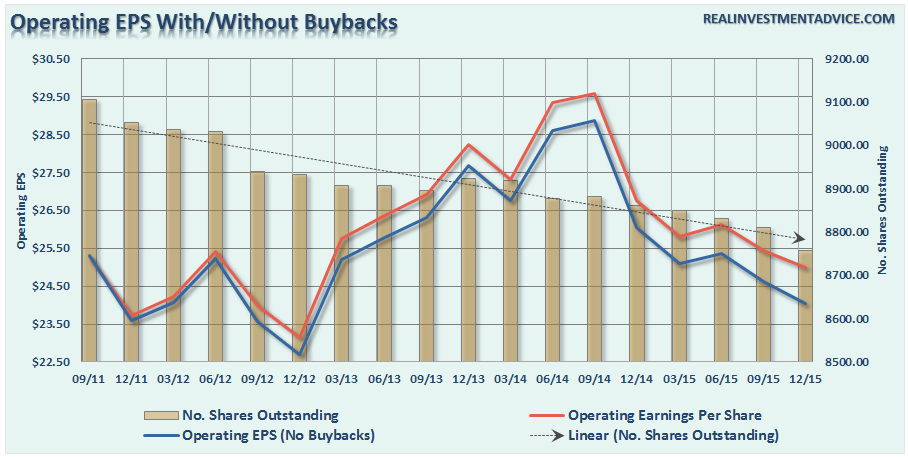

“Since 2009, the reported earnings per share of corporations has increased by a total of 206%. This is the sharpest post-recession rise in reported EPS in history. The problem is that the sharp increase in earnings did not come from a similar surge in revenue that is reported at the top line of the income statement. Revenue from sales of goods and services has only increased by a marginal 27% during the same period.”

“For profitability to surge, despite rather weak revenue growth, corporations have resorted to using debt to accelerate share buybacks. The chart below shows the total number of outstanding shares as compared to the difference between operating earnings on a per/share basis before and after buybacks.”

“The problem now is that despite share buybacks, earnings are no longer growing.”

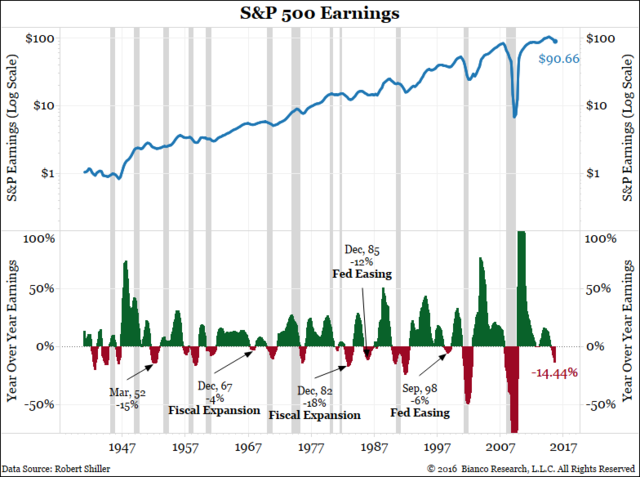

James Bianco from Bianco Research also notes:

“Our chart below starts in 1940 and shows Standard & Poor’s 500 Index earnings in the top panel and their year-over-year change in the bottom panel. The shaded areas highlight the 12 recessions over this period.”

“Earnings turned negative either during or just after all 12 of these recessions. This should come as no surprise. Also noted on the chart are the five instances when earnings turned lower (at least two consecutive quarters) without a recession.

Hence, the last time earnings turned lower without a recession, Fed easing or fiscal expansion was in 1952. So if we are going to be in a period of negative earnings in the absence of any of these, it would be the first time in more than 63 years.“

The point here is that Central Bank interventions likely can not fix that problem in the longer term. While liquidity injections have the ability to “Rob Peter To Pay Paul” by dragging forward future consumption, it continues to enlarge the future consumption void when it inevitably arrives.

ECONOMIC DATA NOT MUCH BETTER

The economic picture, not surprisingly, is not doing well either and, as stated above, is being reflected in current earnings growth.

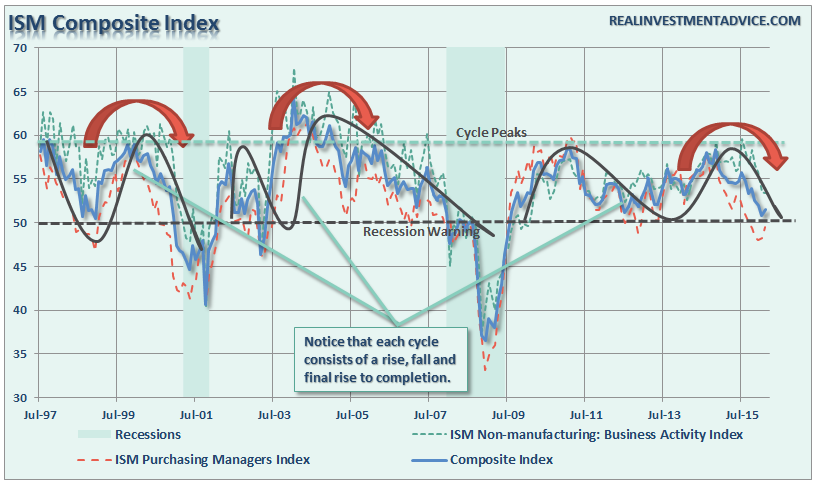

While many pundits have tried to suggest “this time is different” because the “service” sector has not fallen into contraction, this may be presumptive as the “trend” of the data suggests this is not the case.

The same can be seen in the Economic Output Composite Index (EOCI) which is comprised of a variety of broad indices including the Chicago Fed National Activity Index, Chicago PMI, several Fed regional manufacturing surveys, ISM composite, NFIB survey and the LEI. The last three times this index has fallen towards these current levels the Federal Reserve intervened.

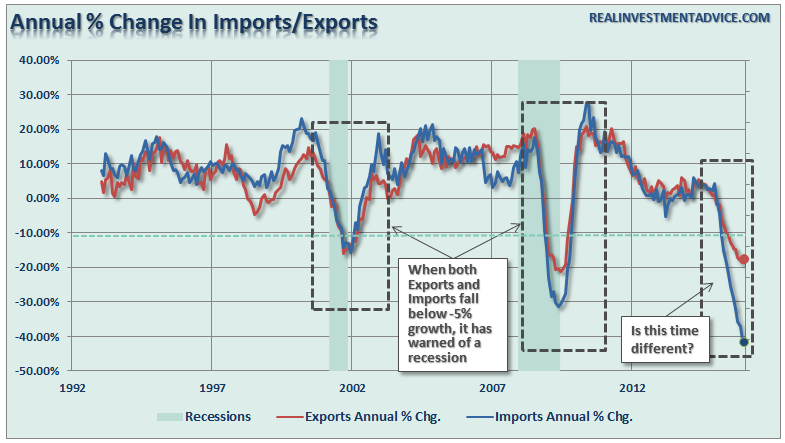

Lastly, imports and exports are the “blood” in the veins of both corporations and consumers. Exports make up roughly 4o% of corporate profits and imports show the strength of consumer demand. See any problems here?

Interestingly, even the ECB understands that liquidity interventions will not be effective in the long-term. As noted by William Watts at MarketWatch this week:

“With the effectiveness of monetary policy ‘clearly diminishing,’ Draghi ‘threw down the gauntlet to fiscal policy makers today, arguing for infrastructure spending while lowering the ECB’s own growth forecasts,’ said Alasdair Cavalla, economist at the Center for Economics and Business Research, a London-based forecasting and analysis firm.”

That help has not been, and will likely not be, forthcoming. As noted this past Sunday, BIS economists highlighted the fragile global economic backdrop and said negative interest rates could become a reality for many more countries as central banks search for ways to stoke real growth.

“The tension between the markets’ tranquility and the underlying economic vulnerabilities had to be resolved at some point. In the recent quarter, we may have been witnessing the beginning of its resolution.

We may not be seeing isolated bolts from the blue, but the signs of a gathering storm that has been building for a long time.“

Unfortunately, all one has to do is look at Japan to see the shortcomings and deteriorative impacts of negative interest rates.

TECHNICALS IMPROVE SHORT-TERM

While the economic and fundamental backdrop are still waving very important cautionary flags, the recent rally in the markets in anticipation of both ECB and Fed support have turned the technical backdrop more constructive. However, has enough repair been done to change our currently cautionary stance more bullish? Let’s take a look.

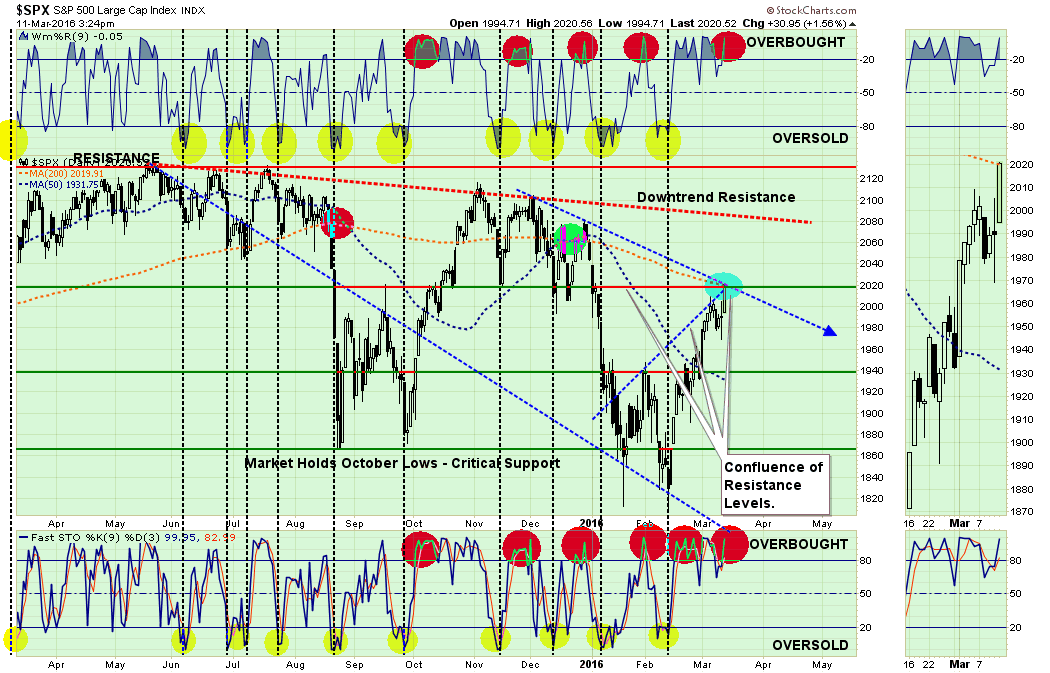

From a short-term, daily, perspective, the current rally is very similar to the one we saw last October following the summer swoon. The steepness of the ascent, amid continued overbought conditions, smacks of a short-covering rally and a scramble by markets for momentum.

Given the “accommodative” stances of Central Banks globally, the current rally runs well in the confines of a reflexive rally. However, as shown in the chart above the current bearish trend remains intact for now.

LONGER-TERM NOT SO MUCH

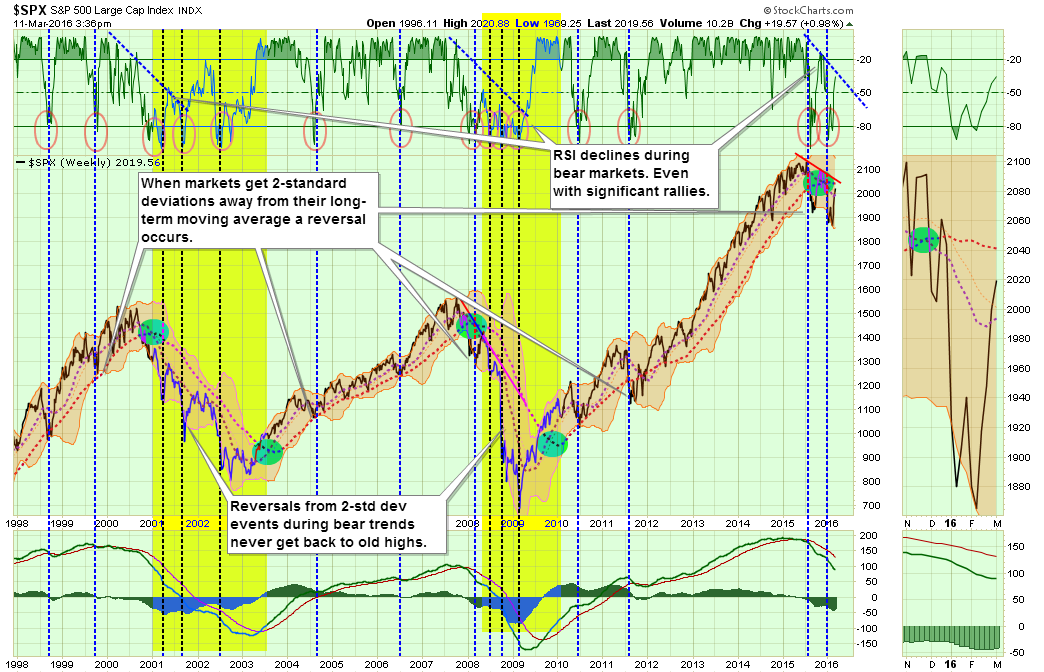

If we step back to an intermediate, weekly, perspective, a little clear perspective emerges. As shown below, while the recent rally has been extremely sharp, it is still confined to an overall negative price trend.

Starting at the top of the chart above, it is important to note the declining trend of the overbought/sold indicator. The yellow highlights denote previous bear market cycles where the markets remained primarily oversold during the entirety of the reversion process.

Moving to the bottom of the chart, there has been NO IMPROVEMENT in the intermediate “sell” indicator which also suggests that the current rally remains confined within an ongoing bear market trend. Note that this indicator has only been this negative during the previous two bear market cycles.

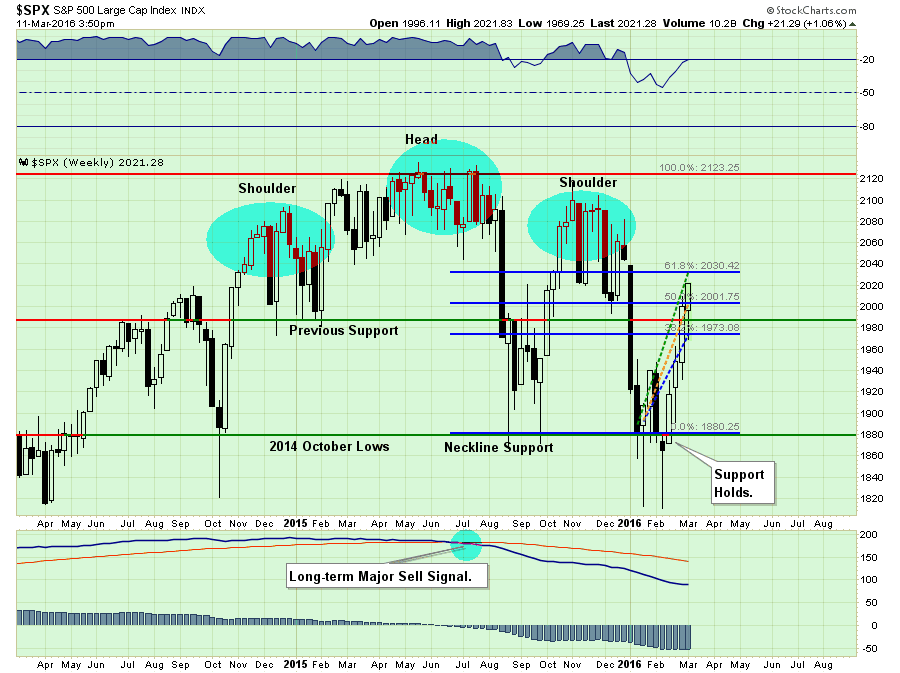

Also, as I discussed last week, the current rally is still within the context of a standard Fibonacci retracement. The target of 2030, which I laid out in January of this year, is now being approached.

It is worth noting what I said way back then:

“It is that very oversold condition that has continually suggested that something would happen to elicit a short-term retracement in the market. Not to be disappointed it was the promise of more liquidity by the ECB and Mario Draghi that elicited a massive short-covering rally on Friday.”

As you will notice, that rally failed and actually broke previous lows. It was then the BOJ’s turn to provide support for the market, more promises from the G-20 and finally action from the ECB. Again, this rally looks an awfully lot like last October, but with with much weaker economic and fundamental underpinnings.

“You just have to ask yourself one question. Do I feel lucky? Well, do ya punk?” – Clint Eastwood, Dirty Harry

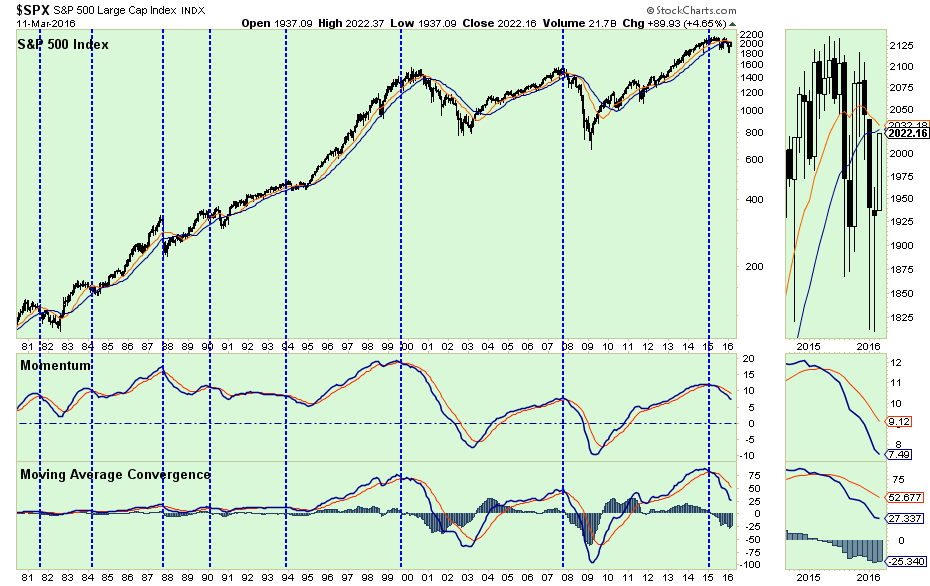

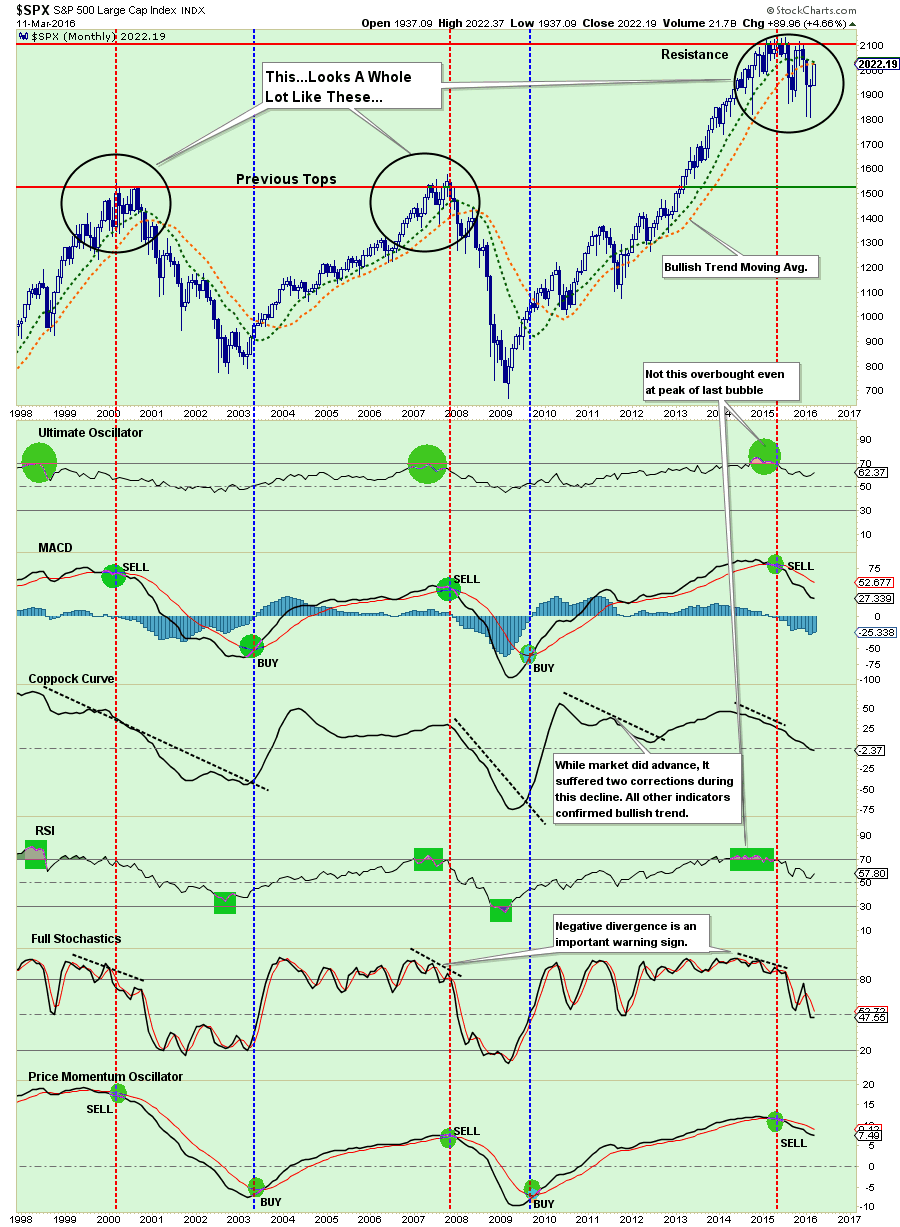

Stepping out even further, on a very long-term, monthly, picture we see even less evidence the current advance is changing from a negative trend. The first chart shows the primary “sell” indicators going back to 1980. When the two lower indicators have aligned previously on a negative crossover, it has corresponded with either an intermediate-term correction in the market, a 1987-crash, or worse.

The final long-term chart confirms the same showing a uniform alignment of all technical underpinnings showing NO IMPROVEMENT following the recent rally.

In order for the market to change the current negative dynamics, which in turn would warrant a significant increase in long-term equity exposure, it will require a uniform improvement in the technical underpinnings and likely a breakout to all-time highs.

Is such a turn possible? Absolutely.

Is it probable? Given the deterioration in economic, fundamental and technical backdrops, my best guess is “no.”

But again, anything is possible and the question you have to ask yourself is:

“Do you feel lucky?”