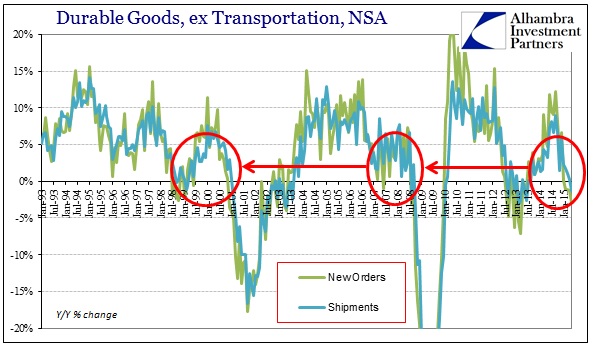

Durable goods orders and now shipments continue to be a serious drag on the overall economy. On a year-over-year basis, shipments joined orders in contracting for both durable goods (ex transportation) and capital goods. For some, there was a glimpse of hope in that the seasonally-adjusted category of new orders for capital goods rose in May, but that was, as retail sales, in sharp contrast to the unadjusted comparison.

The Commerce Department said on Tuesday non-defense capital goods orders excluding aircraft, a closely watched proxy for business spending plans, rose 0.4 percent last month. These so-called core capital goods orders slipped 0.3 percent in April.

Manufacturing has been pressured by investment spending cuts in the energy sector in the aftermath of a more than 60 percent plunge in crude oil prices last year, as well as dollar strength.

The view that seems to be supplanting the previous narrative about the “unquestionable” recovery is that mysterious weakness can be found – but only in limited experience.

“The bottom line is that equipment investment is one of the few expenditure components that isn’t showing signs of a marked rebound in the second quarter,” Paul Ashworth, chief U.S. economist at Capital Economics, said in a note to clients.

Maybe that is progress in a certain light, as in the space of about half a year the “narrative” has transited from universal recovery and boom to transitory anomaly again in weather to lingering but isolated economic illness. Subtle and lagging is this shift, but it is noticeable and that is significant in and of itself as it amounts to further refuting last year’s surety on economic direction.

In fact, from a very broad perspective, the behavior of durable goods and especially capital goods is every bit consistent with economic performance in 2015. You can take the declines in capital goods directly from the capacity utilization figures provided by the Federal Reserve; businesses that see a sudden drop in utilization rates are not going to be keen on ordering and buying new equipment. And if capacity has suddenly become excess, then the massive inventory overhang is undoubtedly responsible for that; all of which traces back to the quite clear consumer recession that has now stretched into May, months beyond where weather and “anomalies” were hanging.

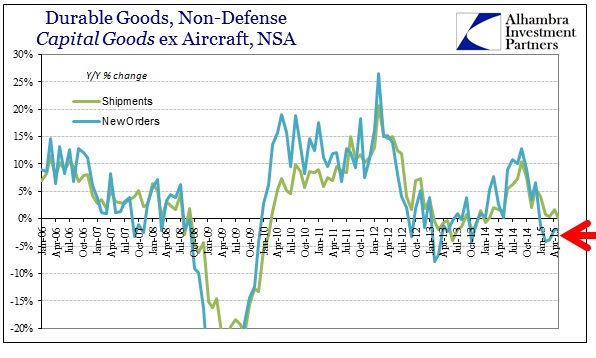

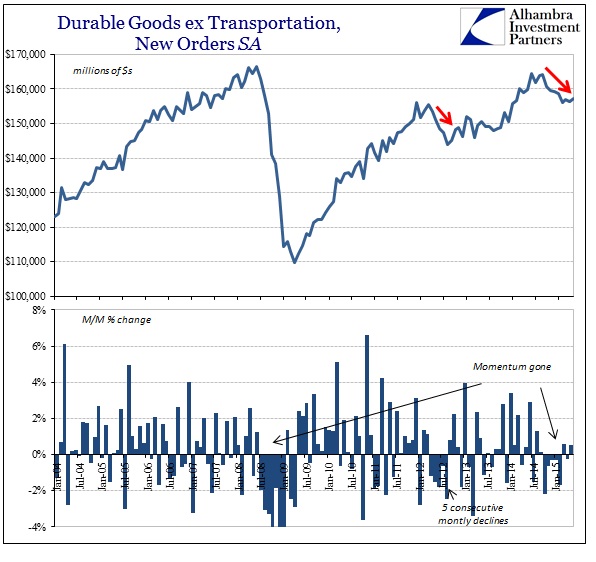

This is the first time since early 2013, in the aftermath of the 2012 slowdown, where all four categories (durable goods and capital goods, new orders and shipments) are all contracting. That would suggest that, no, there isn’t any rebound and that the distress is more widely impugning than just limited manufacturing. The behavior of new orders, especially, as well as the timing of that behavior precludes manufacturing and business investment being isolated in terms of “mystifying” weakness.

This is the first time since early 2013, in the aftermath of the 2012 slowdown, where all four categories (durable goods and capital goods, new orders and shipments) are all contracting. That would suggest that, no, there isn’t any rebound and that the distress is more widely impugning than just limited manufacturing. The behavior of new orders, especially, as well as the timing of that behavior precludes manufacturing and business investment being isolated in terms of “mystifying” weakness.

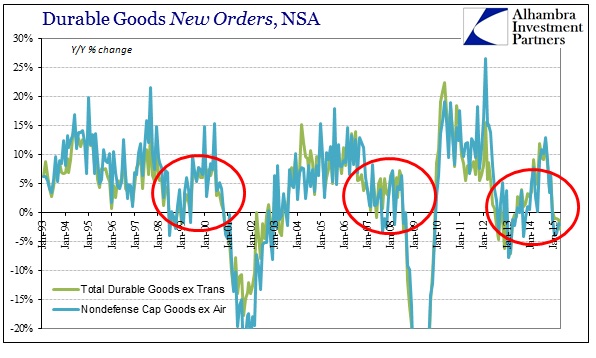

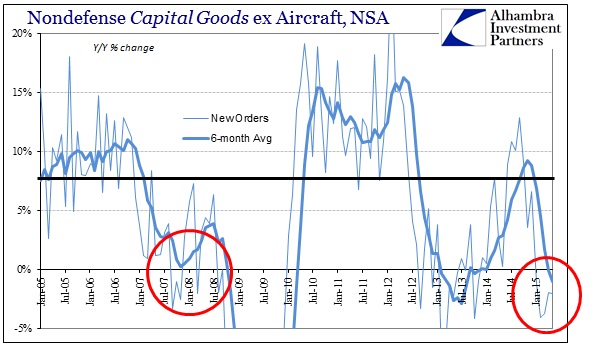

Except for the magnitude of the upward interlude, the current pattern in new orders is remarkably similar to the Great Recession as well as the months prior to the dot-com recession. The commonality may be linked to expectations (false) over monetary “stimulus” measures; in the case of the dot-com recession and Great Recession, they were in the form lower interest rates; in the current case, QE3 and QE4. Ultimately, such expectations amounted to misplaced faith, and may have, in certain senses, actually contributed to the contractions where businesses ordered for monetary success only to be left with larger imbalance when it never arrived(s).

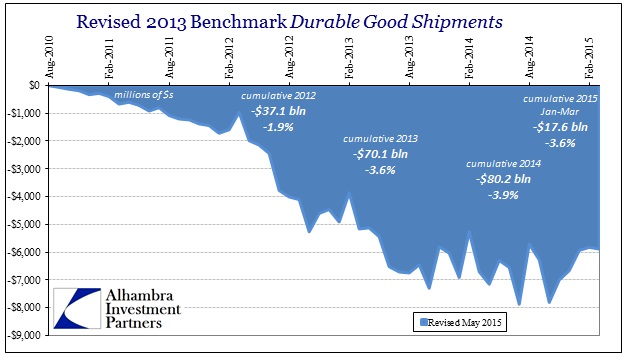

This comes after the major 2013 benchmark revisions (linked to the 2012 Economic Census) which showed a far-too-optimistic statistical regime in the first place. In the other words, the economy and “demand” are a lot less than believed prior, and that it is again shrinking outright; the smaller economy becomes even smaller.

Even the seasonally-adjusted series provides less optimism about the future direction than is given in the mainstream commentary. Q2 may not still be shrinking here, but it certainly isn’t growing either. That is a huge problem because, again, recession is not the actual direction, at first, but the accumulation of opportunity cost gone by. Even sentiment surveys are beginning to warn now about Q3 after Q2 failed to live up to showing Q1 as an aberration. In the disappointing US PMI for June, Markit notes:

The latest expansion of production volumes was the weakest recorded by the survey since January 2014. Some manufacturers cited greater efforts to fulfil orders from inventories in June, as highlighted by the first reduction in stocks of finished goods since December 2014. Moreover, there were reports that softer output growth reflected a degree of caution about the business outlook, as well as concerns about the impact of the strong dollar on competitiveness…

Manufacturers reported a disappointing end to the second quarter, with factory output growing at the slowest rate for a year-and-a-half.

While the survey data points to the economy rebounding in the second quarter, the weak PMI number for June raises the possibility that we are seeing a loss of momentum heading into the third quarter.

Taken together, manufacturing slumped significantly in Q1, rebounded by the smallest amount (and only in the seasonally-adjusted view) which would qualify for the term in Q2, and is now already looking downward into Q3. By that count, manufacturing better be isolated as a negative pressure, for if it is consistent with everything else then that amounts to a very troubling H2 that hasn’t yet begun.