The latest iteration of the Fed’s meeting minutes is surreal. Its another economic weather report consisting of trivial, random observations about the quarter just ended that are as superficial as CNBC sound bites. Along with that prattle comes guesses and hopes about the next 30-90 days—including the expectation that the weather will “seasonally normalize” and that auto production schedules, for instance, which were down in March, will stabilize at that level “in the months ahead”.

Likewise, after noting that consumption spending moved “roughly sideways” during January and February, it detected that “recent information on factors that influence household spending were positive”—-a guess that turned out to be wrong based on data we already know from April retail sales. The data on new and existing home sales had indicated the continuation of a 5-month trend of sharp drops from prior year, but the minutes could muster only an on-the-one-hand-and-on-the-other-hand whitewash, accented with hopeful indicators on single-family permits and pending home sales.

Business investment was treated the same way—that is, it was down in the first quarter but “modest gains” are expected soon based on sentiment surveys. And as you read further the noise just keeps getting more foolish, including the hope that the negative net export performance in Q1 would be off-set by improving global developments. That fond hope included this doozy: “In Japan, industrial production rose robustly, and consumer demand was boosted by anticipation of the April increase in the consumption tax.”

That particular phrase actually translates into big speed bumps ahead, but that’s beside the point. What this item and all of the rest of the commentary amounts to is bus driver chatter about road conditions at the moment. Stated differently, the monetary politburo does indeed believe that it can steer our $17 trillion economy on a month-to-month basis, and attempts to do so with primitive “in-coming” data from the Washington statistical mills that is so tentative, imputed, guesstimated, seasonally maladjusted and subsequently revised as to be no better than anecdotal sound bites.

Worse still, it pretends to be executing its monetary central planning model without any of the “gosplan” tools that would really be needed to drive the thousands of variables and millions of actors which comprise an open $17 trillion economy that is deeply intertwined in the trade, capital and financial flows of the world’s $75 trillion GDP. Alas, its one size fits all control panel includes only interest rate pegging, risk asset propping and periodic open mouth blabbing by Fed heads.

But these are no longer efficacious tools for driving the real Main Street economy because to boost the latter above its natural capitalist path of productivity and labor hours based growth requires artificial credit expansion—that is, a persistent leveraging up of balance sheets so that credit bloated spending rises faster than production and income.

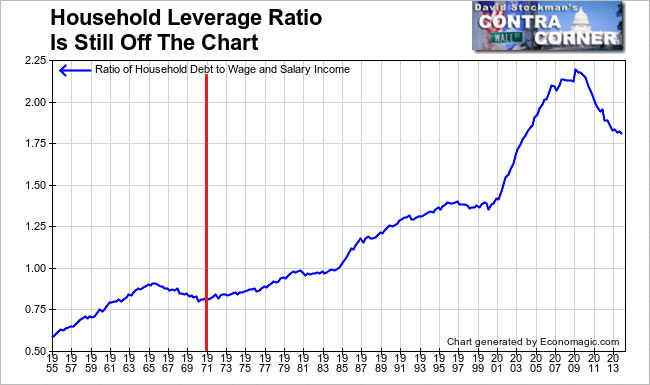

As should be evident after six continuous years of frantic money pumping that old secret sauce doesn’t work any more because the American economy has reached a condition of peak debt. During the Keynesian heyday between 1970 and 2007 the nation’s total leverage ratio—that is, total public and private credit market debt relative to national income—soared right off the historic charts, rising from a 100-year ratio of +/- 150% of national income to a 350% leverage ratio by 2007.

Since the financial crisis, the components of national leverage have been shuffled from the household sector to the public sector, but the ratio has remained dead in the water at 3.5X. That means that contrary to all the ballyhoo about deleveraging, it has not happened in the aggregate, but where it has happened at the sector level actually proves that the Fed’s credit transmission channel is over and done.

Total non-financial business debt has risen from $11 trillion to $13.6 trillion since the financial crisis, but virtually all of that gain has gone into shrinkage of business equity capital—that is, LBOs, stock buybacks and cash M&A deals which levitate the price of shares in the secondary market, but do not fund productive assets and the wherewithal of future growth. In fact, as of Q1 business investment in plant and equipment was still nearly $70 billion or 5% below its late 2007 peak.

In the case of the household sector, the 40-year sprint into higher and higher leverage ratios has reversed and is now significantly below its peak at 220% of wage and salary income in 2007. At 180% today household leverage is off the mountain top—but it is still far above historically healthy levels, especially for an economy with rapidly aging demographics and soaring ratios of dependency on government benefits that requires tax extraction from debt-burdened households or debt levies on unborn taxpayers.

So the traditional credit expansion channel of Fed policy is busted, but the monetary politburo is like an old dog that is incapable of learning new tricks. It plans to keep money market rates are zero for seven years running through 2015 on the misbegotten notion that it can restart America’s unfortunate 40-year climb into the nosebleed section of the debt stadium.

That isn’t happening, of course, but the $3.5 trillion of new liquidity that it has poured through the coffers of the primary bonds dealers since September 2008 has not functioned like the proverbial tree falling in an empty forest. Just the opposite. It has been a roaring siren on Wall Street—guaranteeing free short-term money to fund the carry trades, while providing a transparent “put” under the price of debt and risk assets. In short, it has fueled the Wall Street gambling channel like never before in recorded history.

Do the Fed minutes evince a clue that six years into this frantic money printing cycle that speculation, financial leverage strategies and momentum chasing gamblers are setting up for the next bursting bubble. Well no. Aside from pro forma caveats about possible future financial risks, the minutes claimed that all is well in the casino:

“In their discussion of financial stability, participants generally did not see imbalances that posed significant near-term risks to the financial system or the broader economy….

Perhaps they did not review the two charts that follow. Both are ringing the bell loudly to the effect that we are reaching the same bubble asymptote—or curve that has reached its limit— as was recorded right before the crashes of 2000-2001 and 2007-2008.

The margin debt explosion is especially significant because it had reached a higher ratio to GDP (2.73%) than either of the two pervious bubble cycles. Back in the day of William McChesney Martin, the Fed watched margin debt like a hawk because it was comprised of veterans of the 1929 crash. Accordingly, they did not hesitate to take preemptive tightening actions when speculation began to get out of line, such as in the summer of 1958. But this month’s meeting minutes did not even take note of the margin data.

To be sure, it is always possible to claim that the broad market is trading at “only” 15X the forward earnings of the S&P 500 at $123/share. But that’s ex-items and from analyst hockey sticks which always get sharply reduced as the future actually materializes. In that respect it is notable that at this very point in the bubble cycle during October 2007, S&P forward earnings were projected at $118/ share for 2008 or 15X; they actually came in at $55/share on an ex-items basis, and a scant $15/share after a half decade of phony profits were written of by banks and non-financial business alike.

In any event, the landscape is riddled with froth and unsustainable speculation everywhere, but most especially in the world of junk credit where the final blow-off has occurred in each of the last three bubble cycles. All the usual suspects are there including record junk bond issuance, soaring expansion of the debt-on-debt-on-debt Wall Street vehicles known as CLOs—along with “cov lite” loans and leveraged recaps whereby the LBO kings pile more loans on portfolio companies already groaning under massive debt in order to pay themselves a fat dividend.

And then the tentacles of junk credit expand far and wide. Sub-prime auto debt is at nearly 2007 peak levels, and now another flavor has emerged: Subprime business debt whereby struggling shopkeepers and home-gamers are invited to pay up to 100% annualized interest to keep the doors open a few more months.

Finally, there is the ultimate in sub-prime—-student debt that has now reached $1.1 trillion, and which already sports default rates in excess of 30% among borrowers who are actually in repayment status.

Monetary central planning at the zero bound embodies a destructive internal contradiction. It inherently generates rampant speculation in real estate and financial assets because ZIRP massively subsidizes the cost of carry. At the same time, its practitioners are institutionally disposed to bubble denial because they falsely believe that their policies are what is keeping the real economy advancing–even if currently it is at a sub-normal pace by historical standards.

Without fail, therefore, monetary central planners keep their feet on the accelerator to the very end, boasting that the “in-coming data” shows the macro-economy approaching the nirvana of full-employment. What they are actually doing, however, is driving the financial system to unsustainable extremes of valuation and speculation— and eventually to a crash landing. We have had two of these processions of the lemmings—that is, Fed driven cycles of bubble inflation and bust—- already in this century. Now we are at the asymptote of the third.