BOJ COMES TO THE RESCUE

This week reminded me of the recent AFC Championship game as the Denver Broncos defeated the New England Patriots in the final seconds of the game by foiling the 2-point conversion attempt. The market, like the Patriots, struggled all week with any ground gained one day, lost the next.

Fortunately, for investors, instead of the final play of the game being an interception sending the Patriots into defeat, it was the BOJ completing the conversion and sending the “Bulls” on a rampage on Friday.

However, the announcement by the Bank of Japan (BOJ) to implement negative interest rates in a desperate last attempt to boost economic growth in Japan was only the catalyst that ignited the bulls. The “fuel” for the buying came from the end of the month portfolio buying by fund managers. As I wrote Thursday evening:

“But where could that lift come from? The first is month-end window dressing by fund managers after a brutal start to the new year. After much liquidation, fund managers will need to rebalance holdings.

The second is the potential for Central Banks to intervene which could embolden the bulls as further support could temporarily delay the onset of a bear market and recession. Note: I said temporarily. Pulling forward future consumption is not a long-term solution to organic economic growth.

Not to be disappointed, the BOJ announced a move into NEGATIVE interest rate territory to try and boost economic growth in Japan. (Interestingly, however, was the lack of increase in QE.) The announcement was a shock to the markets as the BOJ had just stated last week that negative interest rates were not being considered.”

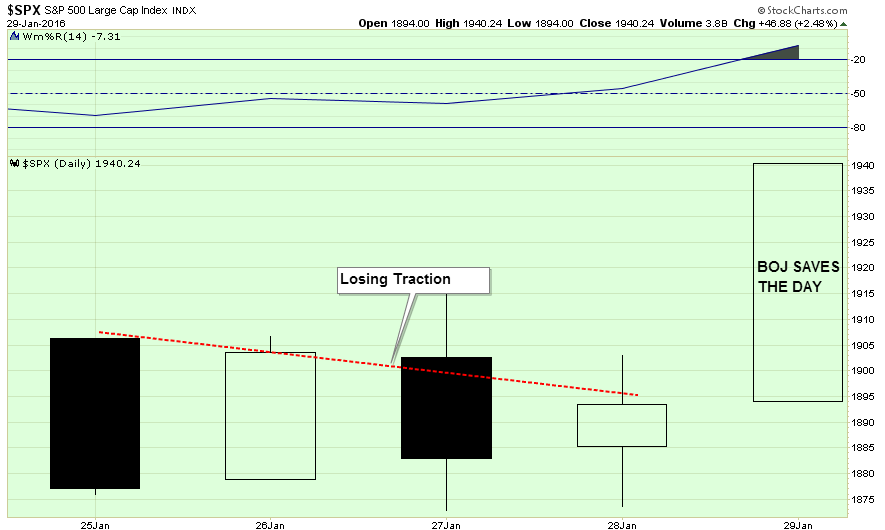

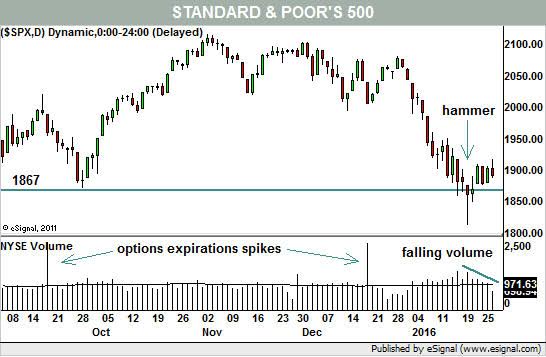

Importantly, the rally pushed the major averages out of the consolidation pattern that had me worrying on Wednesday about the possibility of a technical breakdown. To wit:

“Over the last few weeks, I have suggested the markets would likely provide a reflexive rally to allow investors to reduce equity risk in portfolios. This was due to the oversold condition that previously existed which would provide the “fuel” for a reflexive rally to sell into.

I traced out the potential for such a reflexive rally two weeks ago as shown in the chart below.”

(Chart updated through Friday’s close)

The most important parts of the chart above are the overbought / oversold indicators at the top and bottom. The oversold condition that once existed has been completely exhausted due to the gyrations in the markets over the last couple of weeks. This leaves little ability for a significant rally from this point which makes a push above overhead resistance unlikely.

“Just as an oversold condition provides the necessary “fuel” for an advance, the opposite is also true.”

SO, HERE IS THE QUESTION

Have the “bulls” have regained control of the markets OR is this THE RALLY we have been looking for to reduce portfolio risk into?

I can honestly say I do not absolutely KNOW for certain, but the internals of the market still suggests a “bear market” remains intact currently. This is an important point. All bull markets end as well as bear markets. The important thing to know are the rules that apply to each.

- In bull markets – buy dips

- In bear markets – sell rallies.

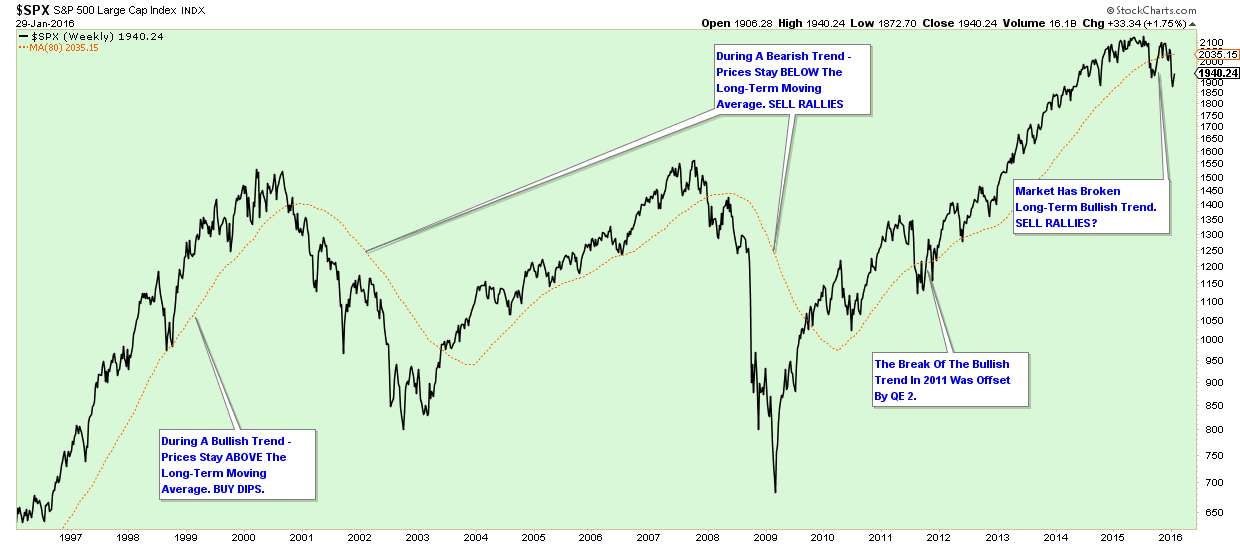

The chart below shows the distinct price trend channels of both bull and bear markets.

During bull markets, prices remain in a steadily rising price trend. This keeps prices trading above a RISING long-term moving average as shown in the chart above. During a bear market, prices remain in a steadily falling price trend. This keeps prices trading below a DECLINING long-term moving average.

During a rising price trend, “buying dips” is a profitable process. However, during a falling price trend, “buying dips” is hazardous to your financial health.

While being “bullish” is always much more “fun,” it does you little good to be “bullish” during a negative price trend in the market. Currently, the market has once again broken its long-term bullish price trend. Without the Federal Reserve intervening, as they did in 2011, there is little reason currently to expect the market to regain its bullish footing in the near-term. Until the price trend changes, this market is exhibiting all the traits of a decline price trend. Therefore, we sell rallies until the price trend changes.

This idea of a declining price trend was also a point made by Michael Kahn via Barron’s last week:

“While the S&P closed below the critical 1867 level outlined here last week, it did not stay there. It was a false breakdown as the index moved higher the next day.

That got bullish juices flowing. After all, a reversal pattern, failed breakdown with heavy volume at a key support level combined for a potential bullish turn (see Chart 1).”

“Unfortunately, over the next few days the stock market saw nothing but volatility and very little net progress, at least in the context of what usually happens when the market forms a “V” bottom. Named for the market’s quick fall and equally quick rebound, it is supposed to be a sharp turnaround. Look back at the sharp rebound in October 2014 following the Ebola panic as a great example of the “V.”

But volume since the reversal day presents a problem as it has been falling on both the New York Stock Exchange and on the Nasdaq ever since. That is more of a marker for a bounce in a falling trend than evidence of a change in market mood. If this were truly a bottom then we should see more volume, not less, as bottom-fishing turns into true buying power.“

Absolutely.

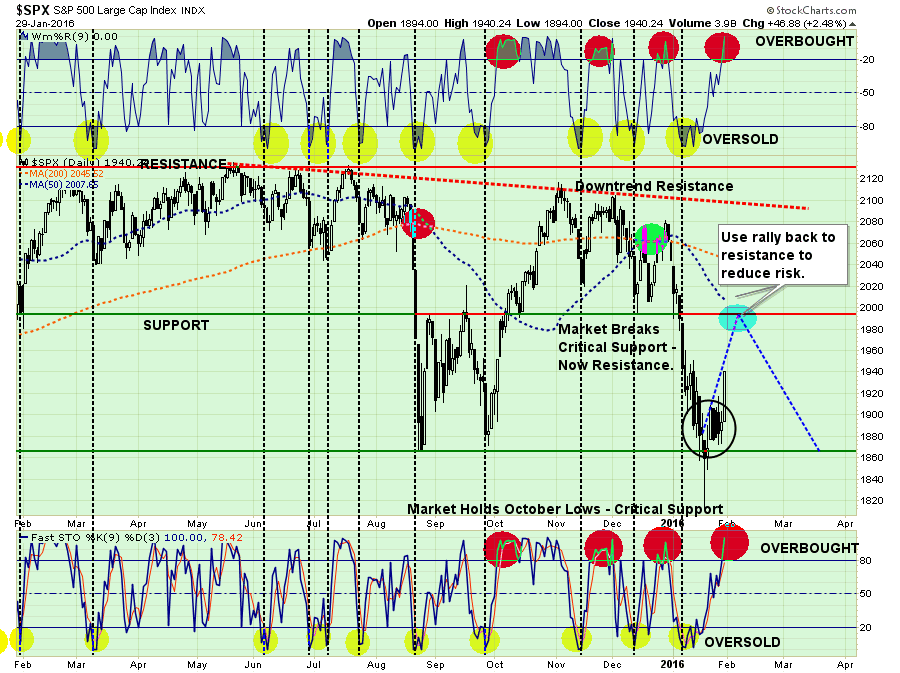

INTERNALS STILL SUGGEST CAUTION

However, let’s step away from price trend analysis for a minute and look at some of the internal measures of the market for more clues.

If the S&P 500 is the “body” of the market, we can look at things that make up the “health” of the market for signs of illness. In much the same way that your body aches and you get “the sniffles” before the onset of a cold, the markets begin to exhibit similar symptoms warning on an impending decline.

Let’s take a look at a few of the more important ones.

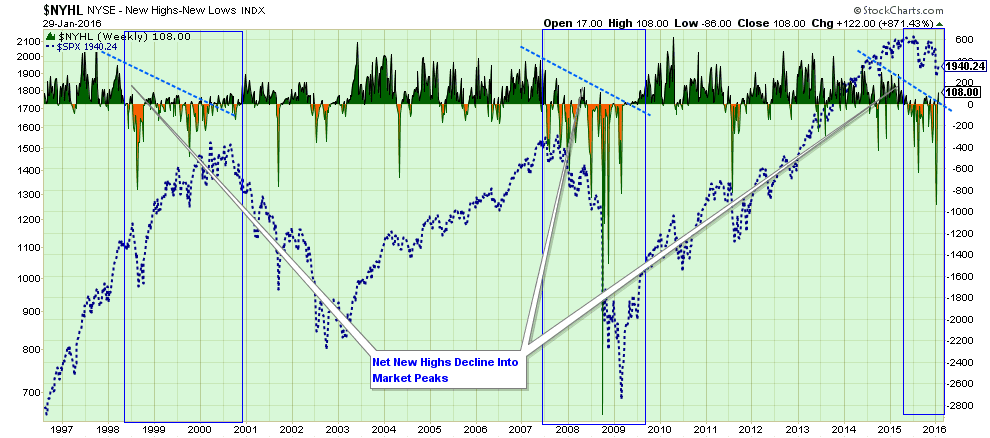

The first chart below is the number of stocks hitting new highs versus new lows on the New York Stock Exchange.

The blue boxes show a similar pattern during bear market declines where more stocks continue to trade at new lows than new highs. Something we are currently witnessing.

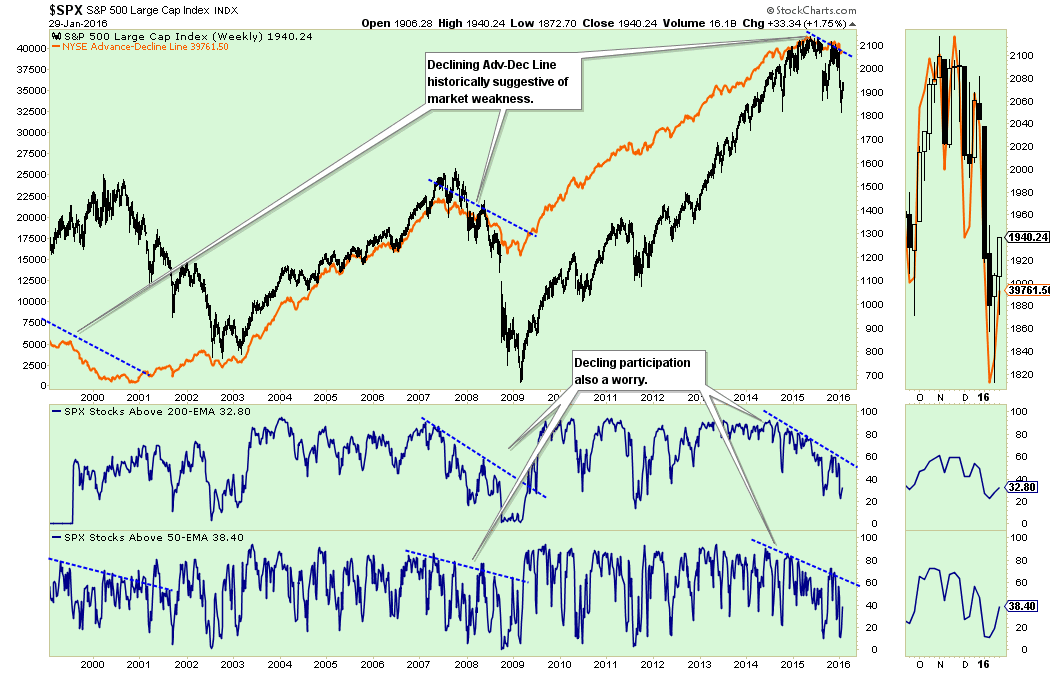

Another way to look at the health of the market is the number of stocks that are currently advancing in price versus those declining. Once again, we see a similar pattern emerging where the declining ratio of advancing stocks signals a more bearish trend in the market.

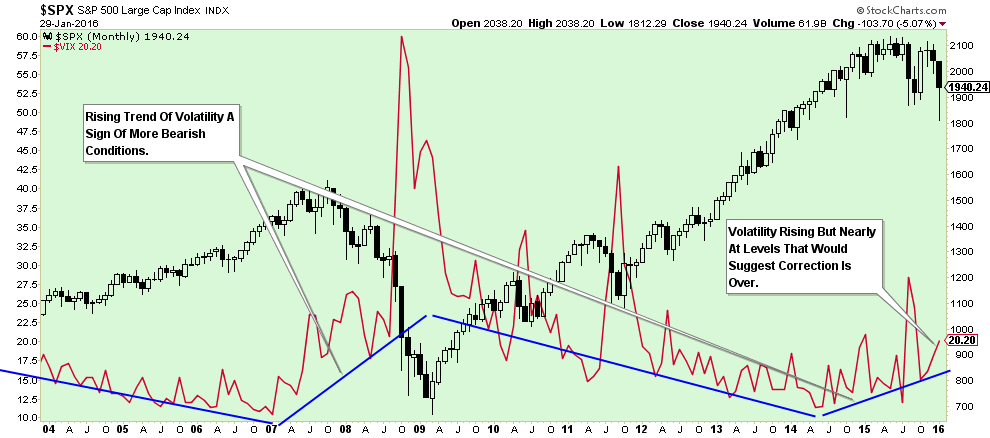

Volatility has also been trending higher. As shown in the chart below, while volatility has been on the rise, a trend last seen just prior to the last major correction, current levels of volatility suggest that the markets have not reached a level of “panic” that would denote the end of a bear market.

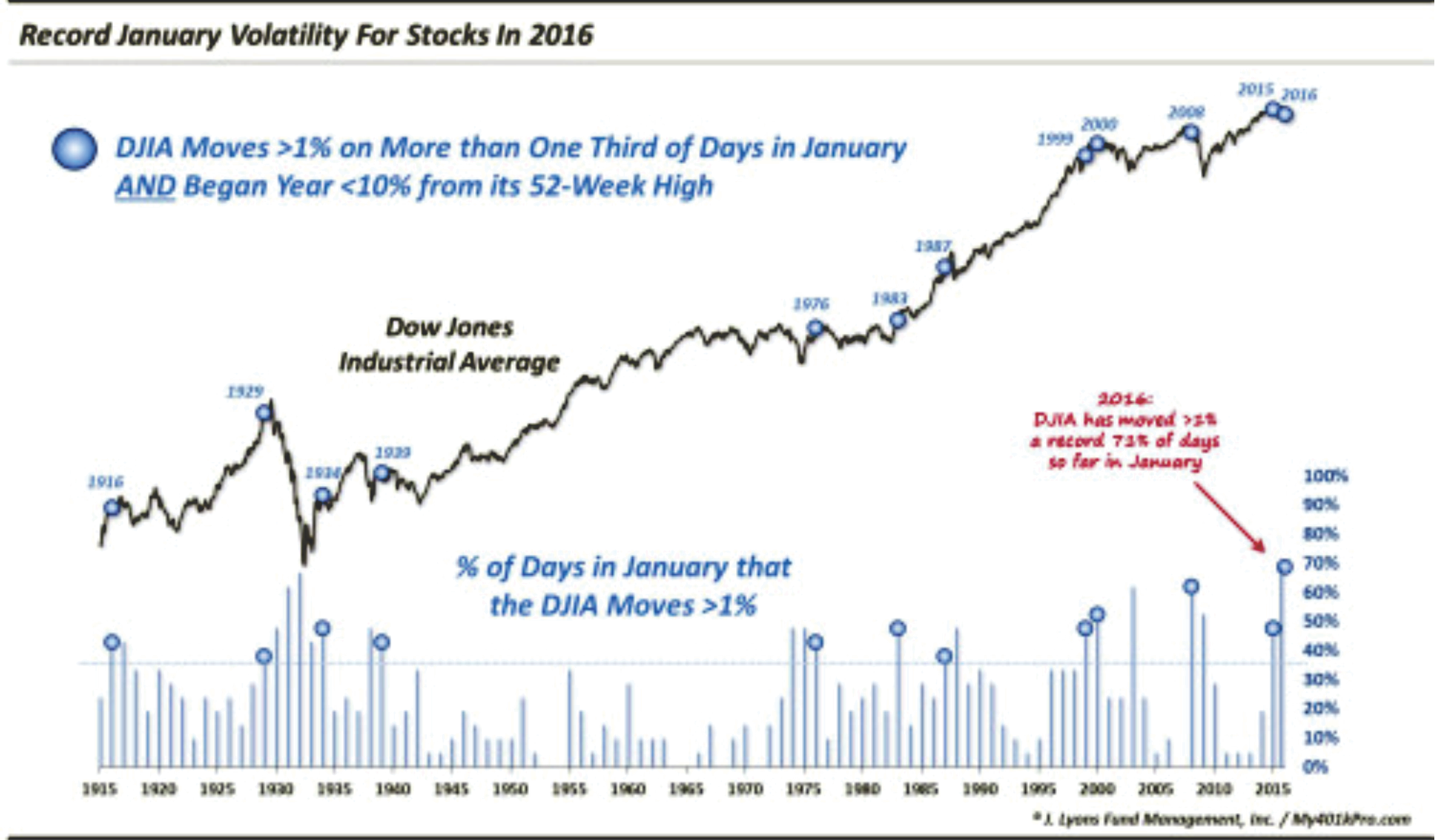

Dana Lyons also made a very interesting observation about January volatility spikes last week:

“First of all, 9 of the 11 occurred within the confines of a secular bear market (FYI, our view is that the market is still likely in the post-2000 secular bear so we are including 2015 in that category). Only 1983 and 1987 took place in a secular bull. And while the market fared just fine in the years following those two, 1987 did bring a little surprise later in the year. All in all, however, these volatile January’s that occurred relatively close to the DJIA’s highs did not lead to very attractive returns over the long-term.”

Furthermore, and this is a point that has been hit on frequently as of late by the media, is the collapse of the high-yield market. It is currently being dismissed as being all energy-related, however, in the past it hasn’t really mattered. Once the “fear of contagion” begins, the subsequent rout will be devastating.

Importantly, the collapse in the high yield market also affects two of the major underpinnings of the markets rise over the last couple of years in particular: debt-funded stock buybacks and M&A.

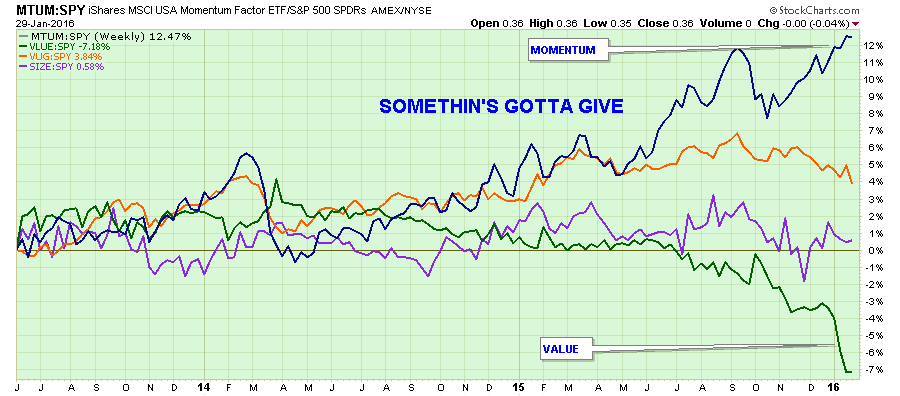

Lastly, in late stages of bull markets, the chase of “Momentum” stocks continues to build. As the number of stocks rising narrows, know as breadth, the ultimate reversion has been historically rather nasty. Currently, we are seeing a rather fantastic deviation between Momentum and Value stocks. Something will eventually give.

STILL A “SELL THE RALLY” MARKET

As I laid out last week, the markets were oversold enough on a short-term basis to have a fairly healthy reflexive rally. With the internals of the market still weak, along with the economic and fundamental backdrop still deteriorating, there is little reason to believe the market has completed its corrective process.

As shown in the chart below, the levels identified last week remain good targets for taking some risk management actions in your portfolio.

1970ish – Sell laggards and losers in portfolios. Take profits in winners and raise some cash as a hedge against further volatility. (I would do the bulk of your risk management in this zone as I don’t currently expect the market to be able to achieve the next two levels.)

2000ish – Continue rebalancing portfolios to reduce risk. Take profits and sell losers.

2030ish – Be at final risk-adjusted allocations.”

IMPORTANTLY: Notice the market has now traced out a fairly definitive “head and shoulder” technical pattern similar to that seen in 2008. If this rally fails, and breaks neckline support at recent lows, the market will be in a confirmed bear market.

WE ARE NOT IN A BEAR MARKET…YET

I want to close with this.

“We Are NOT In A Bear Market…Yet.”

However, as an investor, if you wait for confirmation of an official bear market, more than half of the damage to your portfolio will already be done. (Confirmed bear is when the market is down 20%, the average historical bear market / recession is down 33%)

What you decide to do is up to you, however, if you look at your portfolio and see holdings down 20, 30, 40 or 50%, shouldn’t you ask yourself why? The math of making up those losses will take an exceptionally long amount of time which means you have capital that is no longer working to further your financial interest. Making up losses has never been a strategy for building wealth. This is likely a good time to reassess how you, or your advisor, is managing your money.

No, we are not in a bear market yet. However, there are more than enough signs that suggest one may be stalking us.

Besides, the last guy I saw get mauled by a bear didn’t look so good afterward.

(Leonardo DiCaprio in the Revenant)

Have a great week.

THE MONDAY MORNING CALL

As stated above, the markets are finally providing the bounce that we have been waiting for patiently over the last three weeks. (I admit I was getting awfully worried that we might not get one, but this is why patience and an adherence to a disciplined strategy generally pays off longer term. It will not always work exactly as intended, but more often than not it will.)

As identified above, the initial target to begin reducing portfolio risk and rebalancing portfolios will be in the area of 1970 on the S&P 500. Importantly, note the word AREA. One of the mistakes individuals consistently make is picking a specific price point to take action. The problem is, so are many others. I have seen investors repeatedly fail to take action, ultimately to their disappointment, because a precise number didn’t get hit.

Don’t get tripped up waiting for 1970 precisely to take action. If the market fails and turns lower, you will have wished you had done something as the next opportunity may be at lower levels.

Working With A Model Allocation

NOTE: The following is for example purposes ONLY. It is in no way a suggestion, recommendation, or implication as to any portfolio allocation model currently in use. It is simply an illustration of how to overweight or underweight a model allocation structure.

Again, this is just for educational purposes, and I am not making any specific recommendations. This is simply a guide to assist you in thinking about your own personal position, how much risk you are willing to take and what your expectations are. The closer you want to track the S&P 500 Index, the less fixed income, real estate and cash your portfolio should have. For a more conservative allocation reduce allocations to equities and add more to cash and fixed income.

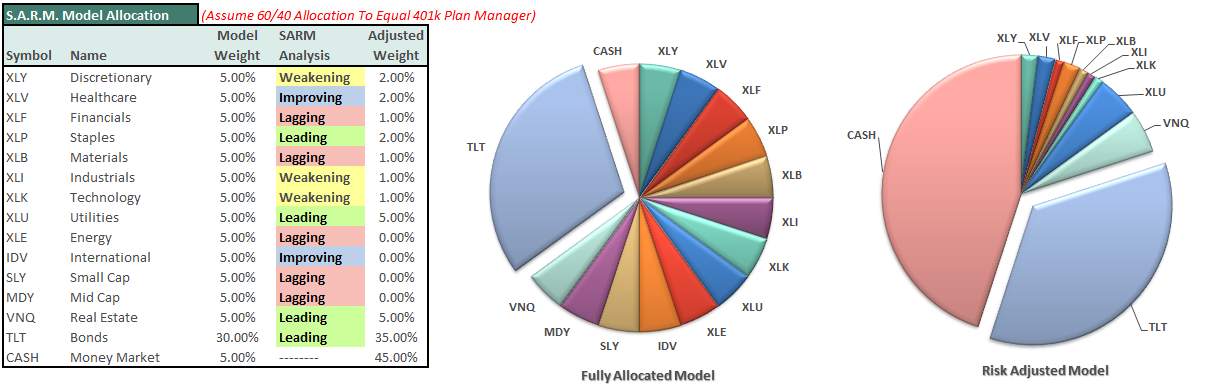

S.A.R.M. Current

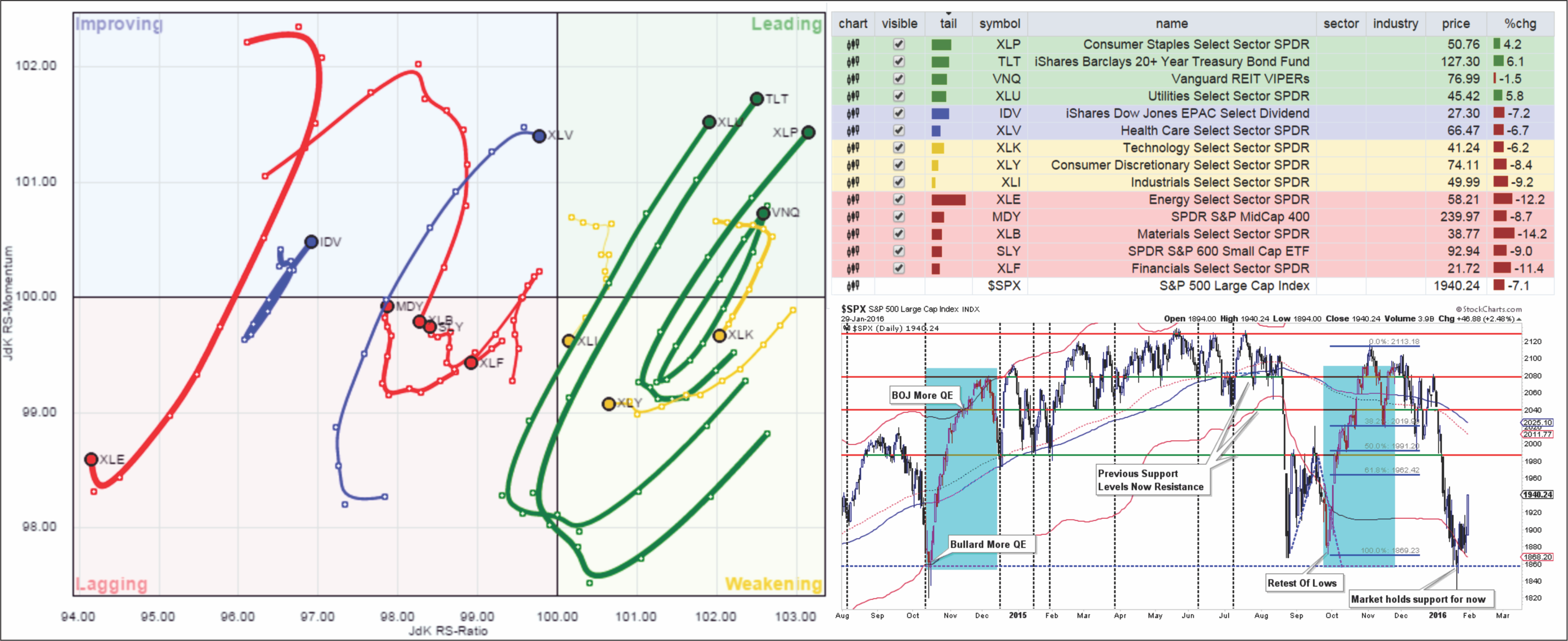

The Sector Allocation Rotation Model (SARM) is an example of a basic well-diversified portfolio. The purpose of the model is to look “beneath the hood” of a portfolio to see what parts of the engine are driving returns versus detracting from it. From this analysis, we can then determine where to overweight sectors which are leading performance, reduce in areas lagging, and eliminate those areas that are dragging.

The Sector Allocation Rotation Model continues to deteriorate suggesting that markets are significantly weaker than they appear. As suggested all through this missive, a reflexive bounce in the market should be SOLD into currently.

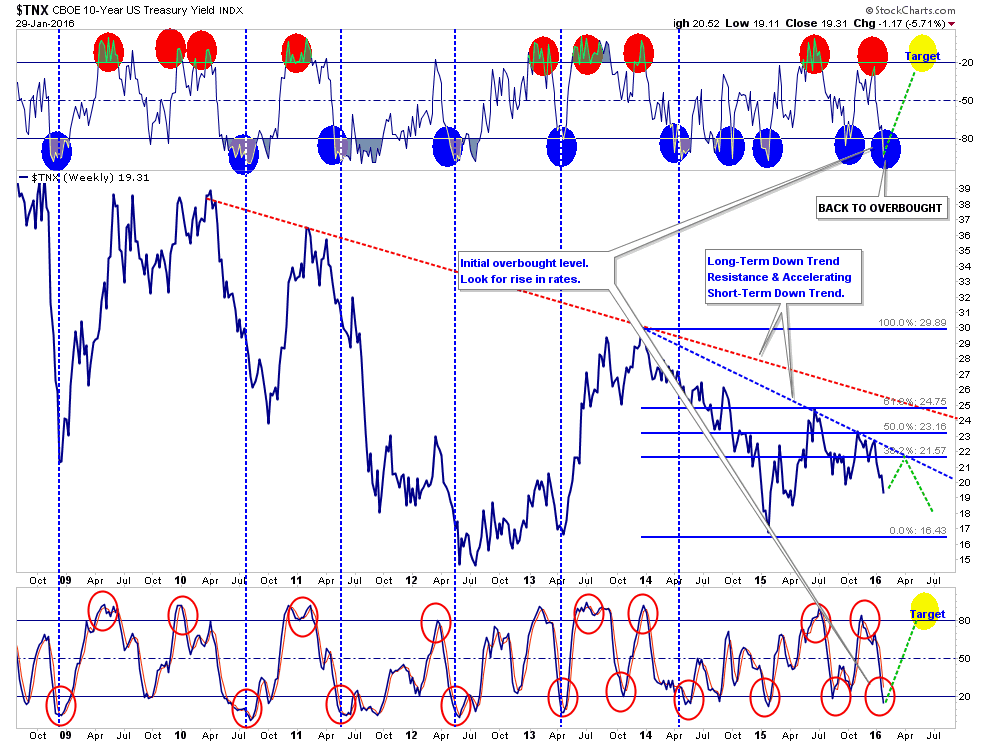

Not surprisingly interest rate sensitive sectors, along with the more defensive sector of the market, Staples, surged last week as the 10-year Treasury plunged below 2%…again. The search for safe haven investments such as REIT’s, Utilities, Bonds, and Staples has become a more crowded trade as capital leaves the previous leaders of Technology, Industrial and Discretionary sectors.

Energy remains a disaster along with Mid and Small-Cap indices. Financials have also weakened considerably along with Basic Materials as these economically sensitive sectors are continuing to be impacted by a slowing economy. Health care and International are only improving by not losing as much.

The call for fixed income to go below 2%, the target is 1.8%, this year is rapidly coming to fruition. Unfortunately, it is happening much more rapidly than expected as economic weakness continues to take hold.

With Interest Rates now very oversold, meaning bonds are overbought in price due to inverse relationship, it is time to take some profits and rebalance the fixed income portion of portfolios back to model weights (35% according to the model below.) We will look to add back to fixed income when rates push back up to the declining trend of 2.15% to a maximum of 2.4%.

The recommendations for “pruning and trimming” exposure over the past couple of months has already done much of the risk mitigation needed to navigate the current markets. Therefore, there should be only relatively minor changes needed currently.

S.A.R.M. Model Allocation

I have adjusted the model allocation to account for the rebalancing of bonds, REITS, and Utilities in portfolios. We will still want to use the current reflexive rally to take actions to rebalance portfolio models accordingly.

During THIS bounce in the market, adjust weightings as follows:

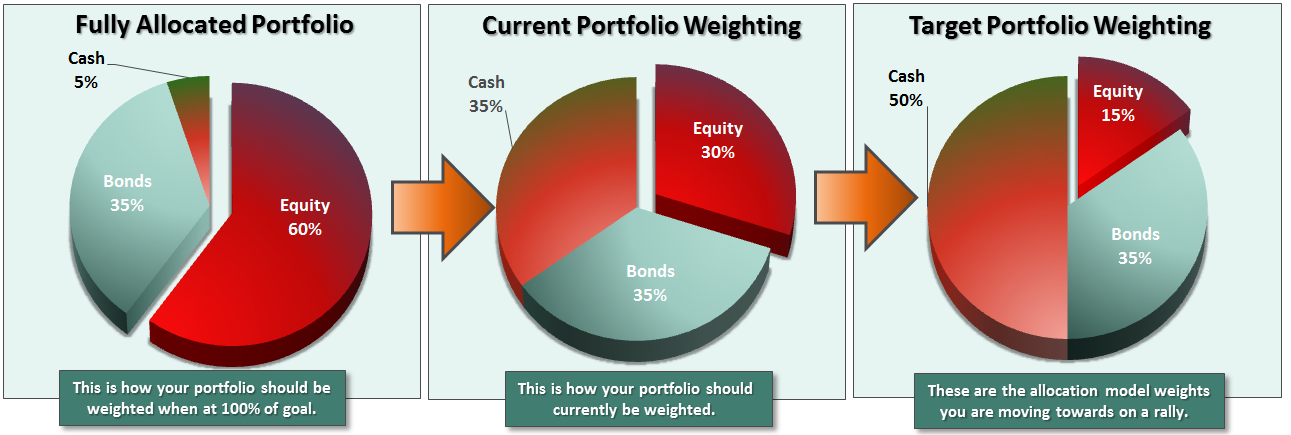

During this rally, cash will be increased from 43% of the portfolio to 45%, with 35% in bonds, and the rest in equities.

It is completely OKAY if your current allocation to cash is different based on your personal risk tolerance. This is just a guide.

As you can see, there are not DRASTIC movements being made. Just incremental changes to reducing overall portfolio volatility risks. However, if the expected bounce fails at resistance, then further reductions will be required in accordance with the risk reduction modeling.

Remember, as investors, our job is not to try and capture every single relative point gain of the market as it rises. While we certainly want to participate in the rise, our JOB is to protect our capital against substantial losses in the future. A methodology that regularly harvests gains, reduces risk and keeps the portfolio focused on longer-term goals will lead to a more successful outcome.

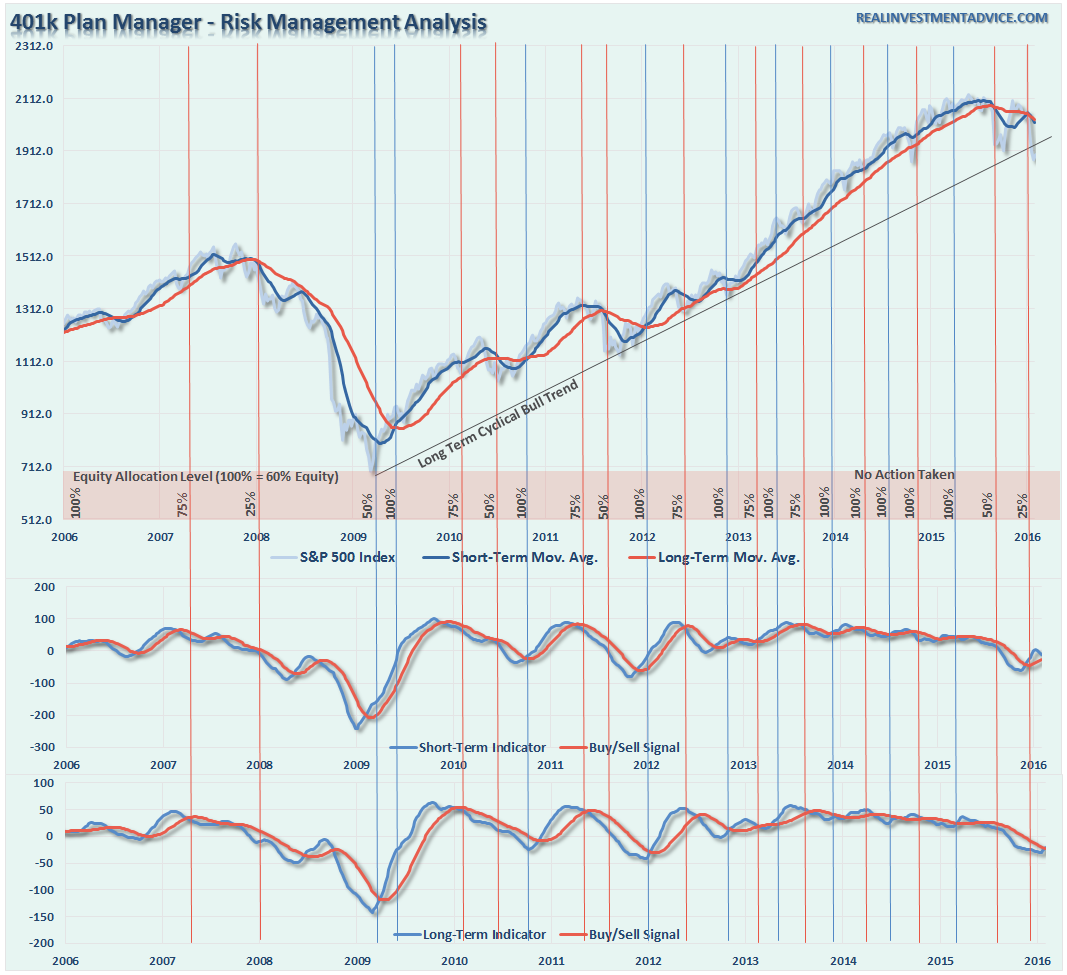

The Real 401K Plan Manager

I have added some new features to the 401k plan manager model following a recent discussion with my colleague Robert Seawright. This is to clear up the confusion between “risk management” and “market timing.” Market timing denotes being “all-in” or “all-out” of the market. I am only suggesting small modifications to the “risk” side of your portfolio by minimizing losses during periods of market declines.

As you will notice, I never advocate being 100% out of the market. As I have discussed many times in the past, it is far too difficult to reverse course when the market changes from a negative back to a positive trend. Emotions keep us from taking the correct action. There are 4-steps to allocation changes based on 25% reduction increments. As noted in the chart above a 100% allocation level is equal to 60% stocks.

Market Fails – Action Advised On This Bounce

As discussed above, the market has NOW BROKEN the long-term trend support. A change in TREND is critical and suggests that the bull market advance that began in 2009 is over. As shown in the chart above, the technical deterioration is significant.

I continue to advise caution. As I stated two weeks ago:

“The 401k Model is NOT being tactically adjusted at this time because the markets are VERY OVERSOLD on a short-term basis.”

As stated above, I expect the market to rally towards previous resistance at 1970 on the S&P 500. This level should be used to reduce portfolio equity risk to the current model levels.

The current market environment is NOT conducive to an overweight allocation to equity risk currently.

If the recent market volatility has made your nervous as of late, you are probably carrying too much risk in your portfolio. Use this bounce in the markets to take some action in your portfolio to reduce risk for now.

If you need help after reading the alert; don’t hesitate to contact me.

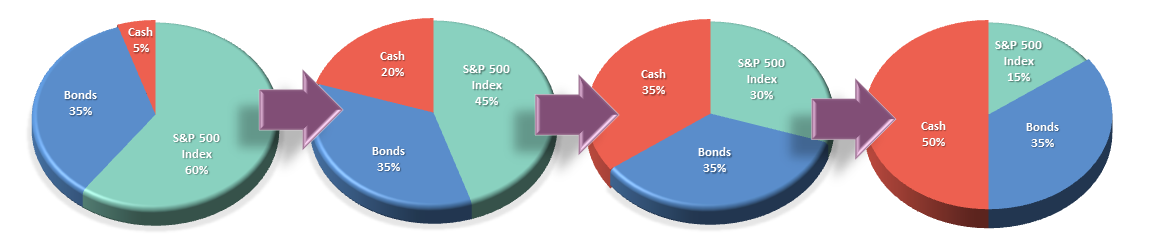

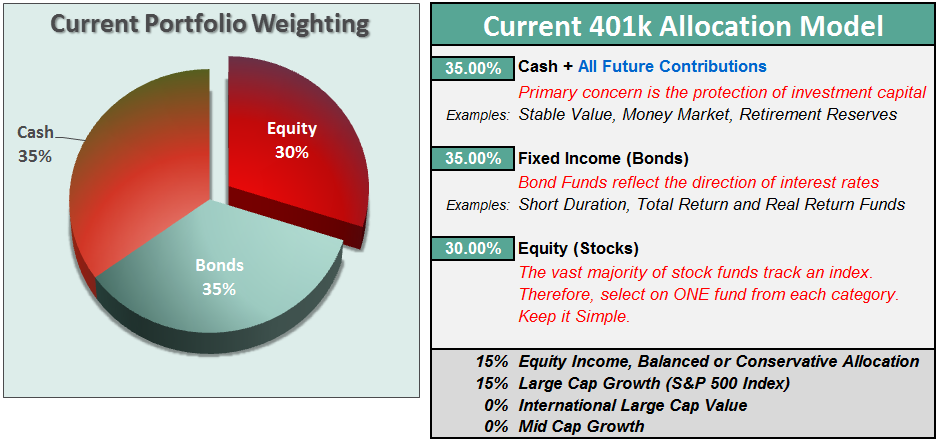

Current 401-k Allocation Model

I am adding the model allocation progression for clarity purposes. The chart below shows the transition from a fully allocated 401k plan, the current portfolio weighting, and the target allocation when, and “if”, the expected rally to 1970-ish occurs.

The 401k plan allocation plan below follows the K.I.S.S. principal. By keeping the allocation extremely simplified it allows for better control of the allocation and a closer tracking to the benchmark objective over time.

401k Choice Matching List

The list below shows sample 401k plan funds for each major category. In reality, the majority of funds all track their indices fairly closely. Therefore, if you don’t see your exact fund listed, look for a fund that is similar in nature.

Lance Roberts

Lance Roberts is a Chief Portfolio Strategist/Economist for Clarity Financial. He is also the host of “The Lance Roberts Show” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter and Linked-In