“

In this past weekend’s newsletter, I discussed the timing and process of reducing equity risk in portfolios to minimize the ongoing deterioration in the markets.

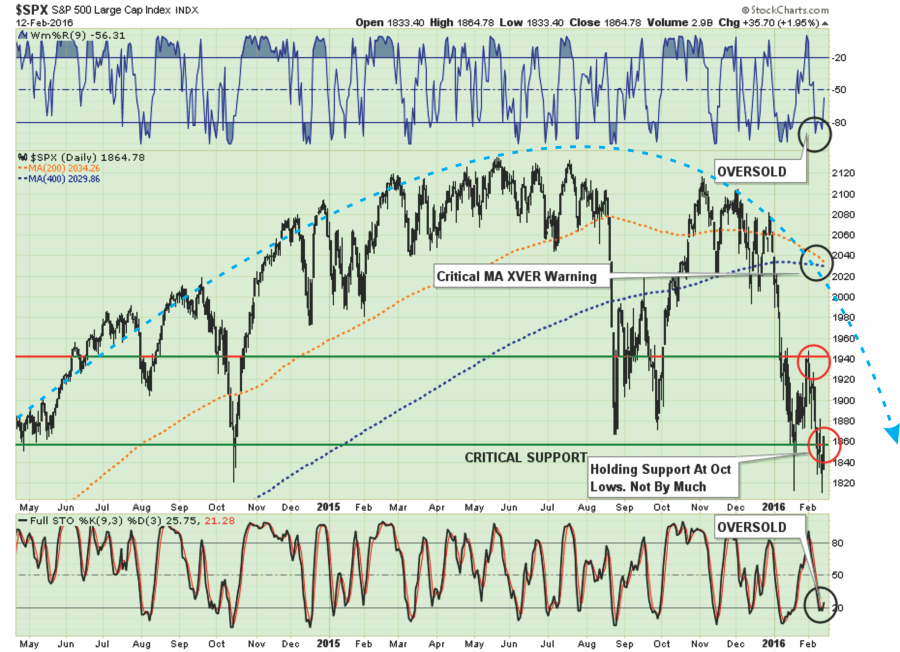

“On a very short-term basis the market is oversold and the bounce on Friday was JUST enough to close above the October lows support at 1860. Any continued rally next week should be used to further reduce equity risk and rebalance portfolios.”

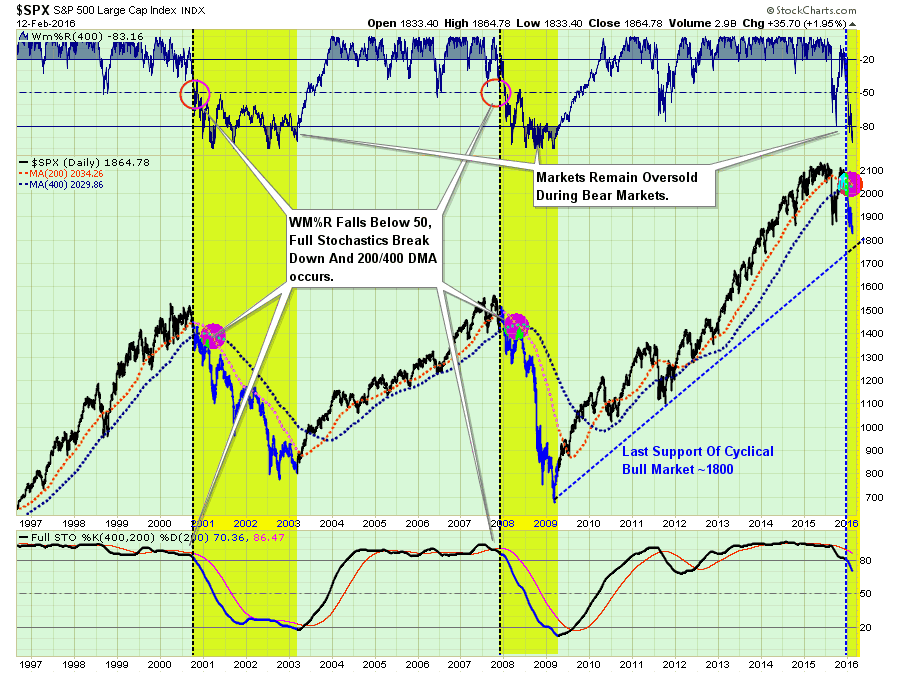

I have added the dashed blue line showing the formation of the asymmetrical bubble pattern that has been the hallmark of major market peaks in the past. While this pattern is not a definitive indicator of the entrance into a cyclical bear market, it does indicate that the easiest path for market prices is currently lower.

However, market bulls will argue, and correctly so, that the continued retests of the 1860 level by the markets is building bullish support for the market. However, this action is not uncommon at major market peaks as it takes time to erode bullish “hopes” to the point those supports finally give way.

With the markets once again oversold after last week’s fairly brutal sell-off, a rally is expected over the next couple of days to allow portfolio risk to be rebalanced. That rally could take the markets back to the previous resistance of 1940 (about a 4% push) from current levels. Such a rally would be enough to suck many of the “bulls” back into the markets pushing markets back into overbought territory and setting up the next decline.

Most likely the next retest of the 1860 lows will fail and, as we move into the summer months, the markets will begin to push to lower levels of support.

EXPECTATIONS VS REALITY

The analysis above, while considered “bearish,” is just an honest assessment of price trends currently. You can dismiss it, ignore it, and doubt it but that won’t change the potential negative impact to your personal wealth.

As Bob Farrell once quipped:

“Bull markets are more fun than bear markets”

That doesn’t mean that you should not acknowledge the risk of one. As I have discussed before, Wall Street has an incentive to keep you invested in the market at all times. There is nothing wrong with that as long as you understand the conflict of interest – their bottom line versus yours.

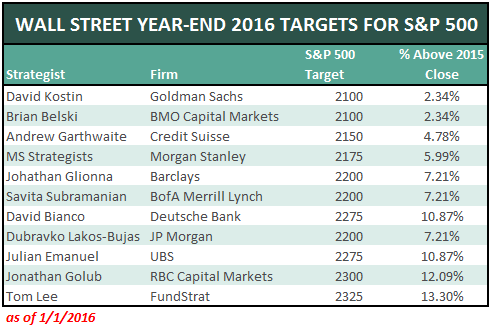

Let me show you what I mean. A recent survey of Wall Street firms 2016 year-end price targets revealed only slight reductions from where they were at the beginning of the year. At the beginning of this year in the 2016 Outlook & Forecast, I published a table of Wall Street targets:

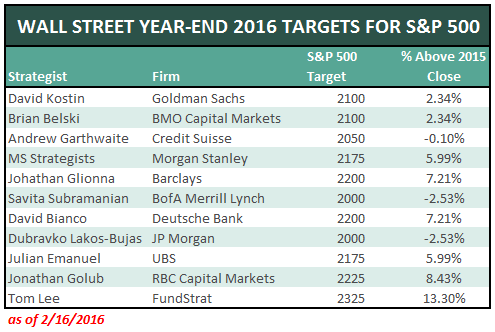

Here is the updated version just 45 days later.

None of them expected a market decline just 45 days ago, and even after the recent rout, only two expect a moderately negative return by year-end. If you are betting your retirement on people making predictions 12-months out, you are likely going to be very disappointed. (Furthermore, with the markets already down -8.5% for the year, you are now almost 3-years behind on your financial plan if you are using those 8% annualized rates of return Wall Street keeps touting.)

The problem with the “always bullish mantra” is the lulling of individuals into a false sense of security which leads to a host of investor mistakes.

Just recently, Ben Carlson, via A Wealth Of Common Sense, wrote a really good piece on why “bear markets” are so painful. Simply put, and as shown below, “bull markets” generally advance over longer periods causing individuals to forget about the very short-term, vicious “mauling” of the previous “bear.”

While the entire article is worth reading, I do disagree with one point Ben makes. In his missive he states:

“…the majority of investor mistakes occur during bear markets.”

In actuality, the majority of mistakes that investors make are during bull markets as they:

- Chase performance

- Chase yield

- Overpay for investments

- Ignore accrued build up of portfolio risk

- Opt out of fixed income to chase performance

- Skew diversification by incorrectly rebalancing

- Misalign portfolio duration to financial goals.

I could go on, the list is long. During rising bull markets investors are continually forgiven for a whole bevy of investment mistakes. It is only during bear markets that these mistakes are realized and the true meaning of “risk” is revealed.

Ben is correct that investors make the mistake of making “emotionally driven” decisions during sharply declining markets. However, if investors had been counseled about portfolio and risk management during the first half of the “full market” cycle, they would not be making “panic” based decisions during the second half.

SPEAKING OF COMPLACENT

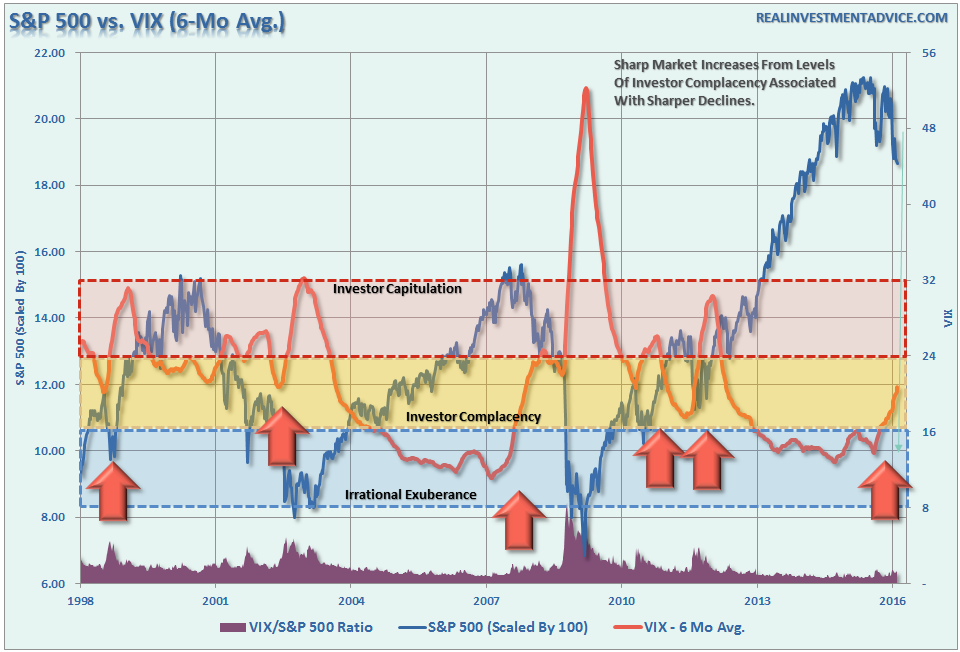

While the market has been under substantial attack since the beginning of the year, one of the reasons I remain more “risk averse” currently is simply due to the fact that investor complacency is still very high. The chart below is the volatility index (VIX) smoothed with a 6-month average to reduce the noise of short-term market dynamics.

As you will notice, volatility has indeed risen over the last couple of months which would be expected during a market decline.

However, and most importantly, the rise in the 6-month smoothed index is more consistent with the onset of more severe market corrections. Furthermore, despite the recent turmoil, volatility remains at levels more normally associated with investors complacency rather than capitulatory levels normally associated with the end of a bear cycle.

CENTRAL BANKERS UNITE

Of course, the one thing that could quickly change the entirety of this analysis would be a reversal of policy by the Federal Reserve in March.

If Yellen & Co. would decide to join the rest of the major Central Bank’s push into negative interest rate territory, and/or launch an additional round of Quantitative Easing (QE), the markets would reverse sharply.

In such an event, recommendations would change to begin increase equity exposure accordingly. That is…what it is.

In the meantime, there is no indication of such a policy shift near term, as Ms. Yellen seems determined to promote the underlying economic recovery story. Although, if the market decline begins to significantly erode consumer confidence, action by the Fed would not be surprising.

However, until then, I continue to suggest taking actions to reduce risk in portfolios by using the current rally to:

- Trim back winning positions to original portfolio weights: Investment Rule: Let Winners Run

- Sell positions that simply are not working (if the position was not working in a rising market, it likely won’t in a declining market.) Investment Rule: Cut Losers Short

- Hold the cash raised from these activities until the next buying opportunity occurs. Investment Rule: Buy Low

As you will note these are not drastic changes. Simply rules of portfolio management that have survived the test of time and are the basis of every great investor’s philosophy throughout history.

As Gerald Loeb once stated:

“The art of investing is being able to adjust to change.”

Lance Roberts

Lance Roberts is a Chief Portfolio Strategist/Economist for Clarity Financial. He is also the host of “The Lance Roberts Show” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, and Linked-In