Next to Japan’s “unexpected” re-acquaintance with recession, the most serious indication of global economic distress has to be oil prices. And where commentary turned to “explaining” Japanese recession as related to a small attempt at fiscal discipline rather than the more debilitating flirtation with intentional debasement, convention surrounding the precipitous plunge in crude is desperately trying to direct toward “supply.” In both cases, the spinning narratives hold enough water to offer some plausibility; as clearly the tax increase in Japan was unhelpful to an economy already suffering from QQE-yen projection, at the same time there has undoubtedly been a significant increase in domestic crude production.

Neither of those are sufficient, however, to form a compelling and comprehensive view of the global economy. The mainstream commentary is limited by its colored view of “the recovery” and so, in terms of oil, it has to be supply. But empirical history more than suggests that demand is the primary focus of oil prices – outside of blatant “dollar” engineering.

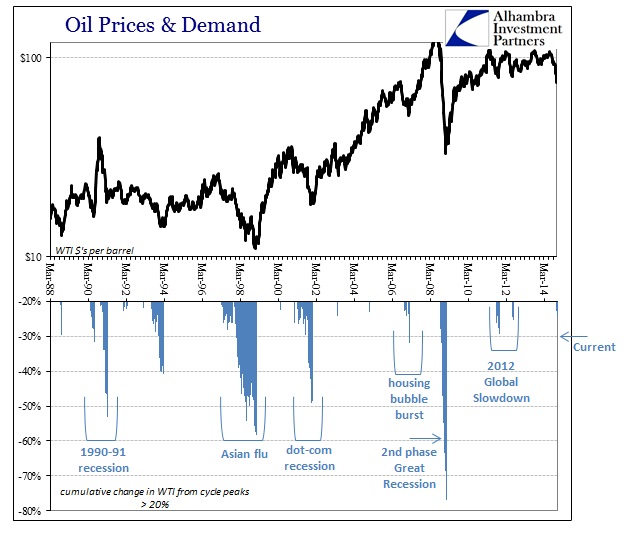

Going back to the 1980’s, in almost every instance where there has been a 20% decline in the price of the WTI benchmark (light, sweet in Cushing, OK) it has coincided with either outright recession in the United States or a global slowdown (that precedes outright recession in the United States). The only exception here was the drop in oil prices in 1993 that could probably be classified in conjunction with the steady decline after the 1991 recession.

Prior to every US recession, global oil prices have made a habit of taking on one of these major downward moves in what looks to be more elongated business cycles. There has been a clear change in economic and cycle pattern found easily in the proliferation of “jobless” recoveries after the 1980’s, but there is also a related and seemingly misunderstood extension of that to the cycle peaks as well. Where economic convention fails to connect the Asian flu with the dot-com recession, for example, there are also enormous similarities between what happened then and what occurred between 2006 and 2008, and the period 2011 to now.

As it was, the US barely escaped recession in 1998, instead “following” the course set by Greenspanism and into dual bubbles (both the housing and stock bubbles are obvious in their 1995 inflections). That meant where “global growth” had downshifted, including the baseline advance in the US, the central bank here (as well as others abroad, like the BoJ introducing the world’s first ZIRP regime in 1999) tried in vain to arrest that deterioration. They “succeeded” only in the context of stalling the inevitable for two years before recession came anyway. Unfortunately, the interim period contained those asset bubbles which only grew far worse, meaning a larger ultimate “reversion to the mean.”

In some respects, that same exact process had been played out in the late 1980’s, where “global growth” had downshifted from the early 1980’s true recovery. By 1986, the US also had escaped recession and then saw one of the largest monetary bursts that eventually shook out as the junk bond bubble and the S&L crisis. And while global growth slowed during that period, central banks around the world did what they always do to try to prevent the tide of the inevitable business cycle (especially, again, BoJ and the epic Japanese bubble of the late 1980’s that related to the “great” currency intrusions of the Plaza Accord, and then the Louvre Accord to try to undo some of the Plaza Accord).

What was established by the late 1990’s, then, was a pattern of how the elongated cycle would work – there would be a noticeable slowing in growth that would take global form and reach, to which central banks sprang into action to quell such economic disquiet. The mechanism for that monetary reproach was uniform financial imbalances that acted not as a recession prophylactic but rather as an amplifier to the downside. In simple terms: growth slowdown followed by heavy central bank “stimulus” that “somehow” coincides with great financial imbalance that only delays the inevitable for a few years.

To orthodox economists, this was success in that the artificial “burst” of activity, largely bubble based, looked like recession prevention. Thus the cycle peak was actually moved ahead by several years to which the orthodoxy counts as a separate cycle entirely – which then moves the bubbles themselves, wrongly, into a separate category in convention.

The visible signal is crude. In these elongated cycles, including a minor oil disruption in 1988, a crude oil warning of sorts precedes the each new business “cycle.” The Asian flu, then, and the tumble in oil prices into 1999 was not a distinct cyclical phase but rather the first inflection toward trouble. The response in every nation affected was, again, monetary and thus coincided with preventing recession in only the immediate circumstance – thus allowing bubbles to advance much further. What happened after 1998 was an immense rush of financialism globally, including emerging markets that built up not “reserves” but upon the rapid acceleration of the eurodollar standard into every economic edifice.

While the recession in 2001 was mild in the US, it was not elsewhere (and the US, pace Krugman, was only “saved” by the inflection of the housing bubble to outright mania). But there should be no mistake that the dot-com recession had its origins in 1997 and the global slowdown that followed and never arrested (unfortunately timed to make far too many look upon Greenspan as some sort of monetary “maestro”).

The next cycle played out in almost exact replication, as by the time of the housing bubble finally bursting in 2006 there was the now-familiar oil “warning.” “Global growth” slowed into 2007, including the US as I have noted time and time again, but did not fall immediately into outright recession. Instead, financial imbalances only grew (at least until early 2007, and really all the way to August 2007) despite the clear warning in crude prices back in 2006 that the baseline growth assumption was “off.” After that initial move, crude prices followed sharply the orthodox idea that everything was “contained” and that “decoupling” would assure only minor disruption – right up until the moment when that slowing trend that began in 2006 was revealed in the summer of 2008 as far more damaging and widespread than thought by conventional opinion.

Crude prices now are following much the same trajectory as the 2006-09 period, with a warning about “global growth”, including as always the US, beginning in 2011 and following into 2012. That preceded the massive slowdown in the global economy in 2012 to which every central bank around the world responded via monetary means (no coincidence as to what Bernanke was thinking about QE3 in the summer of 2012). That created an artificial “burst”, more likely only a pause in the decline rather than anything of a “surge”, to which crude prices responded as they had in the prior elongated cycles – to ultimately pointless monetary posturing rather than actual signals from the economy itself.

At this point in 2014, the other side of that elongated “peak” process appears to be forming, as WTI has now fallen more than 30% from its recent peak in June. That would be not only the largest such decline since 2009, but also, by far, the quickest.

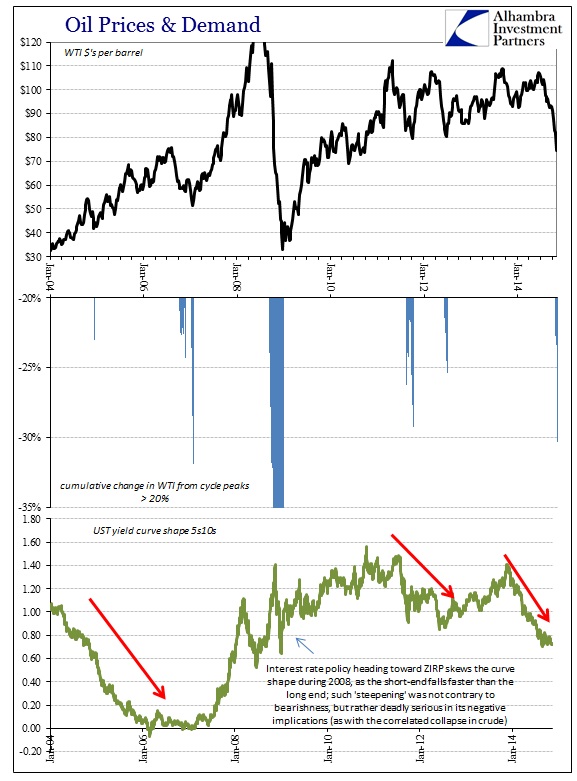

Credit markets, at least the wholesale and UST pieces, are mostly in agreement with oil prices in the past decade (with the exception of the panic in 2008, where the curve shape underwent drastic alterations from the inside out as the Fed administered interest rate targeting “stimulus”). In fact, it seems very much like credit markets lead oil prices by several months (especially in the current “recovery” period). The same factors and perceptions that skew the yield curve toward bear flattening also act upon oil prices, and they are not the amount of crude flowing out of domestic fracking plays.

This correlation can be extended to other commodity prices as well, which again precludes the predominance of “supply” as the driving force in prices. Credit markets and oil prices are in tandem warning about the next phase of “global growth” as it exists within the modern occurrence of the elongated business cycle. If the history of that since 1985 is indicative of what to expect, the elongated peak may be finally coming to an end. That would fit with intuitive perceptions where central bank actions after the 2012 slowdown are coming up far short of intents, and thus that deficient baseline is once again being revealed as well beyond monetary “aid.”