To the never-ending astonishment of our economists, global growth has been much weaker since the Financial Crisis than before it, despite enormous global stimulus from years of extreme central-bank monetary policies and record amounts of government deficit spending.

This should not have happened, according to our economists. Fiscal stimulus and expansionary monetary policies beget economic growth, which beget even more economic growth. That’s the theory. And that’s precisely what hasn’t happened. All it did was inflate asset prices. But the global economy has been a dud.

“If we calculated global growth with China’s true growth rate and not the official rate, global growth in the second quarter of 2015 would be only 2%,” figured Natixis, the investment bank of France’s second largest megabank, Groupe BPCE.

This “sluggish growth, close to a recession, is due to persistent, structural causes; we therefore use the term ‘structural recession’ to show that it does not have a cyclical origin,” the report explained. It’s not caused by normal cyclical fluctuations, but by “persistent structural problems that are specific to each region.”

China loses its cost-competitiveness

The problem dogging China is the soaring cost of labor, in an economy that is still too centered on low-end products and exposed to “a very high level of the price elasticity of exports.” Thus, if Bangladesh or Vietnam can produce it a little more cheaply, China loses those exports.

Labor costs have soared in the double digits year after year. Even per-unit labor cost, which compensates for productivity gains, has jumped year over year: in 2015, by 4.5%, which is at the low end; and by over 10% at the high end in 2000-2001 and 2007-2008.

Hence a decline in exports of those products, a weakening of investments, and a sharp weakening of what Natixis calls China’s “true growth.”

Japan Inc. shortchanges its workers.

The main problem in Japan is “the excessive and virtually continuous distortion of income distribution at the expense of employees.” This shows up in the “frequent decline in real wages.”

OK, that sounds like an American disease as well, and it is….

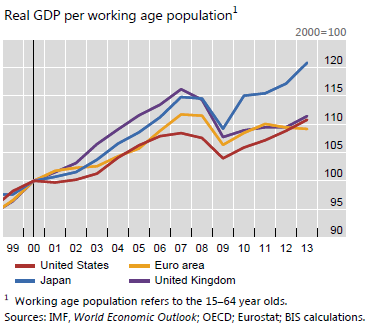

Real per-capita wage growth in Japan has been negative year over year since 2013. From 1998 to 2012, there had been five significant periods with real wage declines. Yet per-capita productivity has continued to grow. And real GDP per working-age population has outgrown the rates in the US, the Eurozone, and the UK, as this chart from the Bank of International Settlements shows (blue line = Japan):

The Japanese are working hard and productively but are increasingly reduced to cheap labor by Japan Inc. The consequences of Abenomics, including a bout of inflation, have made this condition worse. If workers don’t make enough money, household demand is left twisting in the wind.

Household demand moved in fits and starts. But on April 1, 2014, the consumption tax hike hit, and household demand plunged. It’s now merely 9% above where it had been 1998.