Editor Note: Michael Lebowitz of 720 Global Research is an investment consultant, specializing in macroeconomic research, valuations, asset allocation, and risk management. He is a regular contributor to Real Investment Advice.

The following research was jointly produced by: J. Brett Freeze, CFA of Global Technical Analysis and 720 Global

720 Global has written four articles to date on stock buybacks and the harm these actions will likely have on future corporate growth rates and the economy. To better gauge the effect of buybacks we join forces with Brett Freeze to present a unique analysis on the S&P 100.

As we have previously noted, a large majority of companies, including 94 of the S&P 100, have actively repurchased shares since 2011. These companies often announce and execute share repurchases without providing a rationale to shareholders. As a fiduciary of shareholder’s capital, managements’ core responsibility is to act in the best interest of its shareholders. Unfortunately, we believe the majority of current repurchase activity is dictated by management’s self-serving desire – temporarily inflating the current market-value of company stock, while enriching themselves through the exercise and sale of equity-based incentive compensation.

There are two conditions that should be met when a company engages in a stock buyback. 1) The shares should be trading below intrinsic value 2) there are no investment opportunities available that would allow the company to continue to grow at a desirable rate. If both conditions can be met a case may be made for share buybacks.

This article solely focuses on the first aforementioned condition– intrinsic value. For more information on the second condition, please read “In Yahoo, Another Example of the Buyback Mirage” by Gretchen Morgenson of the New York Times. In her recent article, which quoted 720 Global, she demonstrates how Yahoo weakened future earnings growth rates and corporate value through questionable stock buybacks.

Intrinsic value is not the market price or market capitalization of a company or its stock, but a theoretical value formulated through analysis of the balance sheet and income statement of the company. Conceptually, investors should seek companies whose share prices trade below intrinsic value and shun those trading above intrinsic value. This logic equally applies to corporate management executing buybacks.

When shares are purchased below intrinsic value, the company has added value. It is equivalent to buying a dollar bill for fifty cents. Conversely, share repurchases executed at a premium to intrinsic value destroy intrinsic value. Existing shareholders who sell are rewarded by the share-repurchase program, but those who hold are irreparably damaged. In the words of Warren Buffett from his assault on buybacks:

“Buying dollar bills for $1.10 is not good business for those who stick around.”

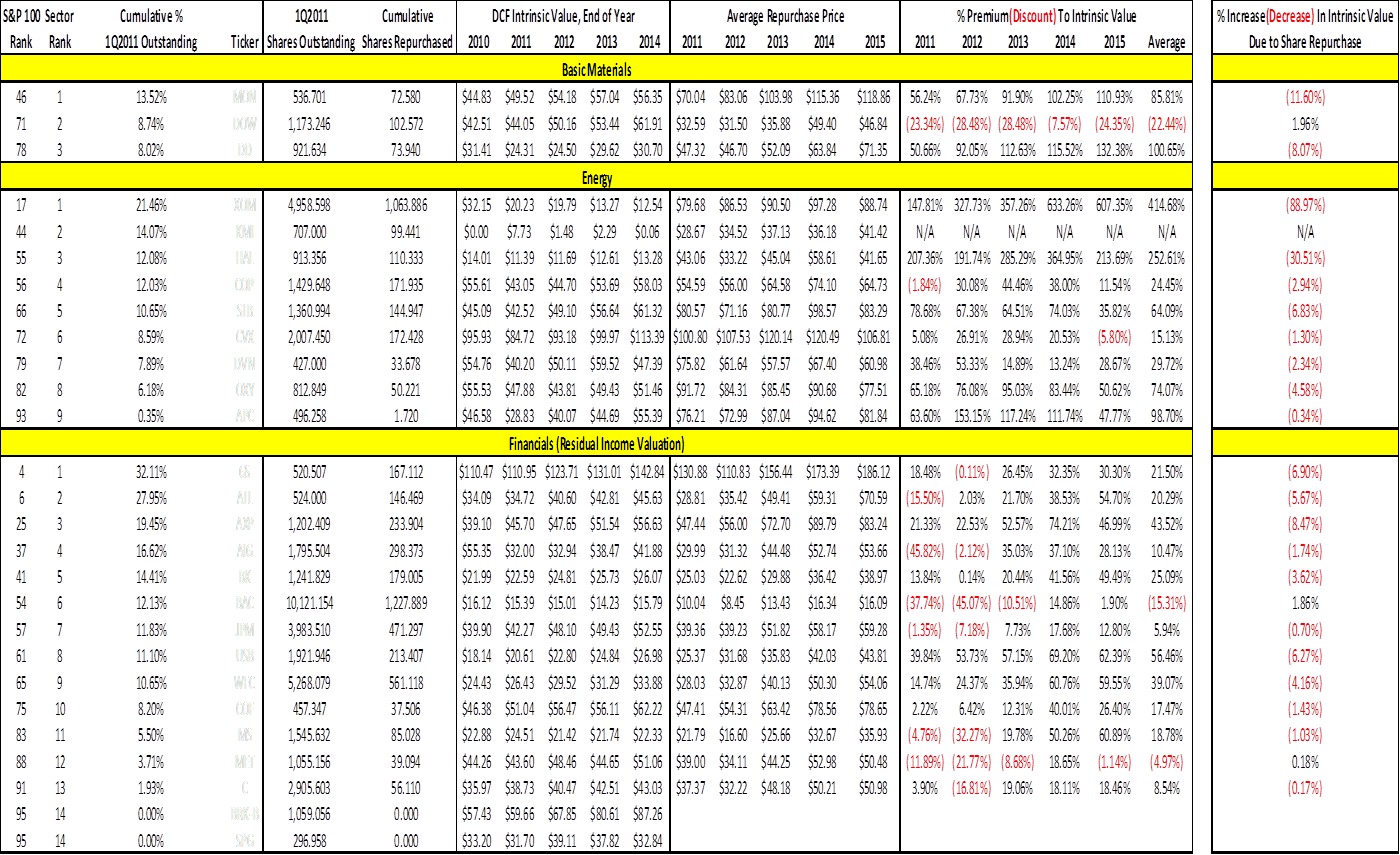

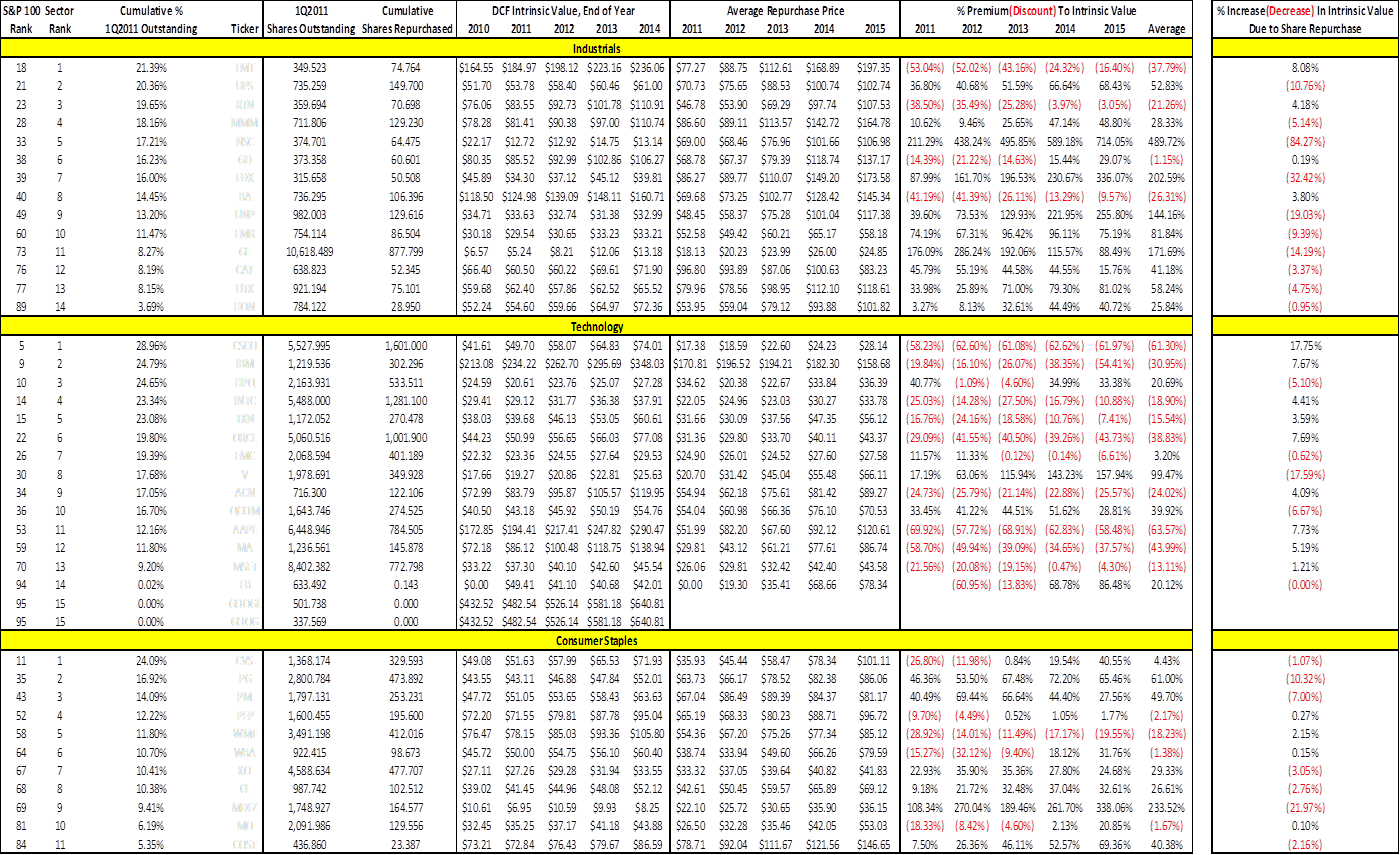

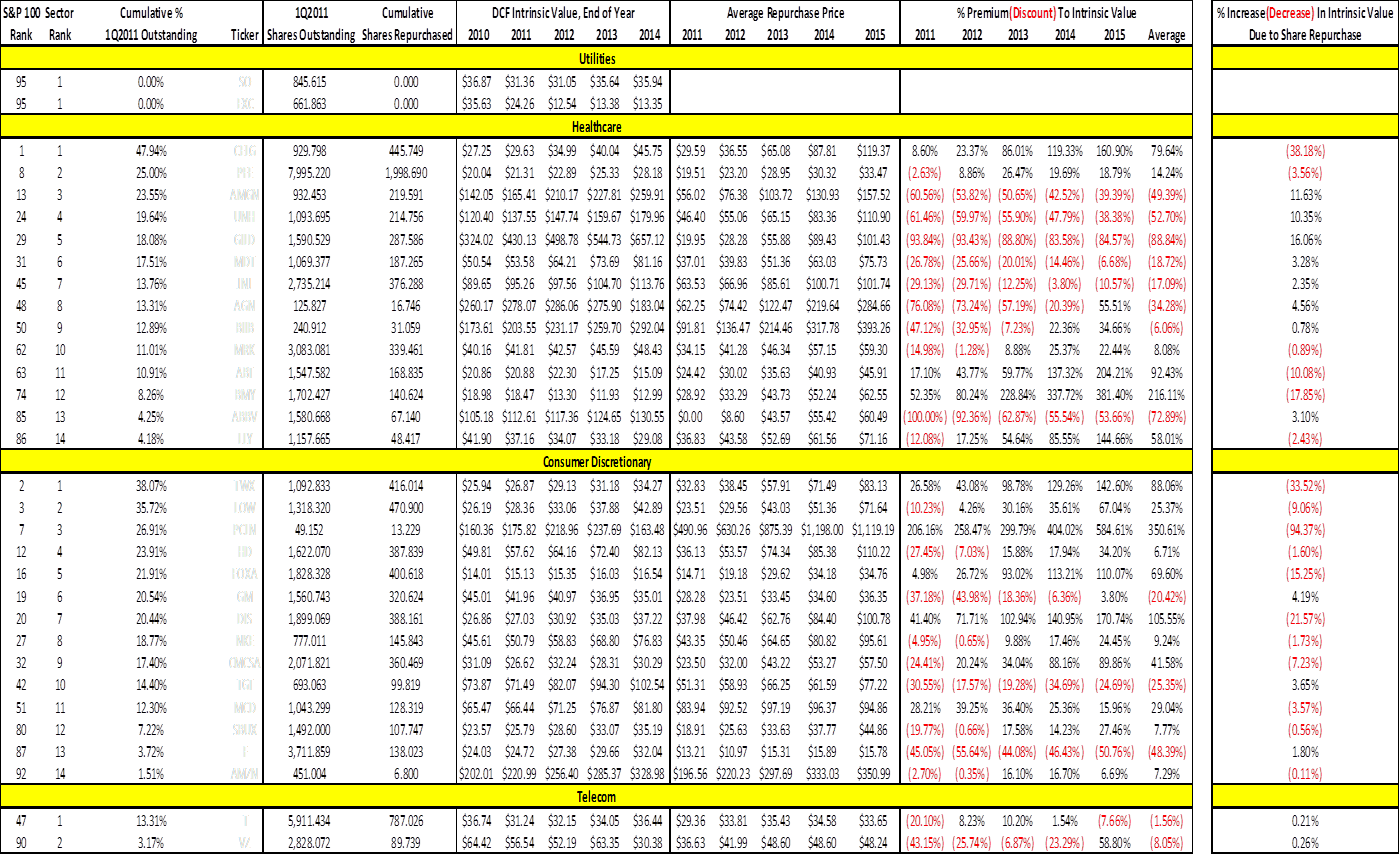

For this analysis we evaluate share repurchase activity and intrinsic values for the companies in the S&P 100 Index. Our measure of intrinsic value for non-financial companies was calculated using Global Technical Analysis’s proprietary discounted cash-flow model. For each non-financial company, 20-years of estimated forward cash flows were discounted by the weighted-average cost of capital (energy company data was normalized, when necessary). For financial companies, our measure of intrinsic value was calculated using Global Technical Analysis’s proprietary residual income model.

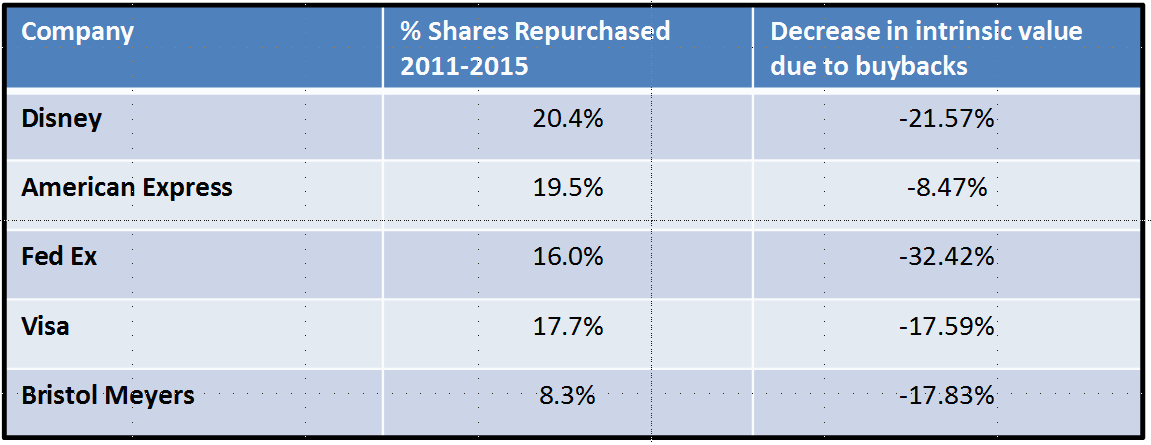

The following table provides a glimpse of the value being reduced by share buybacks of five widely-held companies.

The entire analysis is presented below by S&P Sector. Within each sector, companies are ranked by cumulative share repurchases relative to Q1 2011 outstanding shares. The final column of data shows the effect of share repurchase activity on intrinsic value. This column reveals the positive or negative effect that buybacks have had on the intrinsic value of each respective company.

S&P 100: Share Repurchase Analysis

The results of our analysis confirm our beliefs regarding share repurchases. Approximately two-thirds of the S&P 100 destroyed intrinsic value, by an average amount of 12.03%, as a result of their share-repurchase programs.

***Corporate names have been withheld from this presentation. A full analysis can be acquired by contacting the authors.

Michael Lebowitz, 720 Global Research

RIA Contributing Partner

Follow Michael on Twitter or go to 720global.com for more research and analysis.