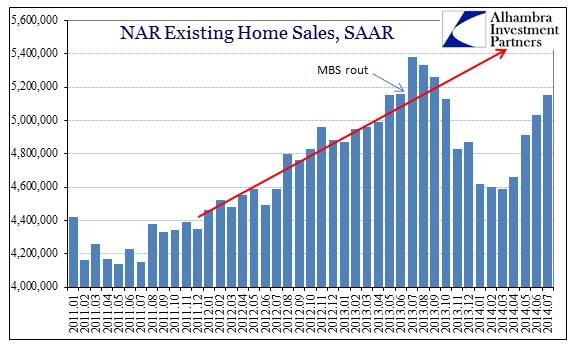

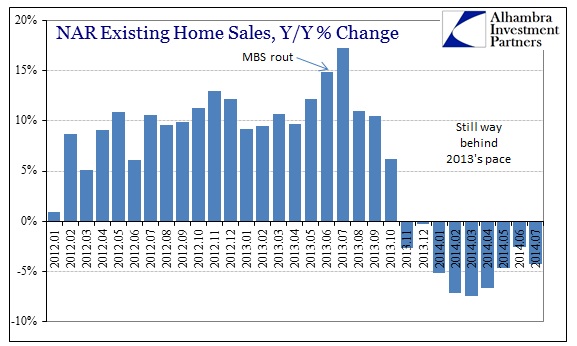

Existing home sales rose again in July from a downward revised June, as the monthly change of 2.4% matched June’s revised increase over May. The yearly comparisons still continue to lag, as does the overall trend after the massive interruption that began last autumn.

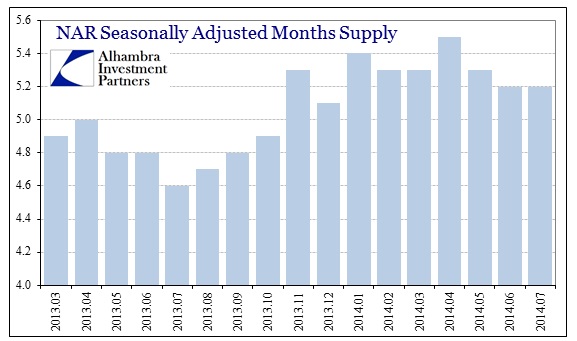

As the pace of sales has come back somewhat in 2014, the number of properties for sale has largely matched. That means that there are now more homes for sale than at any point in the past five years (going back to the tax credit fiasco in 2010). With the actual sale activity gyrating recently, that has meant the inventory-sales ratio has remained elevated.

What is perhaps most interesting out of all of this is that the upper segments continue to see rapid sales while the lowest end, the “distressed” category, maintains its implosion. That is taken as a positive by most, including the NAR itself, as it presumes a healing process.

I don’t think they are quite reading that right, as the collapse in sales at the lowest end is due for the most part to the demand side as institutional buyers have almost fully refrained from expanding their REO-to-rent operations (all-cash sales were the lowest since January 2013). That they would do so speaks not just to the economics of housing at the low end, but the economics of their prospective renters and the forecasted ability to turn cheap houses (with some maintenance work and upgrades, both physical and financial) into premium rental properties.

With that in mind, it is also interesting that the “middle market” segments continue to struggle, particularly the lower piece there. Taken together, the bifurcated economy rears its ugly head once more. The problem, as shown here, is that almost three-quarters of all homes sold take place in these two price tiers.

Even NAR’s chief economist, Larry Yun, has picked up this theme.

Although interest rates have fallen in recent months, median family incomes are still lagging behind price gains, and mortgage rates will inevitably rise with the upcoming changes in monetary policy.

I’m not at all convinced about the last part, but in any case even Yun is apparently warning about the trend in housing going forward, at least until he takes the same data point and flips it around to somehow look positive.

Fast-forward to today and rising home values are helping owners recover equity and strong job creation are assisting those who may have fallen behind on their mortgage due to unemployment or underemployment.

Affordability may be a serious issue because of rising prices and stagnant incomes, but that is offset by rising prices and “strong” job creation?

First-time home buyers continue to be conspicuously absent at only 29% in July, remaining “historically low.” That would seem to confirm the data in household formation as it ties together not just macro factors like wages but also the demand for rentable space and home purchases. The real problem with rising prices is that the median price is telling us almost nothing about affordability as it gets tugged upward by the sales skew (far less on the extreme lower end, and more at the extreme upper end).

More than anything, home sales still bear the heavy imprint of asset inflation and redistribution. Instead of just pushing people into housing generically via the assumed low interest rate channel, it would be far better for the “market” to find its own pricing levels to clear imbalances at all ends, rather than further them by intrusions above and below. Until that happens these kinds of incongruent setbacks look to be more normal than outliers.

Click here to sign up for our free weekly e-newsletter.

“Wealth preservation and accumulation through thoughtful investing.”

For information on Alhambra Investment Partners’ money management services and global portfolio approach to capital preservation, contact us at: jhudak@alhambrapartners.com