Concurrent to more survey-based indications of a US manufacturing slowdown, economists have been quick to blame overseas problems such that it leaves a “strong” US economy as a baseline. On the other side of that equation, China’s manufacturing likewise is rapidly declining but somehow with the same point of blame. Both Chinese PMI’s were decidedly weak, with the private version far more so than the government’s number.

The government’s official gauge of factory activity improved with the manufacturing PMI rising to 49.8, up from August’s three-year low of 49.7 but still marking two straight months of decline. Meanwhile, a private survey by Caixin/Markit revealed PMI fell to a fresh six-and-a-half year low of 47.2, ticking down from August’s reading of 47.3 but still better than an earlier flash estimate of 47.

A big part of this renewed descent is apparently Chinese exports:

Total new work fell at the quickest rate in over three years, partly driven by a steeper fall in new export business, Markit said in a report. As a result, companies cut output at the sharpest rate in six-and-a-half years, while staff numbers fell at the quickest pace since the start of 2009.

US manufacturing declines on “overseas” weakness while Chinese manufacturing declines on “overseas” weakness as if the two economic systems never deal with each other, only the same, non-specific “global economy” that doesn’t somehow count either of them within its growing malaise? It seems far more likely, beyond a doubt, actually, that with the amount of trade between them (especially from China to the US) if Chinese manufacturing is declining than US “demand” is a problem.

Any chronology of China’s post-Great Recession descent follows exactly that relationship. US economists are quick to assert a break, where the US economy has surged since the unemployment rate is so low but China’s economy, which certainly feels instead the effects of the denominator in the unemployment rate as much if not more so now than the statistical outlet of the numerator, begs to differ.

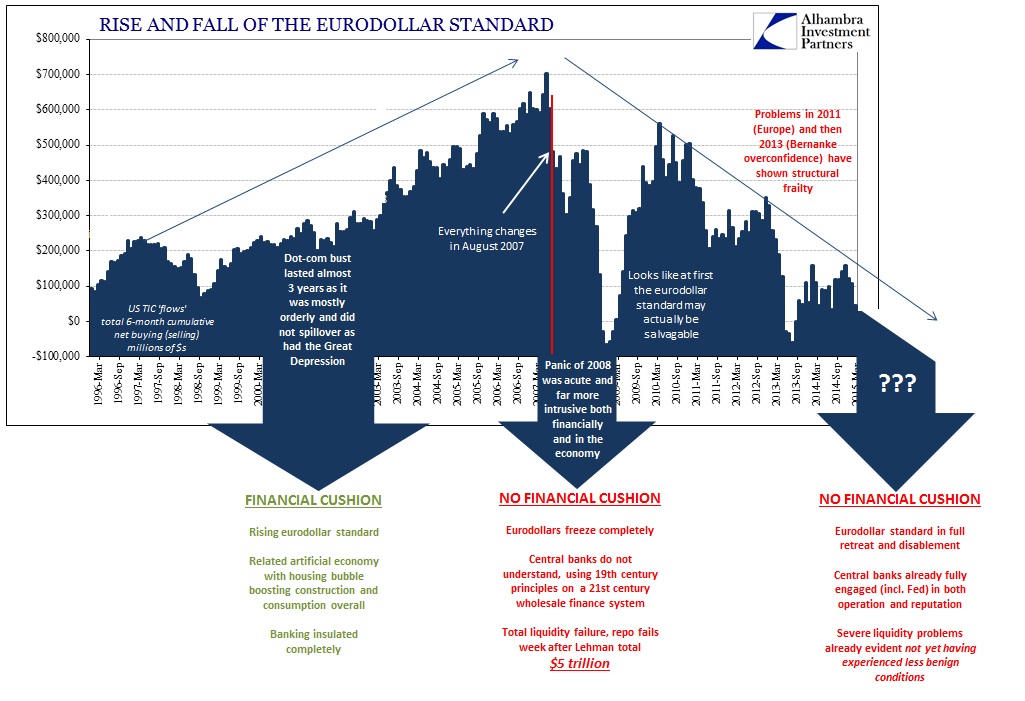

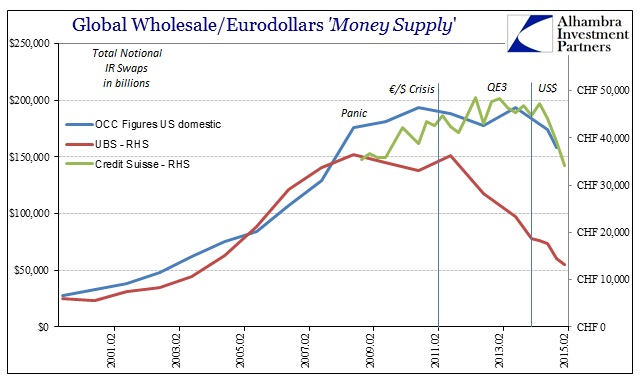

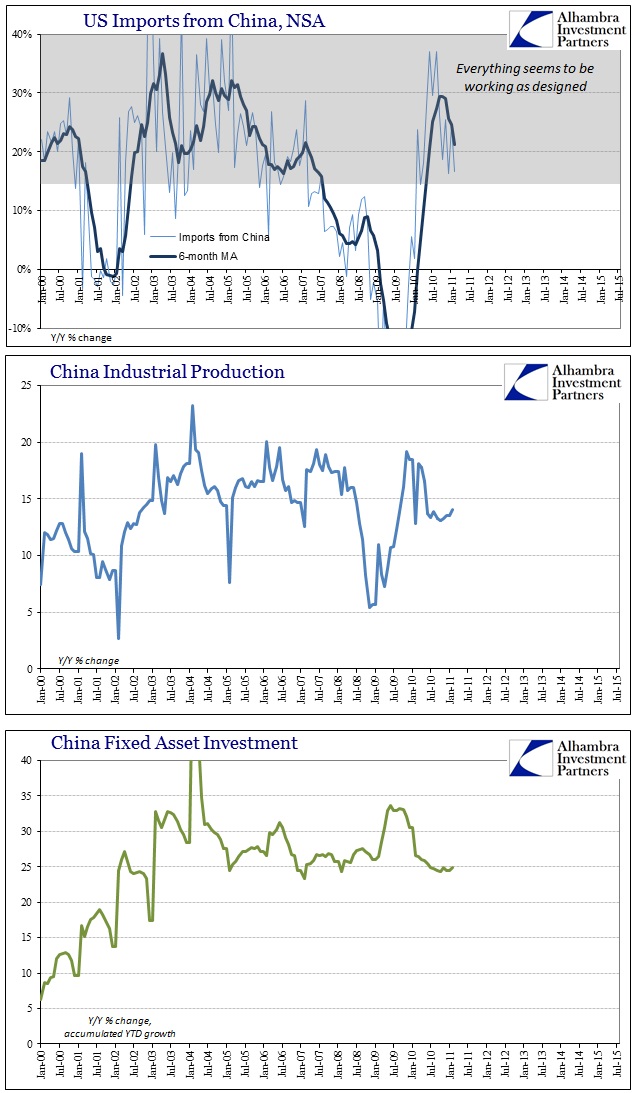

Starting at the trough of the Great Recession, all economic expectations here and abroad were based upon Milton Friedman’s plucking model – the beautiful symmetry of the V-shaped recovery. There were no suggestions of long-term difficulties or structural problems in the orthodox view of even the panic, so every central bank around the world engaged “stimulus” (combined with various fiscal attempts) to bridge the gap between the deep recession and the expected handoff to an organic, symmetrical recovery. In China, those efforts were greater than most, both monetary and fiscal, as the entire marginal economy had come to service the export-driven emphasis.

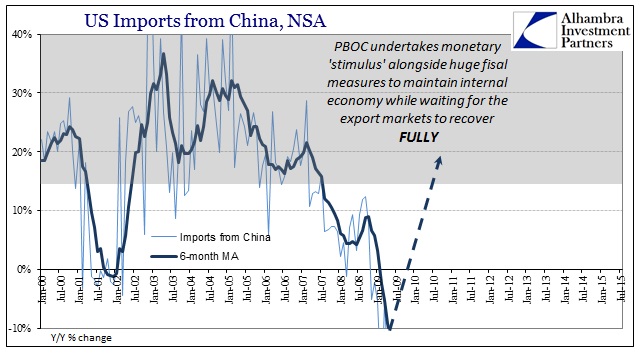

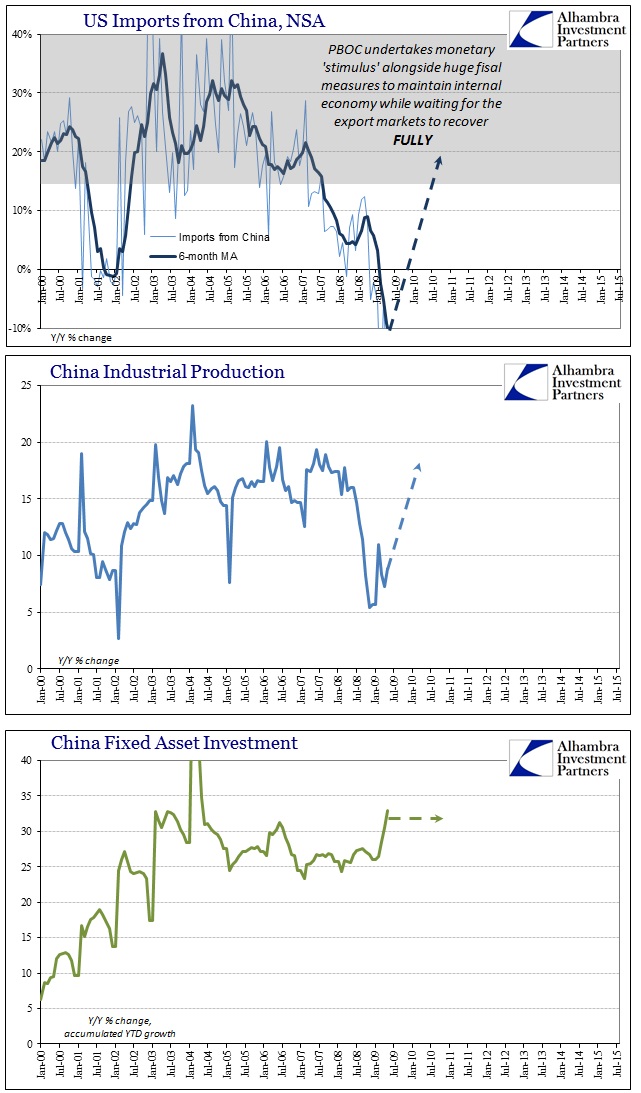

Thus, in China’s view of the Great Recession, industrial production followed US import activity but fixed asset investment was mostly stabilized (“stimulus” at “work”).

Despite renewed financial doubts in 2010, everything seemed to be working as intended and expected; not just in China, but globally. By early 2011, there was confidence enough to actually unwind (especially Europe and China).

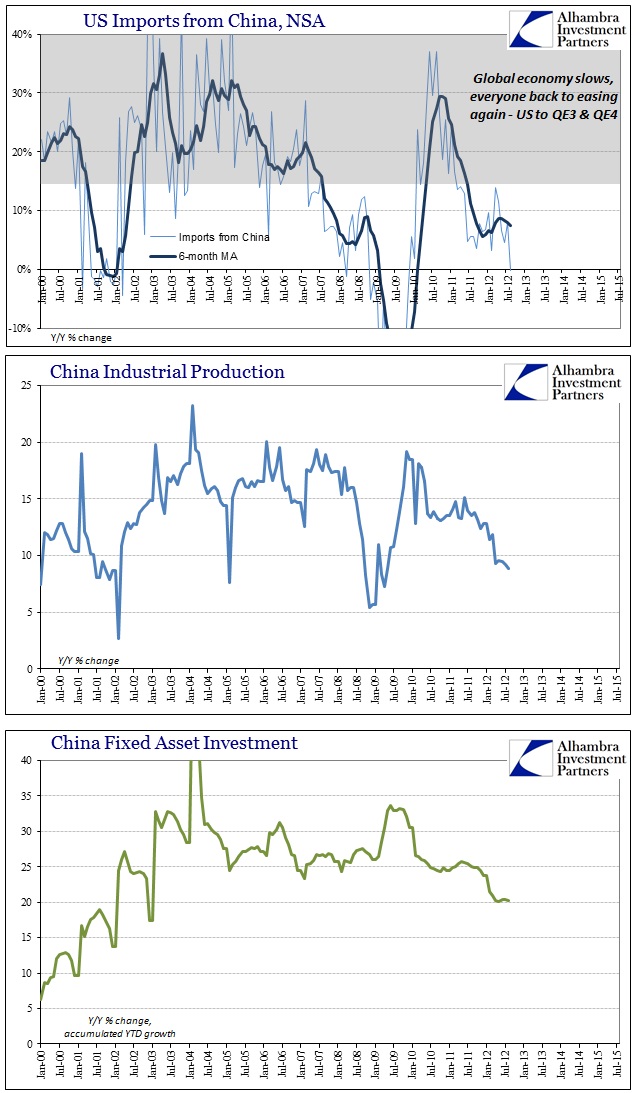

But those financial irregularities suddenly and “unexpectedly” turned into economic retrenchment by early 2012. So central banks did what they are “supposed to” and renewed all the “stimulus.” China’s government unleashed a massive spending program (RMB 1 trillion) while the PBOC aided in outward rate cuts and more directed “easing” aimed at a general flooding of financial conduits. The US Federal Reserve, for its part, engaged more QE, a third then a fourth in quick succession. All of it aimed, as that in 2009, to restore these economic channels to 2007 levels; and it was assumed that everything would follow since this was, as the Great Recession, viewed as another temporary deviation from the plucking trend.

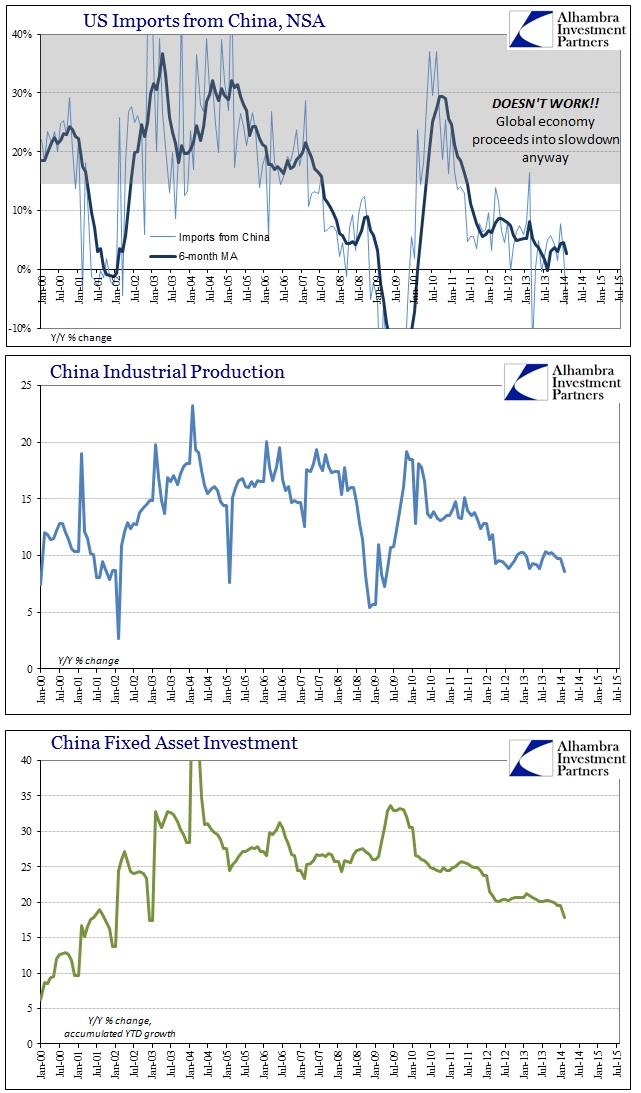

It did not work anywhere. China was the first to figure out, after two huge tries, that it would never work and getting back to 2007 was no longer possible for the global (and US) economy. Because its imbalances were so large, and bubbles so dangerous, it did not have the luxury of hanging on several more years to see if it all might come together at some point. The irregularity of the European and US economies since 2012 were just more confirmation for the theoretical motivation of this new “reform” agenda.

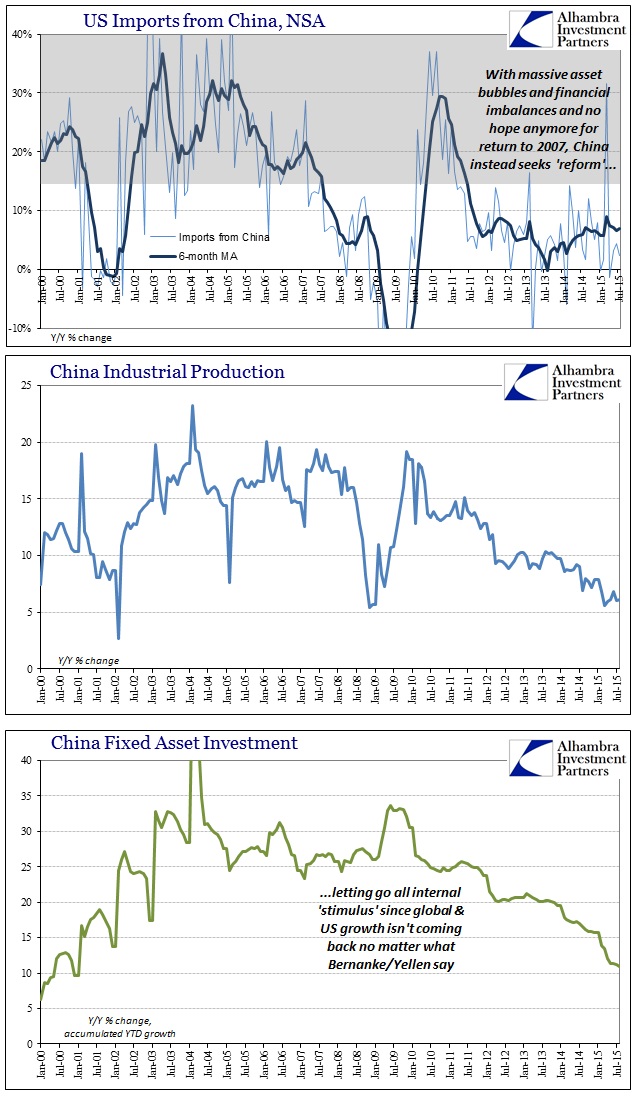

For China, reform means letting the economy go where it may while focusing as much effort as possible on potentially managing a financial reversion that hopefully does not end in total financial (and economic) disaster. While that is China’s end of the problem, it must be emphasized that it begins with the US’s distinct and continued lack of “demand” quite apart from what is suggested by the Fed’s public statements (though confirmed increasingly by its contradictory inaction).

Without either US growth or internal “stimulus” pushing further bubble imbalance, the Chinese economy is winding down toward an unknown but likely dangerous fate. Since so much of the rest of the global economy is tied in with China as the manufacturing nexus between resources (EM’s) and end markets (US, Europe), this succumbing to economic reality is the pivot between US economic decline and the world’s; their economic trouble is our economic trouble, both cause and reverberating effects.

All that is left is to assign a single cause for the second deviation (which is really the same as the first); something powerful enough to burn to ashes all the massive monetary attempts the world over.