For

This week’s report is going to deviate a little from the norm as I am just going to focus on the technical impact from the Brexit vote on Thursday, and the subsequent fallout on Friday.

First, let’s pick up with where I left off on Tuesday:

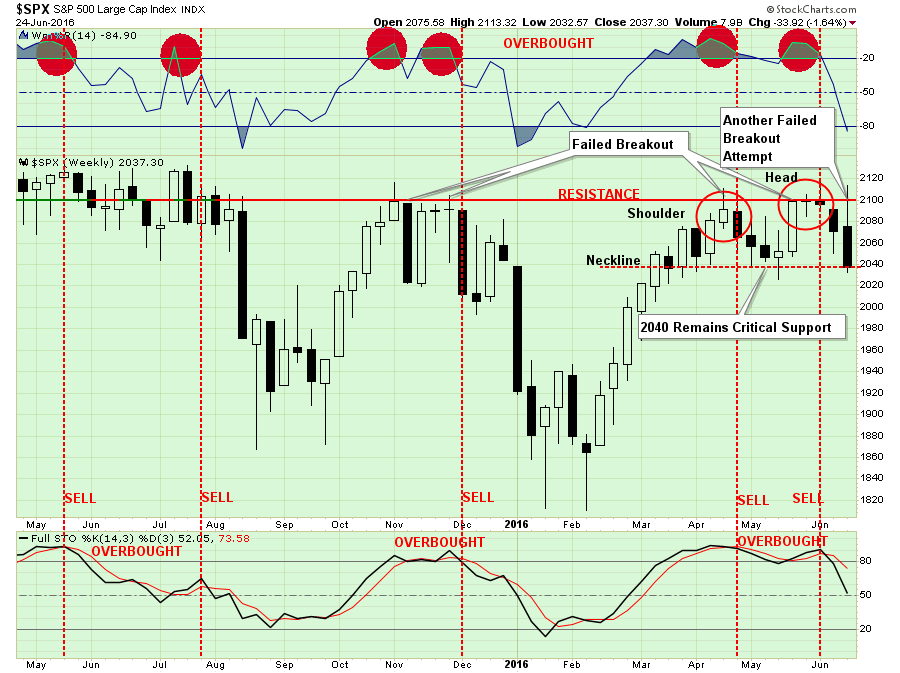

The market has repeatedly made attempts to break out above 2100. But that level has rejected investors more often than Josh Richardson at the net. (Miami Heat)

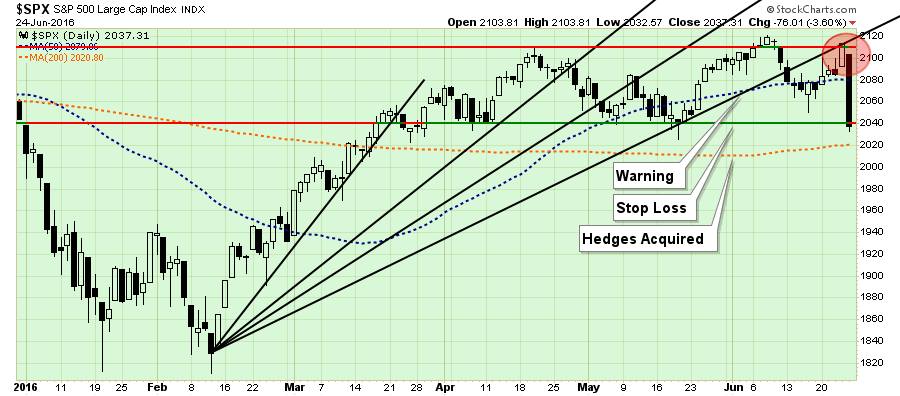

The good news, if you want to call it that, is that 2040 still contains the downside to the market currently. However, the neckline forming at 2040, on a weekly basis, will become critically more important if the development of a “head and shoulder” formation comes to fruition.

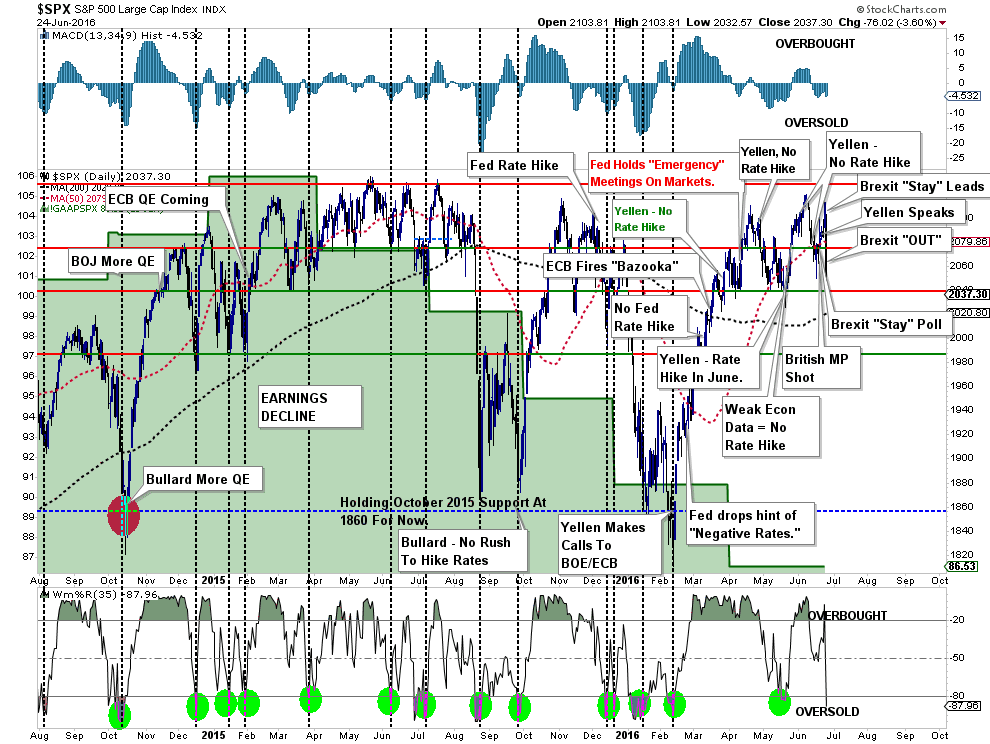

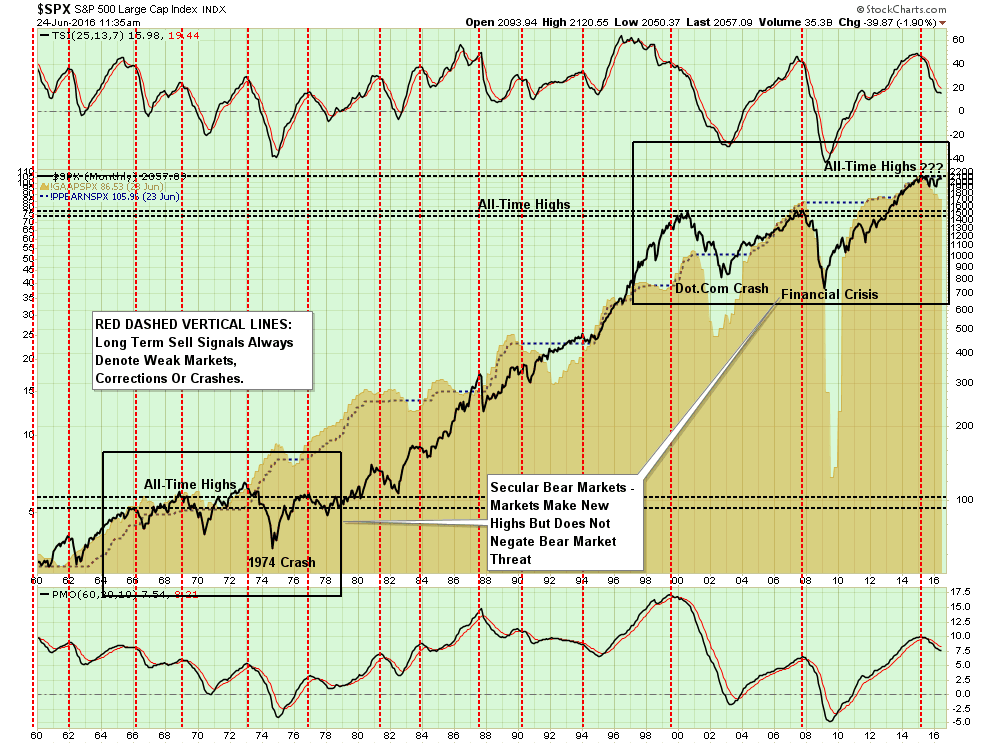

As has been the case since the beginning of the year, the markets have migrated investment strategies to follow “Fed Speak” and headline events rather than fundamentals. The annotated chart below is rapidly running out of room to notate these events while earnings continue to deteriorate.

“Of course, the market ignoring fundamentals and focusing on “Fed Speak” is not a new innovation but something seen at the peak of the last two major bull markets.”

As I have stated repeatedly over the last several weeks, with risk outweighing reward, a more cautious stance to portfolio management should be considered. It is always why I continue to hold excess levels of cash:

“However, if the holding of cash is a ‘tactical’ holding to avoid short-term destruction of capital, then the protection afforded outweighs the loss of purchasing power in the distant future.”

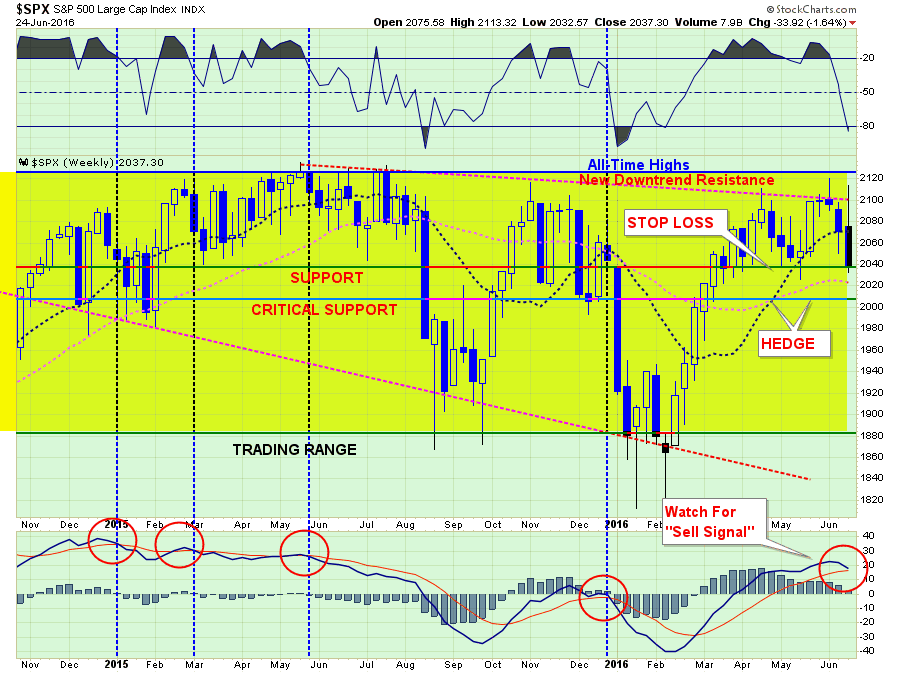

The chart below shows the now 13-month long sideways trading range of the market. However, most importantly, the downward trending price pattern remains in place. The recent failure at the downtrend resistance line remains a concern as well as the violation of the short-term moving average which has been acting as support.

The vertical blue-dashed lines denote market sell signals where subsequent price action has been poor, to say the least. While a “sell signal” is NOT CURRENTLY in place, it will not require much further deterioration in price to trigger one.

Again, as noted above, the compression that was building between the short-term moving average (blue dashed line) and the current “downtrend resistance” was due to resolve itself. The break to the downside puts 2040 support, as noted above, into focus.

The problem for investors remains the focus on short-term “hopes” rather than longer-term fundamental dynamics. The issue of such “short-termism” is such a focus has had generally poor longer-term outcomes. As discussed in the “Theory Of Bubbles”:

“History is replete with market crashes that occurred just as the mainstream belief made heretics out of anyone who dared to contradict the bullish bias.

It is critically important to remain as theoretically sound as possible. The problem for most investors is their portfolios are based on a foundation of false ideologies. The problem is when reality collides with widespread fantasy.”

DO NOTHING

Last Tuesday, while the markets were ramping higher on expectations Britain would “remain” in the Eurozone, I wrote:

“There are times in portfolio management where ‘doing nothing’ is better than “doing something.” This is one of those times.

With portfolios already running at just 50% of total recommended equity exposure, portfolio risk is already substantially mitigated. This leaves us is the best place to be for the moment as we await the outcome of the ‘Brexit’ vote on Thursday and the culmination of Yellen’s testimony on the ‘Hill.’

From that vantage point, we can then assess the markets and make a reasonable assumption about what to do next. Could we miss a bit of upside? Absolutely. But such a small lag is a much better outcome than trying to recoup a substantial loss if things go wrong.”

Well, things certainly went wrong.

However, the problem is we remain trapped in limbo. With the markets holding above supports, but still within an overall corrective topping process, there is no reason to become extremely negative on the markets at the moment OR be extremely bullish.

In other words, the only option is to continue to “do nothing” until the market resolves its current state in one direction or another.

The bad news is the longer the market remains in this current state, the risk are rising of a more substantial downside break.

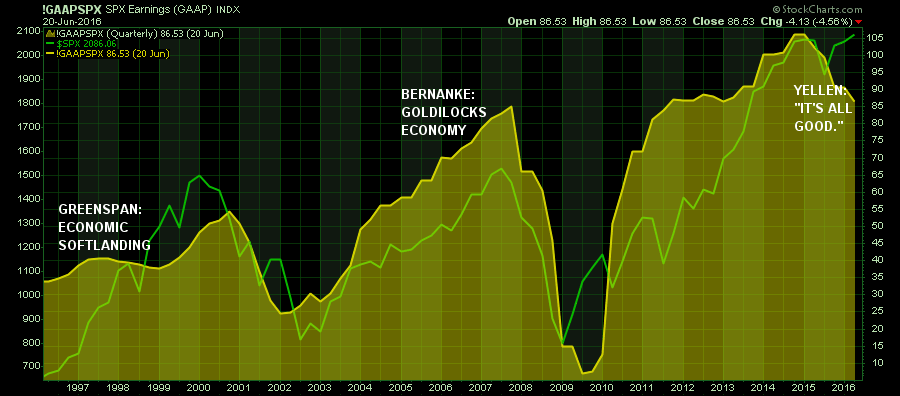

The chart below is a monthly chart of the S&P 500 with GAAP earnings and Peak Earnings shown. The current topping process, stuck below “all-time” highs, is not too dissimilar to what has been seen at previous major bull market peaks. As was the case then, “doing nothing” may be the best solution.

BACK TO FUNDAMENTALS

While the initial shake out of the markets was severe, the “shock” of the exit will be quickly absorbed by the financial markets. In the longer-term, the markets will have to come back to focus on the fundamentals, which are, to say the least, wanting.

As Andrew Lapthorne noted from SocGen earlier this week (via ZeroHedge):

“Whatever the outcome of the Brexit vote this week investors will still be facing the prospect of negative rates and negative yields on a huge range of bonds, massive corporate leverage with worryingly rising delinquencies and of course expensive equity markets and falling profits. To that extent, these political events are a distraction from the main event, weak global economic growth and perverse asset markets. So whilst the market preference for the status quo might be celebrated in the short-term, actually when the fog clears all of the problems will still be there.“

He is absolutely correct. However, this note from Nomura on Friday reiterated the point:

“In a nutshell, we expect the global impact of the Brexit to be more through the financial, confidence and psychology channels than simply through trade. Our warning is to not underestimate the depth and reach of global financial market contagion, which seems to have increased since 2008. For instance, during the European crisis of 2011, when there were significant fears of EU breakup, Asia’s stock and bond markets became much more highly correlated to the Euro Stoxx 50 and the German government bond yield than over 2000-07. And as Hyun Song Shin, economic advisor and head of research at the BIS, recently described it,“the real economy appears to dance to the tune of global financial developments rather than the other way around”, through wealth, confidence, loan collateral and liquidity effects.”

As I have written recently, the markets have been drifting from one Central Bank speech or action to the next. The disregard for underlying fundamentals is something that has only been witnessed at major market peaks historically.

Furthermore, it is virtually assured the Federal Reserve will not hike rates now. In fact, the Fed will likely not hike rates at any point in 2016.

Here are the big risks going forward as money shifts from the instability of Europe to the “safety” of the U.S.

- International and Emerging Market performance will suffer relative to domestic markets.

- USD will strengthen from currency inflows.

- Bond prices will rise (interest rates will fall further)

- Oil prices will decline towards $30/bbl.

- Utilities, REIT’s, Healthcare, and Staples should outperform the S&P 500. (This just means they won’t decline as much as the index)

- Financials, Technology, Discretionary will lag as recessionary forces pick up steam.

- Imports / Exports will continue to suffer weighing on corporate profits (fuggeta’bout hockey stick earnings recovery.)

This is just some initial outlooks. I will continue to monitor and report on these specific areas each week from a price trend basis and make adjustments/recommendations accordingly.

Of course, the reality is that we will likely see a globally coordinated Central Bank response to the financial markets over the next few days if the selling pressure picks up steam. This will come in the form:

- Further interest rate reductions

- Deeper moves into negative rate territories

- Increased/accelerate bond purchases by the ECB

- A potential short-term QE program by the Federal Reserve

- A pick up of direct equity/bond buying by the BOJ.

- Liquidity supports through FX swaps or direct intervention

- Lot’s and Lot’s of “Verbal Easing”

The problem that potentially exists, and should be paid attention to by investors, is the lack of credibility of the Central Banks themselves. If the Central Banks do intervene, as expected, there is a possibility of a “negative” response by financial markets as the veil of “an improving economic backdrop” is ripped away.

PORTFOLIO ACTIONS

While I stated above that you should “do nothing” over the next day or two until the initial “panic” subsides, it is prudent that over the next few days you continue to take prudent portfolio and risk mitigation actions.

Continue with the steps laid out in the “Monday Morning Call” Section a couple of weeks ago:

- Tighten up stop-loss levels to current support levels for each position.

- Hedge portfolios against major market declines.

- Take profits in positions that have been big winners

- Sell laggards and losers

- Raise cash and rebalance portfolios to target weightings.

Next, as shown in the chart below, tighten up “stop loss” levels and have a strategy to hedge equity risk in portfolios in the event the market breaks down.

While the 2040 level was “technically” broken on Friday, I recommend waiting until next week before liquidating positions. With the markets now very oversold on a short-term basis, a bounce early next week would not be surprising. Use any bounce to rebalance portfolios.

Importantly, I am moving the level where a “negative market (short) hedge” is added to portfolio up to 2020 from 2000. This is due to the recent rally which has pulled the longer-term moving average up to that level as shown above.

This week’s actions is the reason I have continued maintaining a large exposure to “cash” in portfolios despite much criticism. As Mohamed El-Erian discussed last week:

“At a breakfast meeting with reporters on Monday, the former Pacific Investment Management Company chief executive said central bank asset purchases have successfully decoupled asset prices from fundamentals and distorted traditional correlations.

‘Investors cannot rely on correlations as a risk mitigator, making cash a very valuable thing to have.

It can give your portfolio resilience during stressful times, optionality—whether you use it for tactical or strategic purposes and flexibility to deploy it when necessary.’

Central banks are finding it harder and harder to repress volatility in financial markets, and any jolts, such as currency devaluation in China or political events, such as Brexit, result in wild swings in the markets.’

El-Erian also said years of unconventional monetary policy, including asset purchases, and a lack of fiscal stimulus are making developed economies less stable.”

While we can debate over methodologies, allocations, etc., the point here is that “time frames” are crucial in the discussion of cash as an asset class. If an individual is “literally” burying cash in their backyard, then the discussion of the loss of purchasing power is appropriate. However, if the holding of cash is a “tactical” holding to avoid short-term destruction of capital, then the protection afforded outweighs the loss of purchasing power in the distant future.

Of course, since Wall Street does not make fees on investors holding cash, maybe there is another reason they are so adamant that you remain invested all the time.

“In a bear market, the man who wins is the man who loses the least.” – Dick Russell