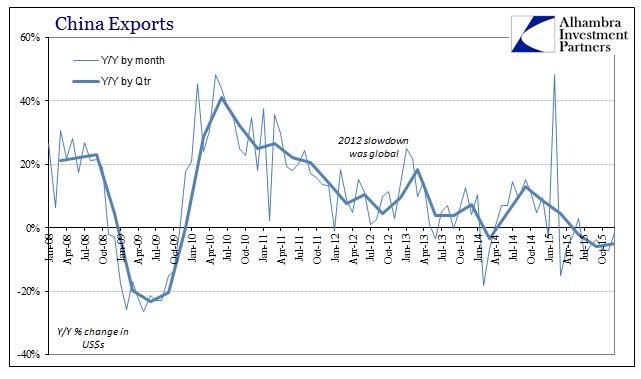

Chinese exports in December were better than feared, declining by just 1.4% against some expectations for an 8% decline. However, there were significant questions in the data, starting with year-end contract projections, unverified accounts that don’t match other countries’ trade figures and the return of Hong Kong as a potential falsification point. As ZeroHedge points out, without the huge jump in Hong Kong activity the export figures would have been more in line with recent months.

While economists were taking comfort with -1.4%, for the quarter exports declined 5.1% which was practically the same as the -5.9% from Q3. The trend is still undeniably weak, with the past five quarters projecting nothing but continued disappointment; +8.5% Q4 2014; +4.6% Q1 2015; -2.2% Q2 2015, including the last positive number for exports; -5.9% Q3 and -5.1% Q4.

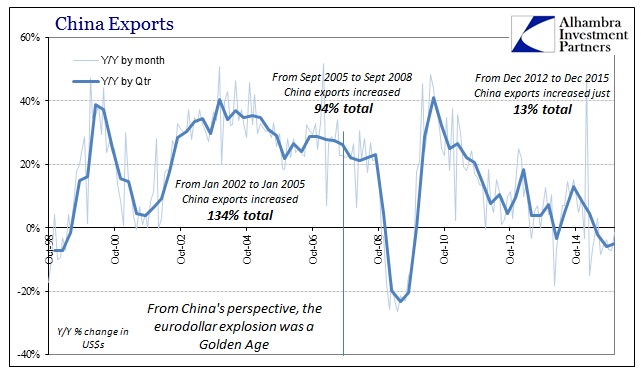

The true nature of the unfolding disaster is revealed by wider context, where the argument over whether -1.4% is really an improvement is put to rest. As noted month after month, China’s industrial capacity was built upon the premise of not positive growth but growth that averaged 20-40% year in and year out. The export numbers in 2015 confirm that either the global economy suddenly stopped buying so much of its goods from China, or the global economy suddenly stopped. Those are the only two possibilities; the only way to explain why China was exporting at 30% before 2008 and then again, briefly, just after, but now can’t even maintain a steady level.

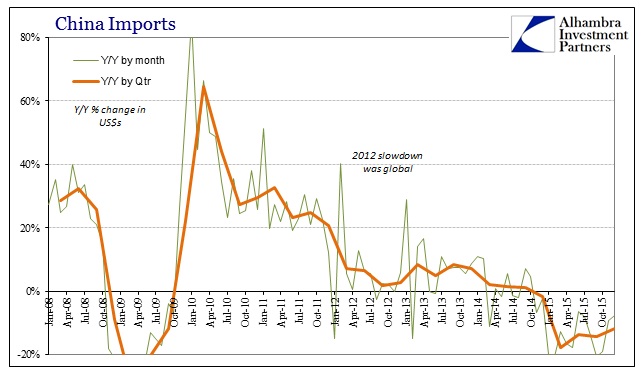

The amount of leverage that went into maintaining capacity growth even as actual activity fell off starting in 2012 is simply enormous, and that explains why so many financial fears plague almost every facet of the Chinese markets now. This would include the “dollar” connection, which has suffered the most visible nature of the disaster. I also think that helps explain, partially, why Chinese imports have collapsed at a far greater rate than exports. The troubled ability to directly source eurodollars reduces the currency available to conduct actual economic trade. Along with the internal bubble dynamics no longer supporting marginal expansion, the result is an ongoing trade disaster where China’s negative output in exports is amplified to the rest of the world via stark reductions about imports.

Here, again, the relative improvement in December’s contraction means very little. Imports fell 7.6% year-over-year against expectations of something like -12%, but for the quarter imports fell almost 12% compared to the last three months of 2014. Further, the monthly variation in growth rates (contraction rates, really) doesn’t tell us much about what to expect next month or next quarter. In June and July, imports fell “only” 6.3% and 8.2%, respectively, but the summer was followed by another wave of contraction slightly lagging the renewed financial turmoil of August and September (imports fell -20% in September and -19% in October).

With a revisit of “devaluation” and money market disorder of late, it is quite reasonable to expect further erosion in Chinese trade fortunes in the coming months (which might not be apparent until spring, well after the upcoming first Golden Week/New Year which can obscure data points from a nation already stretching credibility in more ways than one). It is a disappointing projection for not just China, but the evident and looming recessions from Brazil to Africa to even Canada.

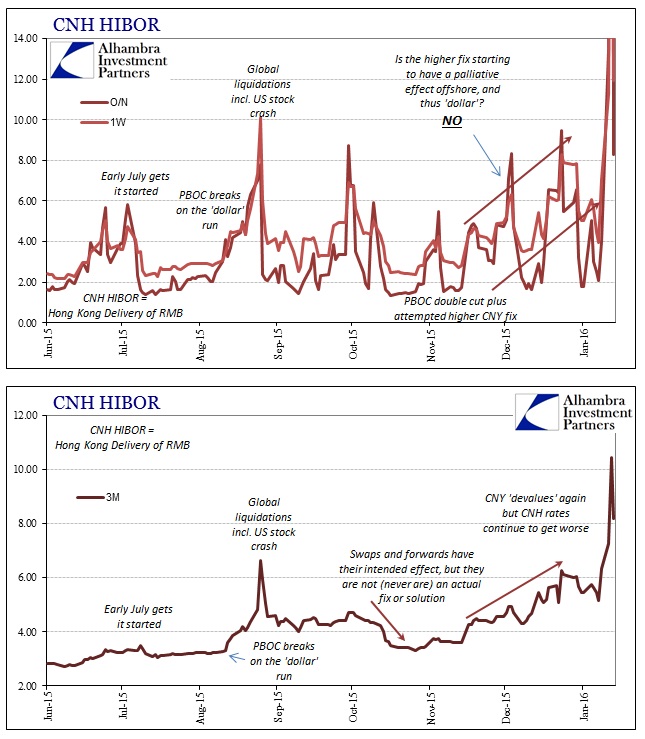

Along those lines, HIBOR rates came back down this morning from yesterday’s historic stoppage, but only by comparison to the previous day could they be taken as an improvement. The overnight CNH rate moved back to 8.31% from the ridiculous 66.8% yesterday, but 8% is still troubling. The 1-week rate still registered at nearly 12%, while the more important 3-month rate declined only to 8.192%, meaning the second highest rate ever recorded.

In other words, if China’s trade follows China’s finances again then we might expect not just renewed weakness but perhaps seriously so in the months ahead. As it was, Chinese officials had targeted +6% growth in total trade for 2015 but serious financial disruption (the “rising dollar”) instead brought about -8% for the year. Starting out 2016 already in that category is an ominous sign for the global economy, not just China.