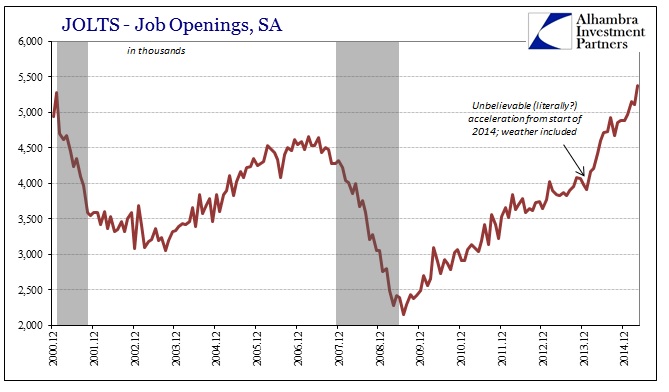

The latest updates for the JOLTS showed that job openings in April surged to a new series high. Jumping by 267k (seasonally adjusted), the trend in job openings is being used as confirmation that there must be some robust underlying trend in overall payrolls despite the ubiquitous slump everywhere else. In other words, this is another series from the BLS that appears to be confirming the Establishment Survey’s view on the economic pickup.

“This is more confirmation that the economy is indeed emerging from that soft patch in the first quarter and can still pick up even faster in the next few months,” said Chris Rupkey, chief financial economist at MUFG Union Bank in New York.

Job openings, a measure of labor demand, rose 5.2 percent to a seasonally adjusted 5.4 million in April, the highest level since the series began in December 2000, the Labor Department said in its monthly Job Openings and Labor Turnover Survey (JOLTS).

Ever since the start of 2014, weather be damned, the pace of job openings has simply decoupled from all perception except the Establishment Survey. While that offers “more confirmation” for economists, in reality it amounts to the same confirmation. The JOLTS survey is benchmarked to the BLS’s Current Employment Situation (CES), meaning that if there is a trend-cycle problem in the mainline payroll report it will passed along, directly, to JOLTS.

From the BLS itself:

JOLTS total employment estimates are benchmarked, or ratio adjusted, monthly to the strike-adjusted employment estimates of the CES survey. A ratio of CES to JOLTS employment is used to adjust the levels for all other JOLTS data elements.

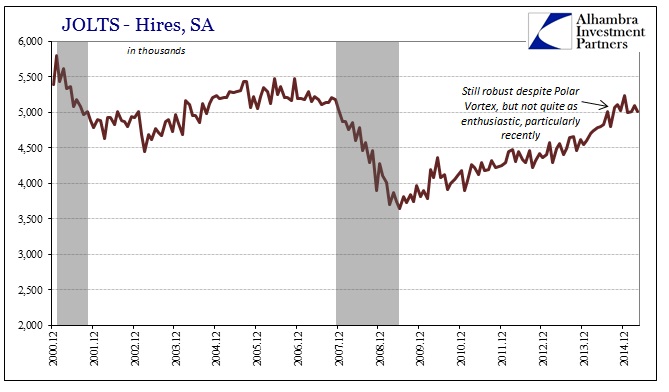

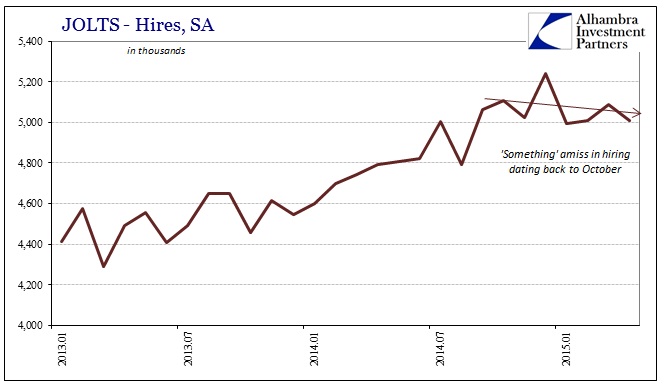

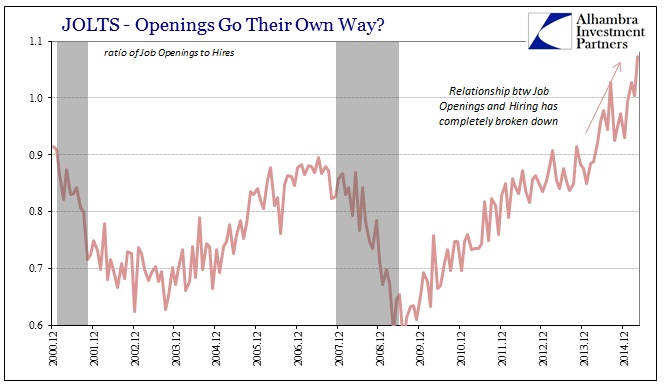

Given that baseline, it would be highly suspect and relevant only where the JOLTS figures diverge from the Establishment Survey. While none of the components had done so for most of 2014, that isn’t the case more recently. While Job Openings have supposedly surged, the hiring rate has not. Dating back to last October, hiring appears to have frozen if not slightly declined.

If I am correct about the benchmark in trend-cycle inputting serious upward bias into the CES, that would also mean the same upward bias in JOLTS, which may further suggest that hiring is worse than even the slight downward trend shown above. The lack of inflection in job openings is puzzling, to say the least, except that job openings have always (going back to the 2000 inception) exhibited a much higher beta. Even with that in mind, the divergence in late 2014 has become almost ridiculous.

That is especially true of 2015 so far, where Job Openings have no fear of anything, but hiring more than suggests the same “slump” that has appeared more universally. Economists have already come up with an “explanation” for this disparity:

Hiring slipped to 5.0 million from 5.1 million in March. Economists say the lag in hiring suggests that employers cannot find qualified workers for the open positions.

That proposal would tend to suggest a shortage in the labor market, an end to the “slack” that has debilitated a great deal of the recovery these same economists have been searching for. Basic economics, however, away from the econometric models, gives us the expectation for rapidly rising “P” for wherever “demand”, in this case for labor, far outstrips “supply” as it would clearly have to be doing if JOLTS presents a realistic scenario. That rising “P” would be wages, which would make sense as businesses that cannot find enough “qualified workers” in a more rapid economy will have to pay up to entice them.

The problem with that view is, obviously, no wage growth is apparent anywhere. There has been ample time to accrue through any lags, as the jump in Job Openings far and above Hiring dates back, again, through the trend-cycle bump in early 2014.

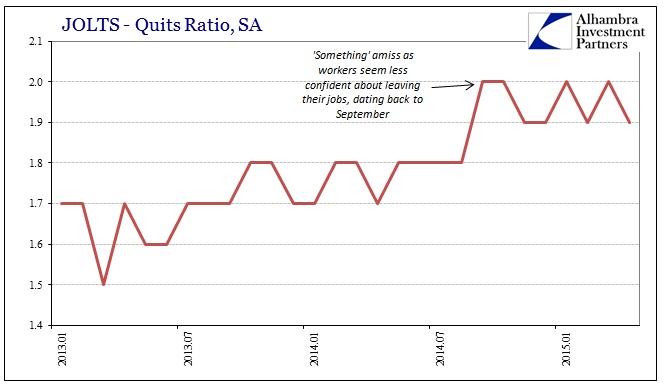

Beyond wages, any surge in openings would likely induce greater overall turnover. Even when there may not a huge difference in pay between an existing job and a new opportunity, a plethora of real openings and a shortage of qualified candidates would offer a compelling reason to be choosy – less likely to stick with a job demanded workers may not be satisfied with. The ratio of “quits”, the JOLTS view on just this activity, did find an increase in voluntary turnover during the middle of last year, but that trend seems to have died, again, right around September or October.

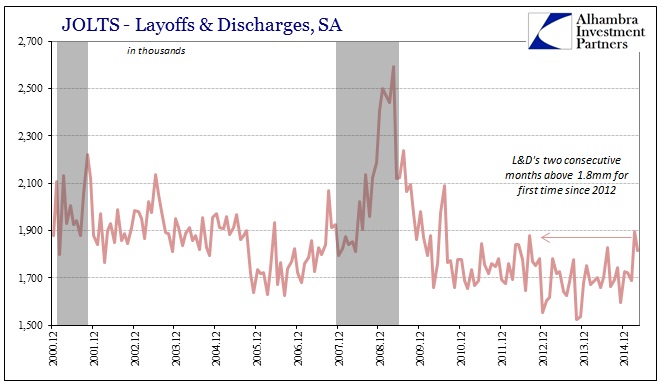

In other words, if there were a sharp and fierce end to the destabilizing “slack” leftover still from the Great Recession, there is scant evidence for it aside from Job Openings that follow closely none other than the CES benchmarking itself. There is, though, one part of the JOLTS dataset that did jump up in the past few months, but it is contradictory to all the happiness over Job Openings: Discharges and Layoffs.

For the first time since the 2012 slowdown, layoffs and discharges were estimated above 1.8mm for consecutive months in March and April; March’s figure of just shy of 1.9mm was the worst months since the middle of 2010! The 6-month average is up to 1.74mm, which is the highest since November 2012, about equal to the estimates for the middle of 2007.

If you accept that the payroll figures represent a truer picture of the economy, then you must at least question what is taking place in 2015 (dating back to last autumn). If there were a robust jobs expansion starting early last year, then it must be considered more than somewhat suspect this year so far. Nonconformity in hires, quits and now layoffs call further into question both openings and the overall employment narrative, not the least of which traces back to the fact that they all share the same benchmark and subjective biases.

The other interpretation, which I obviously favor, is that the surge last year amounts to nothing more than those subjective benchmarks, but that the turn or inflection in late 2014 and into all of 2015 is very real and therefore seriously understated – that it has shown up at all despite the obvious upward bias in chained variation is itself the most significant aspect in all of this. That view would be all the more concerning if it occurred where last year’s upside never truly did. For such a celebrated employment report here as in JOLTS for April 2015, there really isn’t much to be confident about. Job Openings were terrific, except everything else disagrees.