These may be desperate times indeed, where every small piece of anything not wholly dismal is singled out as the indicator that either the worst has passed or it never was. I am simply at a loss to describe housing construction figures in such unequivocally glowing terms. For the most part, construction activity hasn’t deviated at all from its trend in 2014. The only difference, and the facet being overly hyped, is that real estate activity rebounded in April from March and February. From that all lines are extrapolated straight up:

U.S. housing starts jumped to their highest level in nearly 7-1/2 years in April and building permits soared, hopeful signs for an economy that is struggling to regain strong momentum after a dismal first quarter.

The strength in housing is in stark contrast with weakness in consumption, business spending and manufacturing, which has prompted economists to lower their second-quarter growth estimates and raised doubts that the Federal Reserve will raise interest rates before the end of 2015.

“The stronger starts and permits data suggests that some real gauges of economic activity may finally be starting to accelerate during the spring, increasing optimism that the Fed may be on track to hike rates later this year,” said Gennadiy Goldberg, an economist at TD Securities in New York. [emphasis added]

If you can find anything different in these figures that suggest a major upward shift in the economy, then that would be an accomplishment. This is a very tenuous read on these factors especially of that second paragraph, as “stark contrast” really isn’t so much (see below) and is in no way of any sufficient scale to counteract a consumer recession. In other words, comparing housing in April to the declines in “consumption, business spending and manufacturing” is a logical fallacy of order of magnitudes.

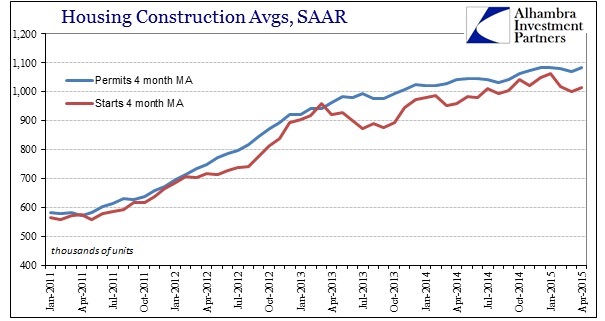

As the Census Bureau itself advises, month-to-month variations should be ignored and that a 4-month average is a much better gauge of actual trends. So the sharp jump in April does not accomplish much of anything except partially retrace the “hole” from the winter. In terms of starts, it wasn’t even that good as April’s estimates only bring activity back up to where it was last September.

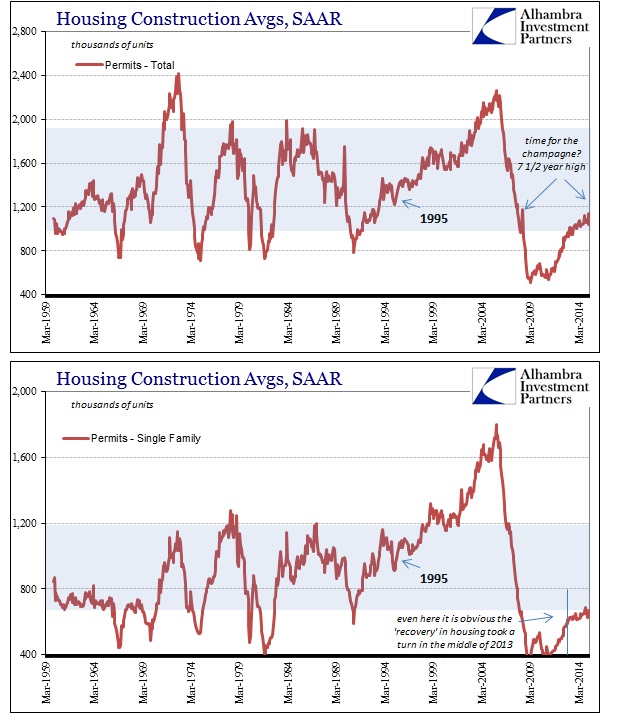

As it is, all this amounts to splitting hairs as a seven and a half year high sounds great for setting a narrative, but comparing to 2008 misses the point entirely; the housing bubble had already mostly collapsed by then. In terms of the overall economy, the level of housing construction remains at levels once reserved for recession. Context matters and it is being ignored purposefully.

Even in the stunted “recovery” in single-family housing it is still clear that there was a sharp deviation from the 2011-12 mini-bubble right around the middle of 2013 (taper selloff). For housing to be anything like an economic force again, not only would that growth rate need to return to the mini-bubble pace but remain at blistering acceleration for probably four or five years without interruption.

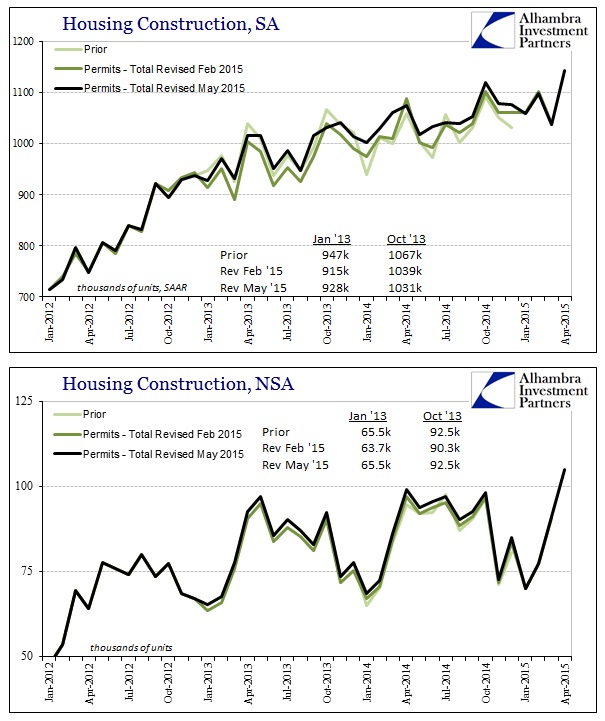

Any interpretations of these figures are further clouded by the constant revisions, including another major change going back to 2012 (after especially the permits series was revised only three months ago). Worse, it appears that most of the revisions to prior years was nothing but adjustments to seasonal adjustments (to what end could the seasons be shifting years afterward?).

Comparing revisions to the unadjusted series, it is clear that the Census Bureau is revising data based on perhaps new benchmarks and adjustment regressions that have left the data smoothed out in terms of SAAR. In 2012 and especially 2013, there doesn’t really seem to be much consistency in how these revisions were carried out (in the unadjusted series, the May revisions simply “unwrote” the February revisions, but in the adjusted series, as shown above, the revisions left changes and not always in the same direction).

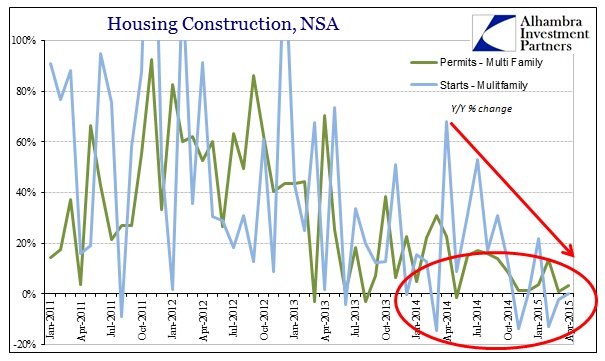

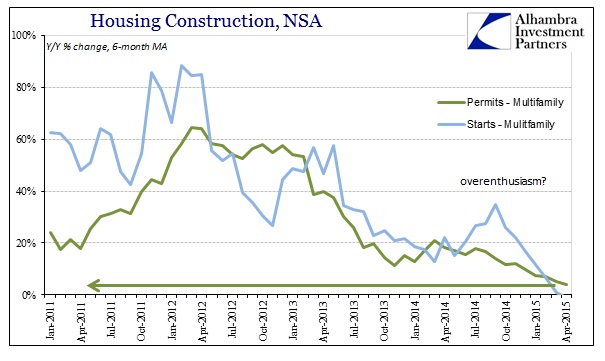

Splitting hairs or not, revisions or not, the most important data in the entire sector remains apartment construction. If there was one indication of actual economic direction, apartment building would be it as it relates directly to wages and the abilities of Americans to create new households. At the very least there should be activity consistent with population growth, and anything short of that is a clear warning. Without an re-opened mortgage avenue, and with new young adults highly saddled now with immense student loan debt, the increase in rentable space is the most sensitive to macro changes (factoring the financial end, including institutional “investment” that has very much faded).

Despite the encouraging words from all economists, apartment-focused activity has sunk to new lows for this “cycle.” Overall permits may be at a seven and a half year new high, in adjusted terms, but starts of new multi-family units were flat year-over-year in April after falling 13% in February and 2.4% in March. Multi-family permits were up just 3.2% in April, after rising Y/Y only 1% in March; in sharp contrast to 2012 which averaged Y/Y growth in multi-family permits of 57.5% where the worst month, by far, was +26.6%.

In fact, the 6-month average of Y/Y growth in starts is negative in April for the first time since July 2010! If we are using multi-year benchmarks, that is the only one that should count here. It is exceedingly difficult to find even a housing rebound in this morass of stochastic values, of any real consequence, let alone the sole hope for an economic one.