“

80% Or Bust

Not surprisingly, the recent sharp reflexive rally has brought the bulls out in full force as noted by a recent comment on my post earlier this week on “4% From The Highs:”

“…by the time you get confirmation with the long term indicators above, you will miss out on 20 to 30% of the rally.”

It’s a fair point if you are a short-term trader looking to time the market. I’m not. As a long-term investor, and specifically as a manager of “other people’s money,” I am much more concerned with the specific inflection points where market dynamics change from a generally positive trend, to a negative one.

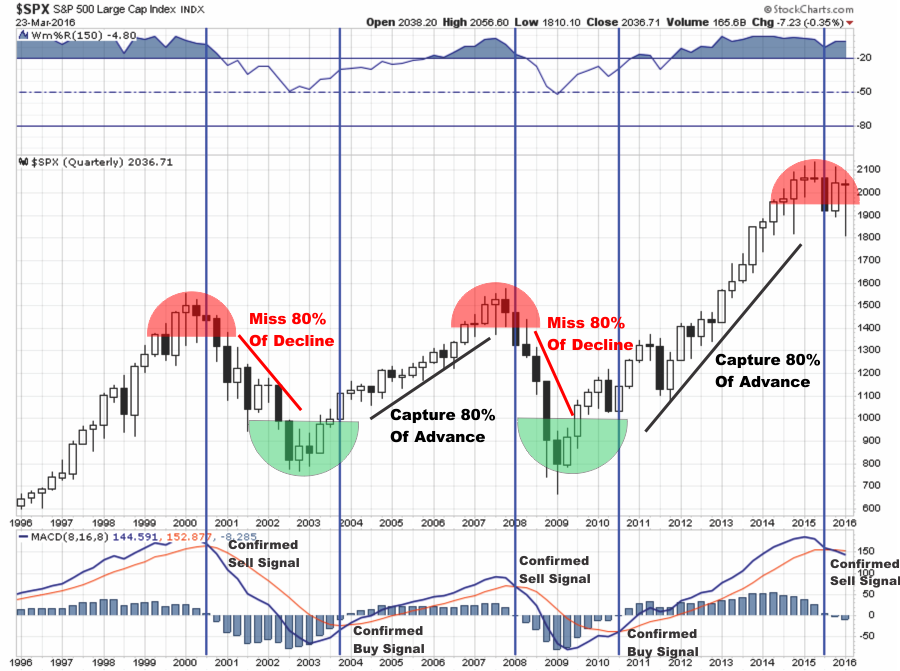

Yes, I will most definitely miss both the bottom and the top of markets. As shown in the chart below, the technical indications of a change in trend are slow to occur. However, I am only really concerned with capturing, or missing, the 80% between the tops and bottoms of major market cycles.

Further, the majority of the “Best-10” and “Worst-10” days are contained primarily within those 80% spans.

So, yes, I am absolutely going to be “wrong” at the tops of markets and at the bottoms while I await confirmation of a longer-term “trend” to emerge. For those that are inherently “bullish” who choose “hope” over what prices are “actually” doing, the historical outcomes have been brutal, to say the least.

As I have said before, my methodologies are my own. They are not new ideas. They are not innovative. They are simply the lessons I have been repeatedly taught over the last 30-years of managing money. If the markets reverse the current long-term sell signals, I will happily put a lot more money to work. Until then, I will wait rather than trying to “draw to an inside straight.”

Think about it this way – if betting in the markets was really the way to build wealth, wouldn’t the vast majority of Americans be wealthy versus just the top 1%? Just a thought.

Mind The Gap

I have discussed the problems with earnings and earnings estimates in the past stating:

“In a 2010 study, by the McKinsey Group, they found that analysts have been persistently overly optimistic for 25 years. During the 25-year time frame, Wall Street analysts pegged earnings growth at 10-12% a year. Unfortunately, earnings only grew at 6% which, as we have discussed in the past, is the growth rate of the economy.”

“The McKenzie study also noted that on average “analysts’ forecasts have been almost 100% too high” which leads investors to make much more aggressive bets on the financial markets. “

My friend Salil Mehta from Statistical Ideas recently published a great piece on this issue.

“The gap between the 2016 forecasts and the YTD returns through January is 13% (8% target minus the -5% YTD). Annual returns have a nearly 20% standard deviation (or 19% if you only look from the end of January onward). So it is still plausible — though rather unlikely, with only a one in five probability — to reach the 8% target gain for 2016. (For statistics wonks, the test statistic decomposes the 13% gap to a ~9% move in addition to the typical 4.5% annualized return, and then factors in a 19% standard deviation.) Now that we are further into the year (mid-March), euphoria and complacency are back to extreme market top levels.

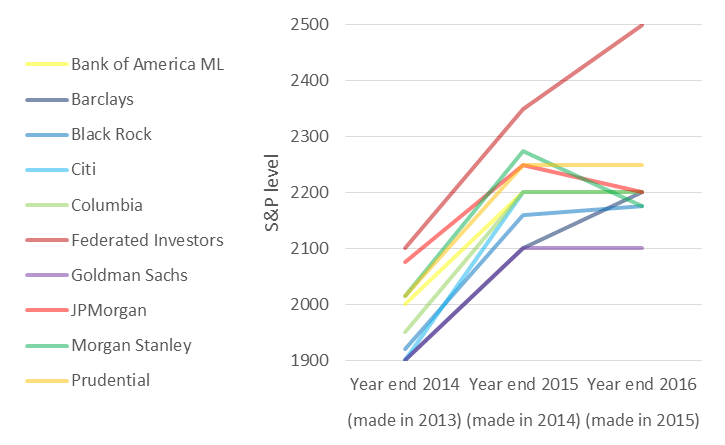

It’s also worth noting that strategists at major firms are consistently bullish, year after year. The sources of the most optimistic prognostications also don’t change. Sorted from most to least bullish, they are Federated Investors, JP Morgan, Prudential, Bank of America, and Columbia.”

“In the table below, two pieces of information averaged among the 10 firms listed above are presented:

- The difference between the target and the January YTD returns.

- The rest of the year returns.”

“If these analyst forecasts were mostly in the right direction, you would expect a positive linear relationship between 1 and 2. Regrettably, there is a negative relationship instead. Never mind that the market continued its drop in February, even after the revised forecasts, and the rebound leaves the market still below many firm’s 2016, 2015, and even 2014 targets!

In other words, the larger the gap in January between the YTD returns and the year-end target, the more unlikely the chance the market will recover to the target by the year’s end.

Think about this: For 2016, the 13% gap noted earlier (after the standardization adjustment) is the largest gap among this data.”

As Salil concludes. “That’s not a good omen.”

It’s A Bunny

Since it is Easter, I will leave you with a story about a bunny.

James Paulsen, Chief Investment Strategist for Wells Capital Management, recently penned an excellent piece with respect to the ongoing “bull/bear” debate.

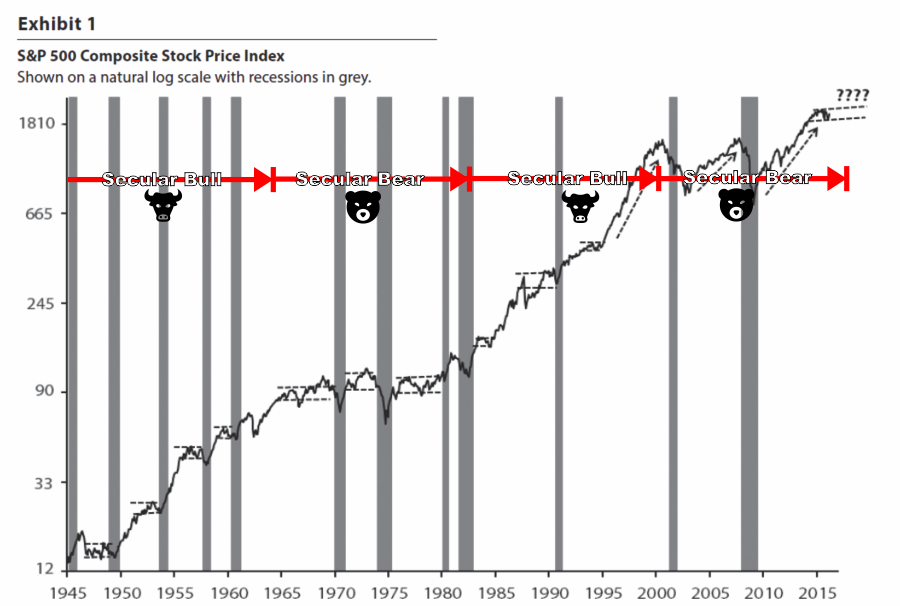

“The accompanying exhibit illustrates the U.S. stock market since WWII with recessions shown by the grey bars. In the last two expansions (during the 1990s and again in the 2000s), the stock market was uninterrupted by a bear market posting solid and steady returns until the economic recovery ended with a recession. So far, despite some volatility in 2011, this has also characterized the contemporary bull market. Without a bunny market in more than 20 years (as shown in Exhibit 1, the last bunny market was in the mid-1990s), most investors currently seem to accept that either the bull market will soon resume or we are nearing the end of this expansion. Since there has not been one in some time, few consider that stocks could simply be headed for another bunny market.”

“Most bunny markets occur in the latter part of an economic recovery. Stocks initially recover aggressively after a recession. However, as the recovery matures, cost-push pressures, inflation, and higher interest rates begin to pressure the bull market. This often resolves into a bunny market for the balance of many economic recoveries.“

I have modified his chart to notate both secular bull and bear market periods. During secular bear markets, as we most likely currently remain in, volatility swings and prices declines are substantially larger than during secular bull market periods. This elevates the risk of emotionally driven investment mistakes during periods of markedly higher volatility which leads to lower rates of investor returns longer term.

Just some things to think about.

Happy Easter.

Lance Roberts

Lance Roberts is a Chief Portfolio Strategist/Economist for Clarity Financial. He is also the host of “The Lance Roberts Show” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, and Linked-In