By Tyler Durden at ZeroHedge

While China’s currency devaluation has, alongside the price of commodities, become one of the two key drivers of market volatility and tubulence around the globe, when it comes to risk, one far more important Chinese metric is the actual amount of capital that leaves the nation.

The reason for this is that as explained over the weekend, in a world where Quantitative Tightening by EMs and SWFs has emerged as a powerful counterforce to Quantitative Easing – or liquidity injections – by developed central banks, what matters for global risk levels is the net effect of these two opposing money flows.

Of all the global “quantitative tighteners”, the biggest culprit is China, which has seen over $1 trillion in reserve selling since the summer of 2014, the direct result of a virtually identical amount in capital outflows.

Furthermore in for a “closed’ Capital Account system like is China, the selling of FX reserves is a direct function of capital outflows, so the only real data needed to extrapolate not only the matched reserve selling and thus Quantitative Tightening, but also the direct impact onglobal risk assets, is how much capital outflow has taken place.

This takes place in one of two ways: by relying on official Chinese historical data, or by estimating how much outflows take place on a concurrent basis, thus allowing one to estimate how much capital is flowing out in real time. Indicatively, China’s SAFE released onshore FX settlement data for the whole banking system (PBoC+banks), suggesting some $97bn of FX outflows in Dec, which is broadly in line with the fall in official reserves.

But much more important is the question what is taking place right now, the answer to which can either wait until SAFE releases January data in several weeks… or rely on day to day estimates of outflows in the form of central bank FX intervention.

Luckily, we have just that.

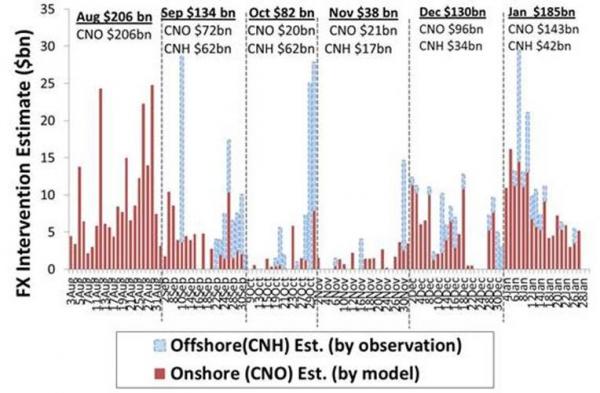

According to a Goldman report, so far in January “there has been around $USD 185bn of intervention (with the recent intervention predominantly taking place in the onshore market)” split roughly $143 billion on the domestic side and $42 billion on the offshore Yuan side.

This would make January the month with the second largest amount of intervention since August 2015, and thus the second highest month of capital outflows, and would explain the ongoing deterioration across global asset classes as China’s various FX reserve managers have been forced to sell not just government bonds but equities as well.

Goldman also calculates that “total intervention over the last 6 months, using our estimates, sums to USD 775bn.” Run-rating this amount would suggest that nearly $1.6 trillion in Quantiative Tightening is taking place just due to China’s attempts to stem capital flight. This number excludes the hundreds of billions in reserves that all other petrodollar and EM nations have to liquidate as well to prevent the rapid devaluation of their own currencies as the world remains caught in the global dollar margin call we first explained in early 2015.

The implications from this are two-fold:

- For the selling culprit, responsible for the recent market weakness look no further than China, whose reverse “flow” has been responsible for the terrible start to 2016 capital markets.

- For the Beijing politburo, halting capital outflows is becoming a matter of life or death, because there are only so many liquid reserves China can liquidate before it enters dangerous territory; worse, the less the reserves, the greater the desire will be on behalf of the local population to take their money and run.

Of course, China’s rabid defense of further capital outflows means that its original intent, to devalue the Yuan to a degree that boosts its economy via exports, has been put on hiatus, or in other words China is trapped, and instead of an external rebalancing it is forced to boost its economy in the one way it knows best: by issuing ever more debt. However, with China’s total debt now estimated at 350% of GDP, it only has a finite amount of time before the debt bubble finally pops as well.

In other words, for China there is, as of this moment, quite literally no way out, and what’s worse the longer it delay the decision of how it will reset its economy, the worse it will be for global risk markets.