The Philadelphia Fed Bloomberg Consensus for the Philly Fed manufacturing index was 9.4. The index came in -6.3.

Highlights

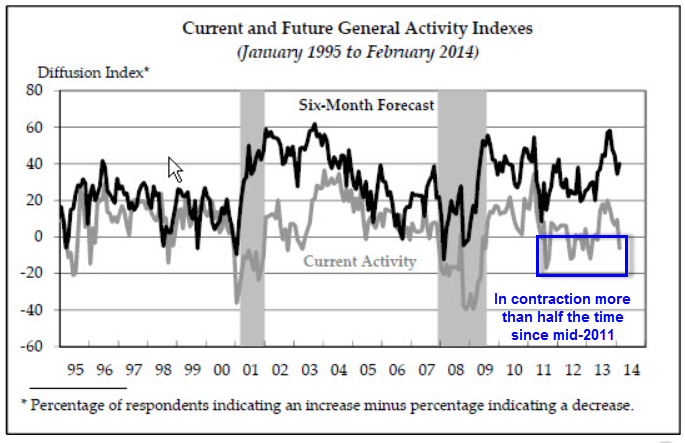

The Philly Fed’s headline index for general conditions fell back into the negative column, to minus 6.3 vs January’s 9.4. This is the first negative reading since May.

Last month’s big 7.8 point decline in the new order index signaled the trouble for today’s report. And new orders are even worse for February, in negative ground at minus 5.2 for a major 10.3 point decline. Unfilled orders are also in negative ground, at minus 2.6 for a 1.6 point decline from January.

Shipments, suffering from a lack of orders and also from weather effects, fell dramatically, down 22 points to minus 9.9. The weather effect is evident in delivery times, which slowed 5.7 points to 2.9.

Weather is a temporary effect and isn’t holding down the longer term outlook in the sample as six-month readings are all strongly positive led by a 6.8 point gain for general conditions to 40.2.

The Philly Fed report doesn’t usually cite commentary but it does for February, saying respondents attributed much of the month’s weakness to severe winter weather. But January also was hit with severe weather.

Philly Fed Diffusion Index

Chart from the February 2014 Philly Fed Report

Manufacturers Optimistic

Special questions show manufacturers are generally optimistic looking six months ahead.

Over 45 percent of the firms characterized the demand as increasing, while 19 percent indicated it was decreasing. The largest percentage (43 percent) indicated that demand had increased modestly. Firms were also asked to provide estimates of production growth for the first quarter. Significantly more firms indicated that production would increase in the first quarter (55 percent) than indicated it would decrease (28 percent), and the average growth for the reporting firms was 0.5 percent. Over half of the firms indicated that production growth would represent an acceleration compared with the fourth quarter.

Firms also remain optimistic about the growth of overall manufacturing activity for the next six months. This month, the future general activity index increased 6 points, from a relatively high reading of 34.4 in January, to 40.2 . Indexes for future new orders and shipments also remained at relatively high levels, with nearly half of the firms expecting increases in both over the next six months. The future employment index was virtually unchanged at 16.5, with nearly 27 percent of the firms expecting increased employment over the next six months.

Expectations nearly always exceed reality.

Unexpected Happens Again

- Japanese GDP and Exports Seriously Underperform Expectations

- Followed the unexpected decline in industrial production (the most since May of 2009) which followed

- The unexpected decline in retail sales which in turn followed

- The unexpectedly weak jobs report in February

- Which followed a Huge Miss in ISM; Largest Decline in New Orders in 4 Years

- Which followed a Big Miss: Nonfarm Payrolls +74,000 vs. 205,000 Expected in January

Mike “Mish” Shedlock

http://globaleconomicanalysis.blogspot.com