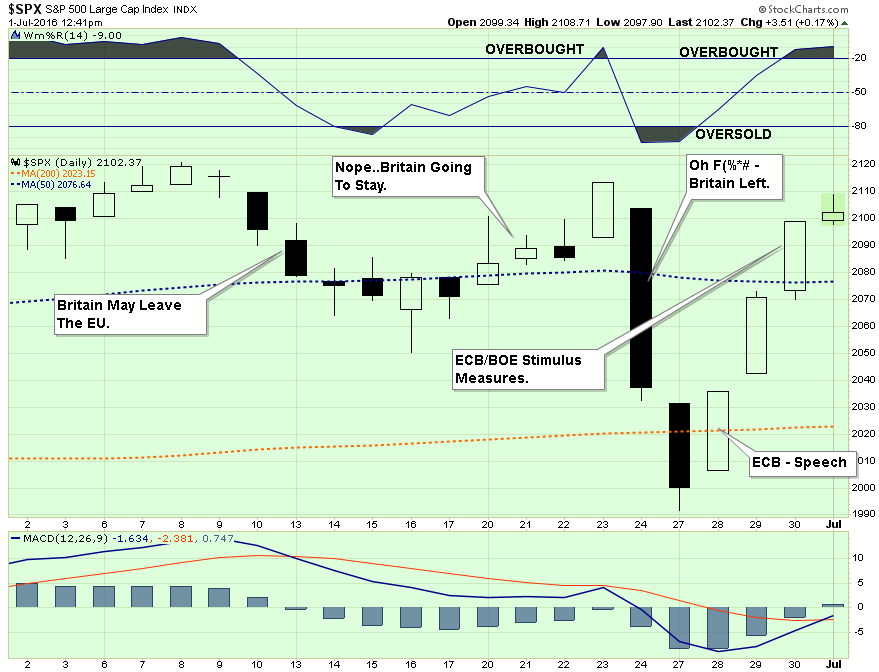

With the markets closed on Monday for the annual “Independence Day” holiday, the technical analysis from the past weekend’s missive still holds. As I stated:

“I discussed the likelihood of Central Banker’s leaping into action to stabilize the financial markets following the British referendum to leave the E.U.

Then on Thursday more announcements came from both the Bank of England and ECB:

- BOE: SOME MONETARY POLICY EASING LIKELY OVER SUMMER

- BOE: MPC WILL DISCUSS FURTHER POLICY INSTRUMENTS IN AUG

- ECB: TO WEIGH LOOSER QE RULES AS BREXIT DEPLETES ASSET POOL

- ECB: OPTIONS TO INCLUDE MOVING AWAY FROM QE CAPITAL KEY

- ECB: CONCERNED ABOUT SHRINKING POOL OF ELIGIBLE DEBT

“While many had predicted a market crisis of magnitude stemming from the “Brexit” vote, the reality was a 100-point swing in the markets in just one week. No matter how you bet, you were probably wrong.”

“So, yes, from “Brexit Fears” to “Brexit MEH” in just one week. Talk about volatility.”

Over the weekend, the Bank of England (BOE) took further action to stabilize currency and bond markets yesterday:

“The Financial Policy Committee’s measures on Tuesday included reducing capital requirements for banks, which Carney called a “major change.” The countercyclical capital buffer was cut to zero from 0.5 percent of risk-weighted assets, a move the FPC said would raise the capacity for lending to companies and households by as much as 150 billion pounds ($197 billion).

The buffer — designed to be bolstered in good times and eased in downturns to support lending — had been increased, effective in March next year. Officials now see it staying at zero until at least June 2017.

Carney and the FPC gave a stark warning to banks that they should not use the extra funding they now have to increase dividend payouts.“

I am sure the banks will absolutely NOT use the funding for the creation of additional profits or increasing payouts to shareholders. (sarcasm)

Of course, while everyone is currently focusing on Britain following the recent referendum, it is a variety of other issues that are weighing on the markets.

- Bear Stearns 2.0: Standard Life & Aviva Property Halt Redemptions (Zerohedge)

- The Italian “Debt Job”, The Next Crisis (WSJ)

- Swiss Yield Curve Negative Out To 50 Years (Zerohedge)

- China’s Debt Frenzy Leading To Depression Event (MarketWatch)

- Bond Yields Pricing In Something Very Bad (The Telegraph)

While global Central Banks continue to perpetuate the illusion that “everything is going according to plan,” the reality is the debt bubble has only grown bigger. Of course, while Central Banks continue to “rearrange deck chairs” by shuffling bad debt around the globe and fostering continued bailouts of banks and hedge funds, the “ship is still slowly sinking.”

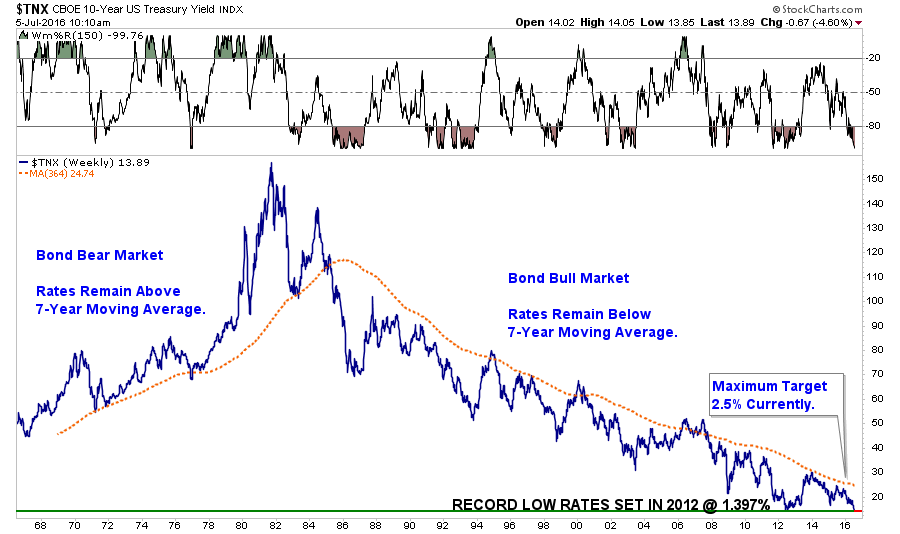

What Do Bonds Know?

This brings me to my point for today. Central Bank interventions are creating a massive debt bubble by encouraging speculation in the riskiest of debt structures by institutions. Of course, why wouldn’t institutions buy high-risk debt when they are backstopped by Central Banks in the event of a creditor default. Of course, that speculation, demand for bonds, continues to drive interest rates lower as money chases yield.

This morning the interest rate on the 10-year U.S. Treasury reached 1.39% which is the lowest level on record following the 2012 low as the nation fretted over a “debt default from a Government shutdown.” Of course, falling U.S. bond yields at that time, as investors piled into U.S. debt for safety, showed that fears of a default were unprecedented.

Today, investors are piling once again into the safety of the U.S. Treasury for a higher yield versus just about every other creditworthy sovereign issuer globally.

It is also worth noting that the current market action following the “Brexit” is not so dissimilar to what we saw in 2008. From the WSJ:

“After Lehman Brothers fell over in September 2008, equities slumped, then rallied back to their previous levels within a week. Brexit isn’t Lehman, but the stock market is behaving similarly.

In 2008, shareholders made an epic mistake: They assumed Lehman would be manageable. This time the assumption is that central banks will ride to the rescue and corral any problems. Investors expect global easy money, adding yet another central-bank prop to the stockade protecting shares from weak economic growth. The result is some unusual, and worrying, behavior in the bond market.

Since the Brexit vote, Treasury yields have tumbled, and they kept falling even as shares recovered. On Friday, 10-year and 30-year yields set new lows, as did British and Japanese benchmarks. Bondholders think central banks will worry about the economic impact of Brexit, keeping rates lower for longer. This is quite different from what happened after Lehman, when bond yields rebounded with shares, as bond investors made the same mistaken judgment that there would be few long-run effects from a midsize U.S. bank failure.”

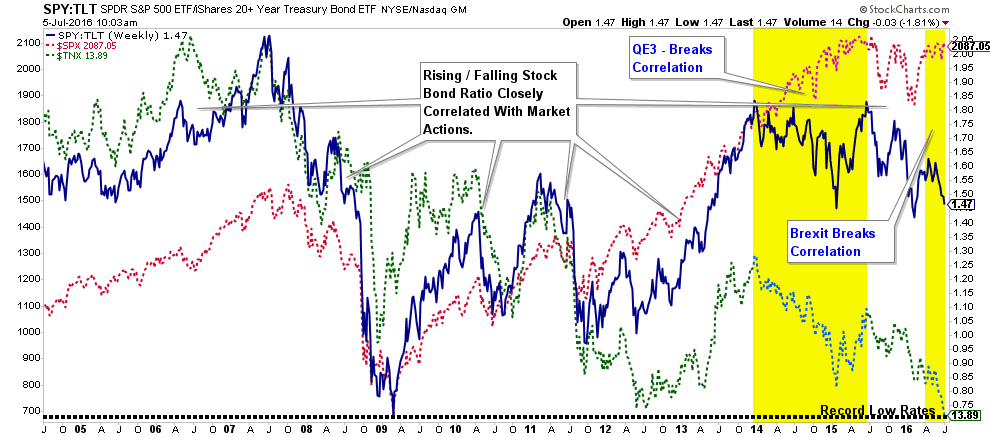

The ratio between stocks and bonds is sending a clear warning.

As shown above, the dark blue solid line is the ratio between stock prices and bond prices. Not surprisingly there is a high level of correlation between this ratio and the rise and fall of stock prices. This is with the exception of just two periods: the run-up of asset prices during QE3 and leading up to and following the “Brexit” vote.

“Last week’s divergence of bonds and equities isn’t healthy. Bond markets are screaming that the world economy is slowing, and shareholders have their fingers in their ears singing ‘la-la-la I can’t hear you.’ Stocks are no longer about growth, but about a desperate search for safe alternatives to low-yielding bonds.”

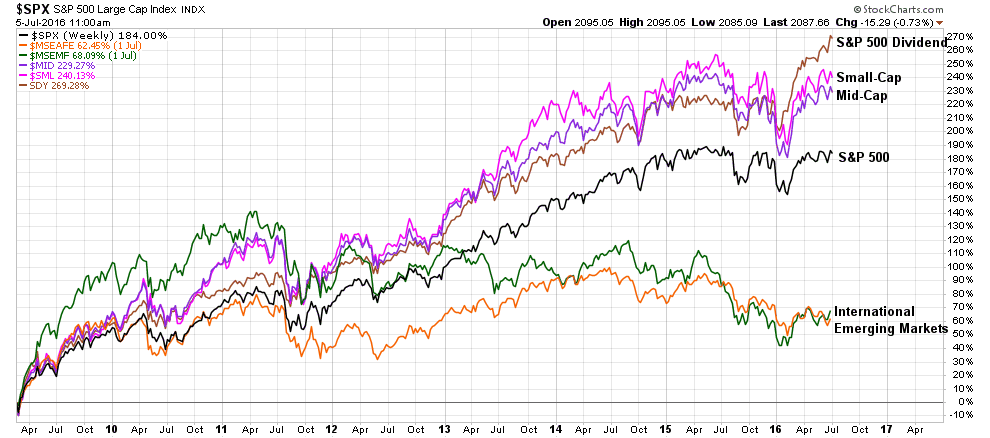

Since Brexit, the drive for bonds has been particularly sharp. However, as James stated, the drive for yield is not just about bonds but also about anything that pays a yield. Utilities, consumer staples, health care and telecommunications have been the leading sectors as they pay the highest dividends.

However, DO NOT be mistaken. This chase for yield is not something new but has been a growing bubble born of Central Bank interventions since the end of the financial crisis. As shown the dividend yielding stocks of the S&P 500 have outperformed every other major asset equity asset class. This should not have happened.

The result has been a push of valuations of mature, dividend-paying, low growth companies to extreme levels. The result will be, not surprisingly, a reprisal of the “Nifty Fifty” crash from the late-70’s. In other words, with the defensive sectors at extreme overbought levels, during the next major-market reversion there will be no “safe place” to hide for investors.

The same goes for bonds and I agree with Doug Kass’ recent commentary:

“I believe that fixed-income markets around the world are in a bubble of monumental proportions — and as is the case with most bubbles, the irrational is being rationalized.

I can say with a high degree of probability that when this whole bond bubble blows up, it will wipe out years of profits for many!”

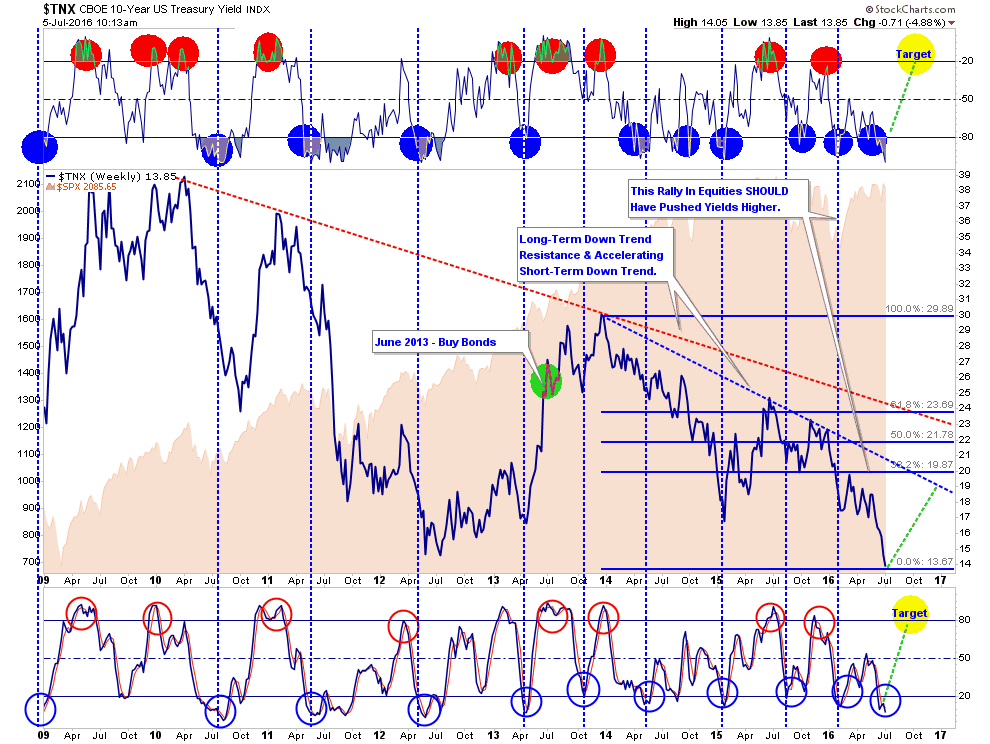

Now, let’s be clear, while I agree with Doug that bonds are extremely overbought currently, it also does not mean rates will go soaring off to the moon either. The chart below shows the current condition and the expected levels of the rebound.

It is unlikely that rates in the U.S. will exceed 3.0% currently. A rapid rise in rates, will lead to a whole variety of bad economic consequences and ultimately a recession from such low levels of current growth. Such a spike in rates will also coincide with a fairly substantial major market reversion unlikely to be contained or controlled by the Fed and the damage will be felt across virtually every asset class in the market.

However, while “Brexit” is the continued focal point of Central Banks globally, the real “risk” for asset markets is never what is “seen” but rather what is “unseen.” That problem can be summed up in just one word: “China.” I agree with Mark St. Cyr on this point.

“All it will take is just one time, or one player to upset this apple cart of illusion which is desperately being maintained, and it all unravels. And as I’ve iterated many times previous I believe that player is China.

As central banks keep intervening mightily within the capital markets as I have stated before: to think China will idly stand by and just ‘suck up’ the consequences of those actions is a fools game. And as proof I would like to point out that as the central banks were busily propping up the markets before, during, and after the Brexit vote. China (once again) devalued the Yuan in a move not seen, and reminiscent in size and scope of August last year. You know, when everything was seeming to come off the rails – once again.”

Of course, it could be something else entirely.

Lance Roberts

Lance Roberts is a Chief Portfolio Strategist/Economist for Clarity Financial. He is also the host of “The Lance Roberts Show” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, and Linked-In