If trade is a reflection of global demand, and if shipping rates are a reflection of the supply of ships by carriers and the demand for those ships by exporters to meet that global demand for goods – well then, we’ve got a situation on our hands.

Two weeks ago, when I wrote about the Shanghai Containerized Freight Index (SCFI), the index had fallen so far so fast that it seemed to be a statistical fluke, something that would instantly bounce back. The SCFI tracks the spot rates from Shanghai to various destinations around the world. At the time, the SCFI component for Northern Europe had plunged 14% from the prior week to $399 per twenty-foot container equivalent unit (TEU), down 67% from a year ago. An all-time low.

There was a lot of handwringing because, even with the lower bunker fuel costs, the break-even rates for these routes were $800 per TEU, according to a report by Drewry Maritime Research. Over twice the spot shipping rates!

The question was how much lower could rates drop?

A lot lower. Over the two weeks since, the SCFI for Northern Europe plunged another 14% to $343, setting a new all-time low. A terrific 68% collapse from the same week a year ago. Something big is going on in the China-Europe trade.

Carriers have tried to impose hefty rate increases, with UASC pushing for an increase of $1,300 per TEU, and a gaggle of others going for an increase of $1,000 per TEU, according to the Journal of Commerce. None of them were able to make them stick.

The swooning rates came as bunker fuel costs have been rising off their January lows. Higher input costs are hitting container carriers just as revenues are collapsing. A toxic mix.

Now the hope is that planned rate increases for June are going to stick….

On some other routes, carriers have succeed in raising rates, and so not all routes from China suffered the same relentlessly brutal fate. Rates ticked up recently to the Mediterranean, South America, and the US West Coast.

But that doesn’t say much. On the routes from Shanghai to the US West Coast, carriers tried to impose rate increases effective April 1. But after rising by nearly $300 to $1,932 per forty-foot container equivalent unit (FEU) in the first week, the spot rate plunged to $1,623 in the second week, and to $1,596 in the third week. In the week just ended, the index jumped to $1,783. It’s still down 8% from early April, and about back where it was a year ago.

Rates lost ground on other routes, such as to Australia/New Zealand and the US East Coast (those rates had been inflated by the labor dispute at West Coast ports that had caused shippers to bypass them). And so the composite SCFI for all routes rose to 761, from 702 which had been the lowest level in years! The index is down 34% from a year ago and far below the multi-year range between 900 and 1,200.

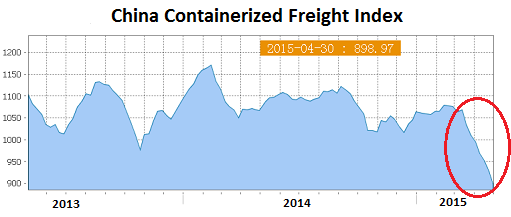

The much broader China Containerized Freight Index (CCFI), which is sponsored by the Chinese Ministry of Communications, paints a similar picture.

While the SCFI tracks spot rates from Shanghai to global markets and can be very volatile, the CCFI tracks spot and contractual rates for all Chinese container ports, is much less jumpy, doesn’t react as quickly to changes in spot rates, and is “more comprehensive and macroeconomic,” as the Shanghai Shipping Exchange, which operates it, explains. It’s considered “the second world freight index” after the Baltic Dry Index.

And it has skidded 16% since mid-February to a multi-year low of 899. This is what the 2-month plunge looks like:

Another index, the Worldwide Container Index for routes from Asia to the Americas and Europe, which Drewry cites, has plummeted 41% since January to below $1,300 per FEU (ugly chart). Clearly, something is going on in the east-west container business – and beyond – to create this sort of gloom.

On top of the list of reasons is weak demand for imports in Europe, particularly the Eurozone, whose currency has been purposefully massacred by the ECB to achieve just that sort of effect: reducing imports and goosing exports as part of the currency war. Imports measured in euros may actually rise, since the same imports are now more expensive. But the number of containers would drop, since the same amount of euros now buys a lot less in China, whose currency is pegged to the dollar.

In the US, there has been a monstrous buildup of business inventories. Inventories tie up cash. Eventually businesses try to bring them back in line by cutting orders. And that comes on top of a really crummy first quarter.

On the Chinese side, the impact has already shown up, however foggy the figures may be. China’s “official” manufacturing PMI, which was released on Friday, came in at 50.1, barely in expansion mode, and the worst reading for an April since 2005. But it captures the state-owned giants that are less engaged in manufacturing for exports.

The HSBC manufacturing PMI, released today, fell to 48.9 in April, solidly in contraction mode, the worst level since April last year. The new-orders sub-index, which points at what the near future might look like, dropped to 48.7. The March PMI had also been in contraction mode. It’s the HSBC PMI that captures the private-sector companies that are heavily export-oriented. These companies are struggling with very lackluster global demand for their products.

In terms of shipping, on the supply side, carriers have been adding new and ever larger ships, now that money is nearly free. Decision makers had been bamboozled into thinking that QE and interest rate repression would stimulate actual demand! And they’d expanded their fleets to meet this illusory demand.

Cheaply borrowed money gets plowed into creating overcapacity: Investors desperately chase yield, and companies become over-optimistic believers in the fallacy that central-bank asset-price inflation can create actual demand for everyday goods needed or wanted by real people. This happened in the global resource sector, in the US oil-and-gas sector, in the global shipping business…. These are among the places where money now goes to die.

There are other places where money goes to die as investors who’d bought into the hype get crushed. Read… Stocks in This Totally Hyped Sector Are Crashing