Now that Kinder Morgan has come out with a massive dividend cut, I think it will get harder to ignore that this isn’t just about crude oil prices and the death of “transitory.” There is a financial element here that is perhaps even more important.

Kinder Morgan Inc., the biggest North American oil pipeline operator, cut its 2016 dividend by 74 percent as the free-fall in crude markets reduced cash flow needed to cover payments on $41 billion of debt.

Kinder Morgan stockholders will receive a payouts totaling 50 cents per share next year, the Houston-based oil and natural gas shipper said Tuesday in a statement. As recently as Nov. 18, the company was promising investors a 6 percent to 10 percent increase from the $2 per share it budgeted for this year, which would have meant payouts of $2.12 to $2.20. [emphasis added]

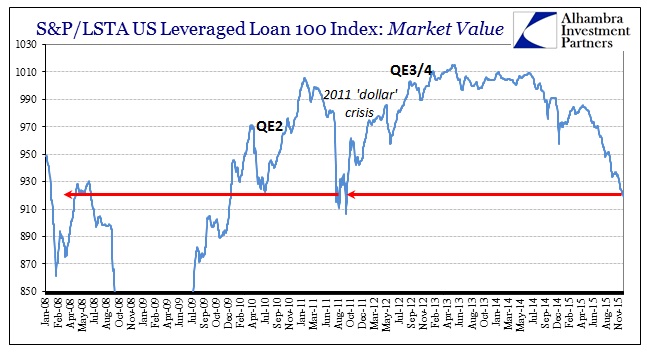

In the space of just three weeks, the company went from expanding its dividend to cutting it by three-quarters? That is far,far more serious than just oil trading below $40 once more. Again, as noted from Anglo American’s earlier statement, you have to believe that the huge and dramatic turmoil in junk right now is playing a role in these decisions. That includes not just 2008-level prices recently, but also much, much more discrimination in trying to float anything (cov-lite of 2014 is as dead as transitory).

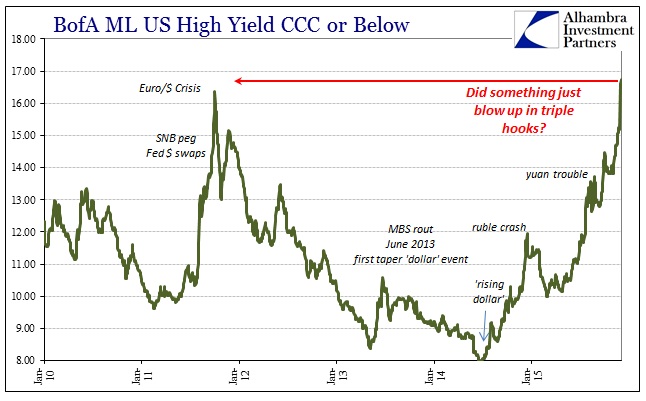

The huge spike in the BofAML High Yield CCC’s last week is proving to be a real event, real trading and possibly a wholesale reset of the whole funding and liquidity environment. “Something” didn’t just blow up in junk, it may have been the whole prior financial paradigm. This has, again, not just financial aftereffects but also deep economic consequences as more and more actual businesses turn toward actively managing a very real combined economic and financial threat, instead of desperately trying to ignore it all as Yellen still demands.

What was theoretical before is becoming active circumstances; the media and economists will spin this as “just oil” or “just commodities”, but they also said that oil prices were “transitory”, beneficial and non-concerning in any way. It will be interesting, and vitally important, to see how long manufacturing and general industrial companies can resist marking these same kinds of adjustments with funding and credit applying as much to them.