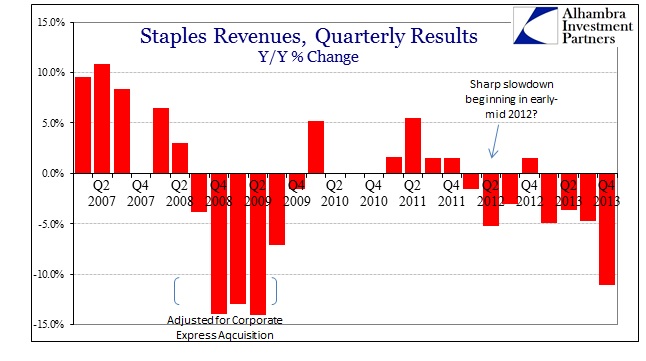

There is undoubtedly a high degree of resistance to the idea that the economy is slowing, or, much worse, has already slowed considerably. For the most part, counter explanations (more narratives than evidence) revolve around the silly to absurd – snow, cold, government shutdown, etc. Office retailer Staples’ latest announcement of a sales disaster, however, actually creates a worthwhile discussion about at least part of the retail segment.

The company just reported revenues that look like something from 2009 rather than 2013; total revenue fell more than 11% in the holiday shopping period. The company does offer at least one somewhat compelling explanation for those results – online competition. That is certainly a valid reason to close 225 “bricks and mortar” stores in an effort to bring the company’s cost structure more in-line with retailing reality as it evolves.

I have no doubt that the virtual shopping trend is a primary factor here, but I question whether it is the sole factor to the obvious exclusion of the macro economy. In fairness to Staples, the company acknowledges both, alluding to the macro theme by including talk of the “tough environment.” It is clear, however, that mainstream analysis is almost exclusive in its focus on Staples’ underperformance as idiosyncratic, again, as doing otherwise would violate the overarching economic theme.

That is somewhat odd to begin with since the company derives half of its sales from its own online shopping portal. It’s not as if the company is solely focused on physical retailing, it already has established a major footprint in exactly where the industry is most changing. And its online results were very much encouraging last quarter. Where same store comps fell 7%, total online sales at staples.com grew 10% Y/Y. Those results would certainly support the impulse to close physical locations, but I don’t find it particularly convincing as a primary factor to the exclusion of worsening consumerism.

When you look at the timing of Staples increasing difficulties, the virtual competition account loses its potency. While the company has clearly struggled since the Great Recession officially ended, the timing of its most recent revenue tension is something that we have seen repeated over and over in a broad section of data (both anecdotal and empirical). The retailer’s misfortunes began to stand out in the first half of 2012.

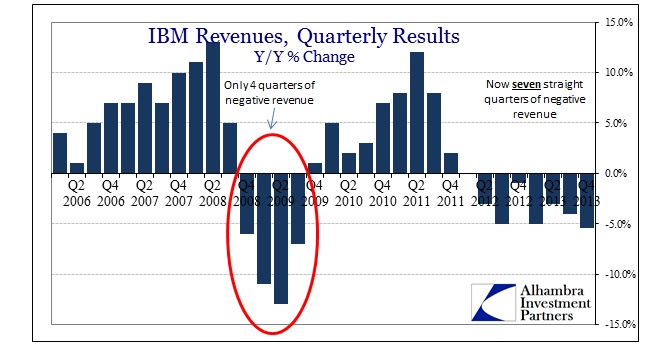

What is even more compelling is that the revenue pattern of Staples is very similar in trends (if not degrees) to a broad array of companies, including those in seemingly unrelated businesses like IBM.

The intriguing resemblance between IBM and Staples runs through their basic business segment – they are both largely related to business spending, including a large proportion on technology investments. I think it would be impossible to conclude that the Staples online competition explanation would also apply to IBM.

It is difficult to ignore, at least on a rational, unbiased basis, these commonalities, indeed as we see them replicated throughout the macro economy. We can assign individual causation to the degrees in which each company or segment experiences that overall trend, but that larger economic dynamic holds far more explanatory appeal and potential – the 2012 slowdown is ubiquitous, extending well beyond even corporate spending.

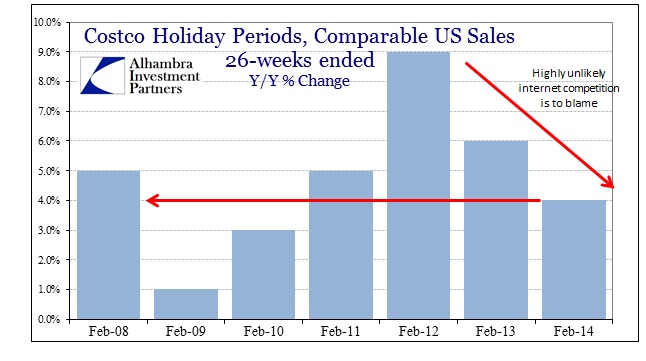

To add one final point of emphasis, bulk retailers such as Sam’s Club and Costco have been one of the few bright spots in the retailing industry. Yet, Costco has seen very much the same pattern as those above, only without the online competition.

The tendency to believe that stronger growth is coming soon correlates very highly with this desire for alternate explanations. At least in viewing Staples’ difficulties there is a plausible secondary scenario that holds actual logical consistency. However, I think a full examination, as I have done here, still points to the overriding macro dynamic.

Click here to sign up for our free weekly e-newsletter.

“Wealth preservation and accumulation through thoughtful investing.”

For information on Alhambra Investment Partners’ money management services and global portfolio approach to capital preservation, contact us at: jhudak@alhambrapartners.com