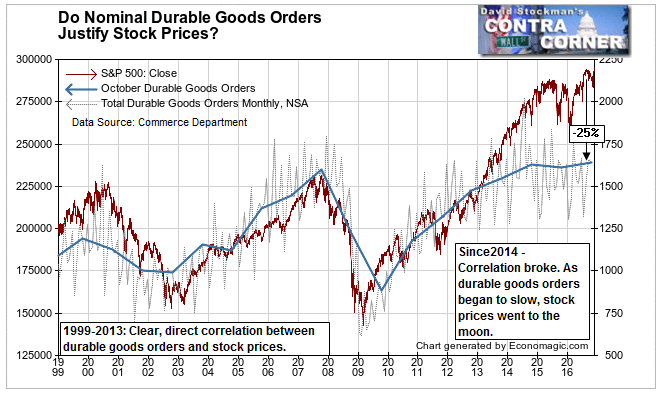

Stock prices started to decouple from durable goods orders in 2013 (see previous post). That broke a direct correlation that had existed since 1999. In 2014-2016, durable goods orders went flat, and stock prices went to the moon.

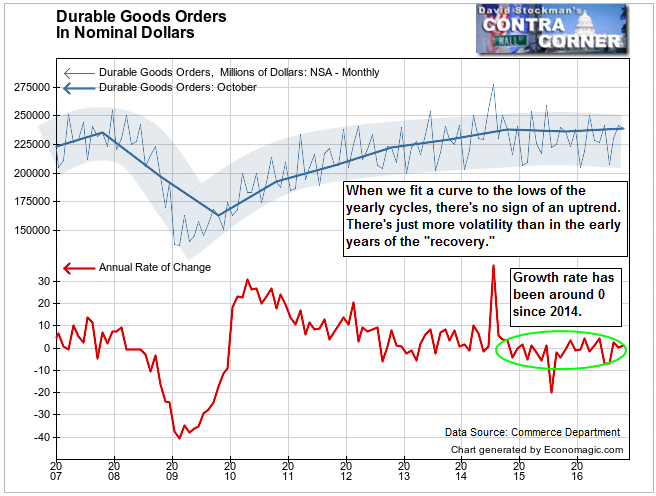

Nominal durable goods orders have been flat for 2 years. Wall Street pundits have called that a “stabilization” in US factories orders. Right. Stabilization at zero.

Nominal durable goods orders include inflation. We saw that after adjusting for inflation the unit volume of orders (real durable goods orders), has been declining since 1999. In 2007, just after the housing bubble peaked, real durable goods orders peaked below the level of the 1999 peak. They then peaked again in 2014 below the level of 2007. As Wall Street pundits were crowing that the US manufacturing sector had stabilized, real orders have actually been slightly declining since 2014.

This hasn’t mattered to the stock market as prices launched into the stratosphere. The fact that the US doesn’t make or buy much in the way of durable manufactured goods has made no difference. Stock prices have bubbled higher because central banks printed trillions (called Quantitative Easing or QE) and pushed the money into the financial markets.

The theory was that the QE cash would flow into the stock and bond markets. Mortgage rates would fall and stock prices would go up. As a result everybody would be happy and spend money, and businesses would invest and grow. The first part worked. Stocks rose and mortgage rates fell.

But everybody wasn’t happy. Corporate CEOs speculated in their own stocks, rather than investing in plant and equipment. They continued to ship good paying jobs overseas, leaving workers to fend for itself. Most of the new jobs for unskilled labor were in low paid service jobs.

So most Americans found their standard of living declining. That led to economic conditions which benefitted only those at the top of the skill spectrum, which begat President Donald Trump. But QE did not help US manufacturing to recover in spite of claims to the contrary.

Meanwhile stock prices rose on “vapors.” Investors who rode the wave have done well, but the risks are growing. A deeper look at the durable goods data illustrates just how disconnected and dangerous this cycle has become.

Total Durable Goods orders includes both aircraft and government orders for military equipment. Both of these numbers are extremely volatile. The military equipment sector is driven by non-economic factors. It’s possible to exclude the orders in these two sectors to get a clearer picture of how the US economy is doing without these extreme non-economic influences.

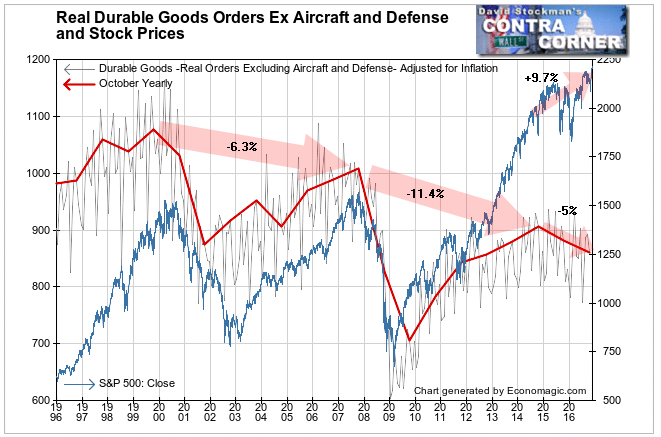

We make the added adjustment of accounting for inflation. The result is a measure of the volume of consumer and business capital goods demand and production in the US. It’s clear that we stopped partying like it’s 1999 in 1999. This measure has been sinking since then. The decline has even accelerated since 2007.

Theoretically this trend should be mimicked in stock prices. Prior to the housing bubble top, this was typical. But something changed after the 2007-2009 crash leading to core durable goods failing to follow the stock market higher.

Over the past year, as the stock market has eked out new highs, these “core” durable goods orders have fallen by 2.4% in real terms. That’s a downward acceleration from a decline of 1.4% in September, and a gain of 2.3% in August.

In other words, in August the year to year trend was positive. It turned down in September and it got worse in October. It’s the weakest October since 2010. The current cycle has been heading down since 2014, with a loss of 5% in the past 2 years. Somehow the stock market managed to rise by 9.7% over the same time frame.

From peak to peak in the cycle from 1999 to 2007, orders fell by 6.3%. Between the 2007 and 2014 peaks, they fell by 11.4%. In the past 2 years they have begun falling again in spite of supposed economic “growth.”

In 2007 both the stock market and durable goods buyers were late in coming to the realization that the party had ended. The peak of orders came a year after housing prices had peaked, and almost 2 years after housing sales volume peaked. There was plenty of warning that the housing bubble had gone bust by the time stock prices peaked.

In the 1999 cycle the durable goods peak was approximately concurrent with the stock market high. The stock market may or may not lead the economic data. Today, there has been a two year divergence between rising stock prices and falling durable goods orders. This must be taken seriously as a warning that the gains in stocks must come back to earth.

Is this possibly a false alarm? Not likely.

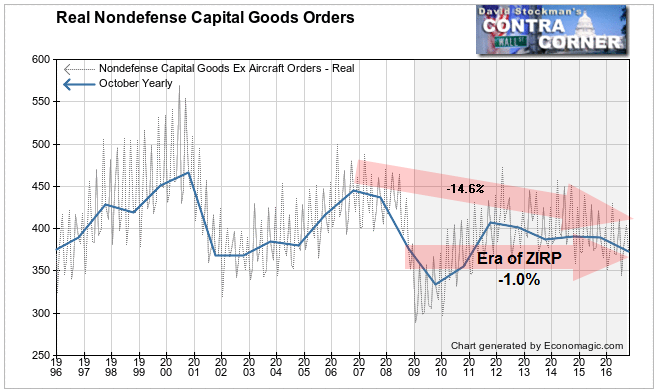

Durable goods orders can be further distilled to just nonmilitary capital goods spending. This is a measure of both business investment and business confidence in the future.

The 2007 housing bubble peak was lower than the internet bubble peak of 2000. So business wasn’t as bullish in 2007 at the top of the housing bubble as it was when the internet bubble began to deflate 7 years earlier.

But look what has happened since the 2007 downturn of the housing bubble. Business capital spending has fallen by 14.6%. In the current cycle, that spending peaked in 2012! Since then business spending on capital goods has fallen. During the era of near zero interest rates, business spending has actually fallen by 1%!

Where’s the stimulus? In stock and bond prices. What happens now that stimulus has ended? The clock is ticking toward the onset of a big adjustment. Stock prices will come back to earth, just as they have in all previous cycles when the Fed ended a period of easy money.

This may surprise you, but in past cycles, business spending rose in tandem with interest rates. Business confidence grew along with rising rates. That continued until rates reached a choke point where investment was no longer seen as likely to be profitable.

Perhaps had the Fed allowed a normal rise in rates in this cycle business confidence would have grown. Corporate CEOs might have invested in their businesses instead of mindless financial engineering schemes to boost their own stock prices.

Now, ZIRP has failed to stimulate real investment in 4 years. No one knows whether the expectation of rising rates will spur more investment. We’re probably destined to find out within the next year. It seems unlikely with economic growth as slow as it is and end user demand as weak as it is.

Normally capital investment takes a period of planning before the spending begins. Over the past 7 years CEOs have become conditioned to undertake to raise their stock prices via Fed sponsored financial engineering gambits. They’re not accustomed to planning capital projects.

Nor does end user demand require or encourage it. Retail sales are barely growing at all in real terms.

One thing we do know is that stock prices and capital spending have grown increasingly out of whack. There will be an adjustment.

This isn’t the first time stock prices have risen beyond reasonable valuations. Stock prices have gotten too high in past long term bubble cycles. They did so in the 1920s, again in the 1960s, then again in the 1990s, and the 2000s. This isn’t a new thing.

But they have never stuck around at “permanently high plateaus,” waiting for the real economy to catch up. Instead the adjustment has come by a major decline in stock prices. We know it’s out there. Buying the market today is an increasing dangerous game. Cashing in and preserving capital, just seems right in today’s frothy environment.

I deal with the questions of timing your purchases and sales in my weekly technical market updates. Try them risk free for 90 days. Fine tune your timing!