[David Stockman’s Note: Last night, I wrapped up my first-ever live video event. Over 30,000 people signed up in total. I hope you were able to attend because during the event I revealed information and access to a once in a lifetime investment that will rock markets… but offer you an opportunity at 300% gains in the coming weeks. If you weren’t able to attend, we’re leaving the full recording plus the urgent access I offered to attendees only until midnight tonight. Please watch the briefing at the soonest chance, and prepare while you still can. After midnight tonight, the video goes dark. So make sure you find the time this evening to watch it. It’ll prepare you for a major market event that could unfold any day now. >>Click here now before you lose the advantage of everything David covered<< ]

By Tyler Durden at ZeroHedge

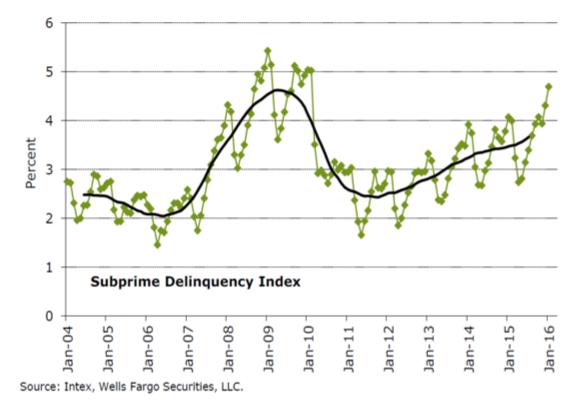

Do not show this chart to Melinda Zabritski:

For those unfamiliar, Melinda is Experian’s senior director of automotive finance and she’s never, ever worried. Or at least not that she lets on.

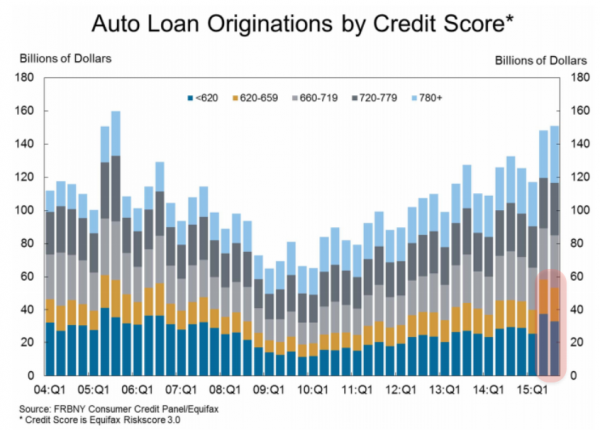

“We’re not seeing anything that would be a red flag,” she said earlier this month in response to data that showed the percentage of auto loans made to buyers with the poorest credit ratings is growing faster than the rest of the auto finance market. As a reminder, here’s the chart that shows the trend:

What the first chart shown above (from Wells Fargo) shows is that delinquencies on the subprime car loans that have found their way into the $125 billion annual market for auto loan-backed ABS have risen to their highest level since 2010.

As we’ve gone out of our way to document, underwriting standards for car loans are getting looser as lenders scramble to feed Wall Street’s securitization machine and keep America’s auto sales “miracle” alive. Of course the pool of creditworthy borrowers is finite and so it must be continually expanded by lending to those whose FICO scores and income might not otherwise warrant the extension of a loan.

Indeed Experian itself will tell you that the market is getting more extended all the time, with average payments rising right alongside loan terms. Some of the loans now being pooled, chopped, packaged and sold to investors were made to borrowers with no credit score at all (thank you Skopos Financial).

And while Citi isn’t ready to ring the alarm bells just yet (see here), Wells Fargo apparently is.

“Rising delinquencies are a warning sign that more loans may end up in default down the road,” Bloomberg reports, citing Wells analyst John McElravey. “What may be most troubling, however, is that the default rate is already climbing, up to 12.3 percent in January from 11.3 the month prior. That is also the highest since 2010, the data show.”

McElravey goes on to suggest that because delinquencies seem to be rising in areas that are hard hit by the slump in crude, we could be on the precipice of a rather precipitous increase in defaults. After all, the consequences for Main Street of the prolonged downturn in crude and other commodities are just beginning to show (see here). As are the effects of the slowdown in global growth and trade (see the recent layoffs at Daimler in North Carolina). As McElravey puts it, “the data on subprime auto is worth watching closely, especially against the backdrop of subpar economic growth.”

But before you go thinking you’re Michael Burry and suprime auto is your overheated 2007 housing market, remember, Citi’s Mary Kane says you shouldn’t watch too many movies: “It seems like too many people have seen the movie ‘The Big Short’ and are starting to think the movie heroes’ short strategy would translate to the ABS market. By the way, the ABS conference did NOT take place at Caesar’s Palace that year as per the film, it was at The Venetian. So, it’s not wise to believe everything you see in a movie and hit films are not the best source for trade ideas,” she wrote late last month.

Who you gonna believe, Mary and Melinda or your lyin’ ..er.. Wells?