By John W. Miller at The Wall Street Journal

CERRO VERDE, Peru—In this volcanic desert, a dusty moonscape patrolled by bats, snakes and guanacos, America’s biggest miner is piling on to the new force in industrial resources: supermines. It’s a strategy that could be driving miners into the ground.

Freeport-McMoRan Inc. is completing a yearslong $4.6 billion expansion that will triple production at its Cerro Verde copper mine, turning a once-tiny, unprofitable state mine into one of the world’s top five copper producers.

As Cerro Verde’s towering concrete concentrators grind out copper to be made into pipes and wires in Asia, it will add to production coming from newly built giant mines around the world, in a wave of supply that is compounding the woes of the depressed mining sector.

Slowing growth in China and other emerging markets has dragged metals prices into a deep downturn, just a few years after mining companies and their investors bet billions on a so-called supercycle, the seemingly never-ending growth in demand for commodities.

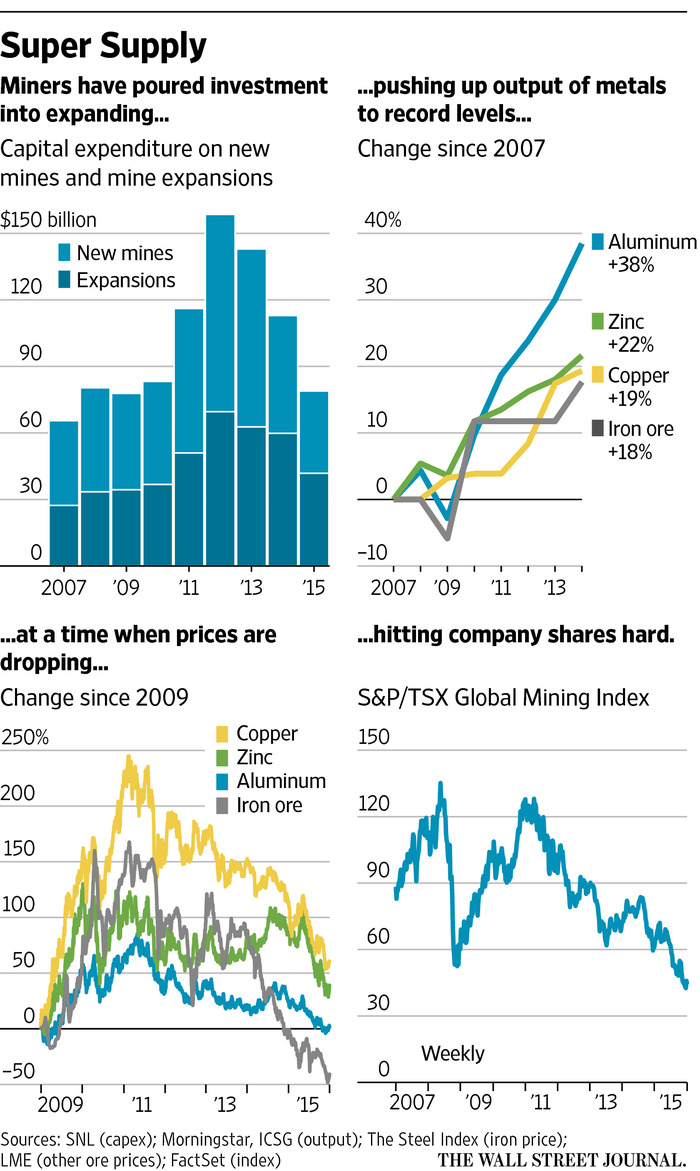

Back then, miners awash in cheap money set out to build the biggest mines in history, extracting iron ore in Australia, Brazil and West Africa, and copper from Chile, Peru, Indonesia, Arizona, Mongolia and the Democratic Republic of Congo. They also expanded production of minerals such as zinc, nickel and bauxite, which is mined to make aluminum.

Those giant mines are now giving the industry an extra-bad hangover during the bust. The big mines cost so much to build and extract minerals so efficiently that mothballing them is unthinkable—running them generates cash to pay down debts, and huge mines are expensive to simply maintain while idle. But as a result, their scale means they are helping miners dig themselves even deeper into the price trough by adding to a glut.

The prolonged price slump has forced miners to make painful cuts. In December, Anglo American PLC, which recently completed a supermine in Brazil that went over budget by $6 billion, announced 85,000 new job cuts, asset sales and a suspended dividend.

On the same day, Rio Tinto PLC, which has built supermines in Western Australia, cut spending plans, while in September, GlencorePLC suspended its dividend and raised $2.5 billion in stock as part of a plan to cut debt.

Phoenix-based Freeport itself has felt the pressure. Executive Chairman and co-founder James R. Moffett stepped down on Dec. 28, months after activist investor Carl Icahn took a large stake. The board approached the wildcatter, who is known as “Jim Bob,” about resigning, after nearly half a century with Freeport and its predecessors.

When Freeport’s Cerro Verde mine’s production is fully ramped up this year, it will hit a billion pounds of copper a year—3% of the world’s production, even as copper prices sink to six-year lows.

The impact of mines like Cerro Verde is sweeping, including downward pressure on commodity prices until the end of the decade, when supply is expected to slip as some older mines finally dry up. Companies’ profit margins are shrinking, many are writing down assets and more smaller players are likely to go belly-up, according to ratings firms and analysts.

Investors who once bet on ever-increasing demand by backing miners have also been badly burned as share prices have dropped and dividends have been gutted. The benchmark S&P/TSX Global Mining Index has fallen 65% since 2010.

Since 2007, mining companies have spent over $100 billion a year in capital expenditure, much of it to build supermines, such as Rio Tinto and BHP Billiton PLC’s expansions in the Pilbara region of Western Australia, which require thousands of workers to fly in for stints in a remote desert, and Anglo American’s Minas Rio in Brazil, which involved a 325-mile iron ore slurry pipeline snaking its way though 32 municipalities.

Investment is still trickling in. Rio Tinto in December announced a $4.4 billion financing deal for its Oyu Tolgoi copper and gold supermine in Mongolia.

“After nearly three decades of having to beg for capital, suddenly bankers and investors were throwing money at miners and imploring them to invest in more and bigger projects,” said Dick Evans, a former board member of Rio Tinto, and now chairman of aluminum maker Constellium NV. “The miners were like kids in a candy store.”

At the same time, new mining technologies, like bigger haul trucks, shovels and other equipment, enabled the building of facilities that could produce two or three times the copper or iron ore of the previous generation of big mines.

Spread over 150,000 acres, Cerro Verde includes two pits that each could fit multiple baseball stadiums; a $500 million water treatment plant half a mile long; and two hulking concrete and steel concentrators that look like giant roller coasters and can extract copper from 360,000 tons of rock a day. The mine is capable of consuming around 9% of all the electricity in Peru. A tour took six hours.

Cerro Verde is so big that “we’re running into the limit of space and how many trucks you can put on ramps,” said Red Conger, the chief operating officer responsible for the mine, on a recent mine visit.

Even before miners started building these giant mines, low interest rates helped spur a wave of mergers in the industry, which had long been fragmented with thousands of small and midsize firms. Global players including Rio Tinto, BHP, Glencore and Anglo American bulked up, and Freeport paid $25.9 billion for Phelps Dodge in 2007. “We bought a company 2.5 times our size, and that was made possible only by cheap financing,” Freeport CEO Richard Adkerson said in an interview in November.

Freeport had only one mine, but it was massive: the Grasberg copper and gold mine in Indonesia, developed by Mr. Moffett, a colorful Southerner known for his Elvis impersonations and his ability to forge political connections in remote places.

Among Phelps Dodge’s 11 copper mining properties was Cerro Verde, located amid dormant volcanoes 20 miles southwest of Arequipa, a picturesque Spanish colonial town dubbed the White City for the color of its stone buildings.

Peru’s mineral wealth has been known to foreign investors since the Spanish conquistadors invaded in the 16th century. Gold and silver were the big prizes until miners from the newly industrializing U.S. arrived early last century with a new target: copper.

Discovered in the 19th century, the Cerro Verde deposit was considered so inconsequential it wasn’t even mined industrially until the 1970s. Then it became “a small mine that had been badly managed by the Peruvian state,” said Carlos Galvez, chief financial officer of Cia de Minas Buenaventura SAA, which has had a minority stake in the mine since the 1990s. The site, which receives only 1.5 inches of rain a year, had insufficient power and water.

Mr. Adkerson and his team, bullish copper advocates, believed Cerro Verde could be much bigger. “We determined from the outset that Phelps Dodge had not been aggressive enough in drilling” to evaluate the possibility of an expansion,” said Mr. Adkerson. “And the benefit of the merger was that we could use the [profits of the] Grasberg mine to support” Cerro Verde and other expansion projects.

Freeport’s drillers concluded Cerro Verde had twice as much copper available as originally estimated, and in 2008, just over a year after the Phelps Dodge deal closed and with copper at $3.94 a pound, Freeport started work on an expansion.

But then the financial crisis hit, pummeling demand for metals used in construction, and Freeport shelved the project in March 2009. The price of copper had fallen to $1.40 a pound, below the expected cost of extraction, guaranteeing that a bigger Cerro Verde would lose money.

Copper prices began to rise as Asian economies led a global recovery in 2009, and demand from China soared for iron ore and copper, the two minerals needed in huge quantities for industrialization. By March 2010, Freeport rebooted the Cerro Verde project. The company also undertook expansion projects elsewhere in Peru, and in Arizona and Congo.

It took three years for Freeport to secure permits and to develop an engineering plan that harnessed the new technologies and secured the water needed to mine on such a massive scale.

Mining companies consider Peru one of the most difficult countries to navigate as a foreign investor. The country has a long history of anti-mining activism, dating back to fighting the pillaging Spaniards in the 16th century.

To obtain permits, Freeport built a $500 million wastewater treatment plant that serves the mine. Separately, it also designed and paid for a $125 million plant that cleans water from a local river for Arequipa.

Majura Chua, 43, runs a small shop selling toilet paper, candy and soft drinks down the road from one of the new water plants. This October, she was hooked up to a pipe. “We can take showers now,” she said. Before that, she had to pour buckets into a reservoir on top of the house.

The company also lobbied local residents and key officials, including the local archbishop. People in one shantytown recall that in 2010 Freeport sent them Christmas presents: soccer balls for boys and Barbies for girls.

Freeport said it has a tradition of sending Christmas gifts to the children of the area, and that it also sponsors educational programs.

Construction didn’t start until March 2013. But copper was already in another downturn, falling from a peak of $4.48 a pound in February of 2011 as China slowed and new supply came online.

The scale and complexity of the project slowed the work. The area, still scattered with volcanic ash from eruptions centuries old, was so mountainous, “we needed 10 and a half months just to create the flat space to build,” said Mr. Conger, the chief operating officer. Cerro Verde is in an earthquake zone, and everything had to be designed to withstand a 9.5 Richter quake.

A project of this enormousness wouldn’t have been possible years ago, and might not have been cost effective, even at healthy metals prices, according to Mr. Evans, the former Rio Tinto board member. “Now there are bigger trucks, faster drills and computer controlled processing equipment which can support larger scale mines,” he said.

Cerro Verde’s copper grades are only 0.37% of the rock, half the rate at comparable mines. Freeport built a much bigger and stronger concentrator to crush and filter the rock before mixing it with chemicals to extract the copper.

Crushing happens in giant drums equipped with tungsten carbide studs. But the rock was so hard the studs were wearing out and needed to be replaced every three months, at a cost every time of $1 million. Engineers changed the length of the studs and the composition of their alloys, which meant they needed to be replaced only every 12 months.

Hauling rock around accounts for half of Cerro Verde’s mining costs, so it bought and programmed trucks and software to run a relatively small number of trucks more frequently.

Monitoring software quickly spots problems in trucks and shovels, allowing them to be repaired before they have to be replaced, saving money.

The mine’s huge scale keeps its operating costs down, at under $1.50 per pound. That means even with copper prices now just above $2 a pound, a six-year low, it will continue to make money on an operational basis.

It is one of Freeport’s least costly mines to run, so “you’d have to close a lot of mines before this one gets shut down,” said mine president Bruce Clements.

But the production of giant mines will help keep metals prices low “because it will help to keep output high,” said analyst Dan Rohr of Morningstar Inc.

After 15 consecutive profitable quarters, Freeport has lost money in the past three. The company is also loaded down with $20.7 billion in debt, much of it accumulated during its 2013 acquisitions of energy companies McMoRan Exploration Co. and Plains Exploration & Production Co. in deals valued at $19 billion.

In 2014, to help pay for the Cerro Verde expansion, Cerro Verde obtained a five-year $1.8 billion loan with a group of banks including The Bank of Tokyo-Mitsubishi UFJ Ltd., BNP Paribas SA and Citigroup Global Markets Inc. The banks agreed to the loan because of Cerro Verde’s low costs and its guaranteed production life of at least 30 years, according to a person familiar with the deal.

Mr. Adkerson said the company “financed Cerro Verde principally with cash flows” in addition to that line of credit. Freeport’s “copper expansions are not driven by debt,” he said.

But Freeport’s quarterly losses and debt load have put pressure on management. In August, the company said it would slash its 2016 capital spending by 29%, cut about 10% of its U.S. workforce—more than 1,500 jobs—and lower production.

The day Freeport made that announcement, Mr. Icahn, the activist investor, let Mr. Adkerson know he had bought an 8.5% stake in the company, worth roughly $900 million at the time, making him one of the company’s biggest shareholders.

In October, Freeport said it would cut the size of its board and focus on its copper business, and explore all options for its energy business, including a spinoff or sale of a stake.

“We’re in a tough marketplace, we have too much debt, we have to come up with business strategies about how to manage our balance sheet in a difficult environment,” said Mr. Adkerson.

But he added he believed the supply of copper would dwindle in the future. “You need large-scale mining and large-scale processing to be competitive,” he said. “And that’s what we have in Cerro Verde.”

Source: Supermines Add to Supply Glut of Metals – The Wall Street Journal