LAID OFF, RETIRED OR ABOUT TO BE – Then this event is for specifically for you.

Click the link below for full details.

Brought to you by KSEV RADIO am700 & The Lance Roberts Show

BEAR MARKET HAS STARTED

The action this past week has been, to say the least, dismal. However, the major lows that have been support for the bull market since 2009 continue to hold for now, but are under attack. We continue to watch these lows closely as a failure would likely accelerate selling.

This week, I am going to take a look at major sectors, asset classes, and markets to analyze the risk/reward of having money invested in any specific area. In every bear market, there are always opportunities, we just have to find them.

However, before I get into that, let me discuss why I believe we have currently entered into a bear market cycle. Last week, my friend Joe Calhoun at Alhambra Partners wrote a brilliant piece discussing what a bear market actually is:

“The definition of a correction as down 10% and a bear market as down 20% though are just arbitrary numbers agreed upon by no one and everyone. And those thresholds, despite recent history, are met quite frequently. 10% corrections come around every couple of years and most of them are over before most investors get a statement that might scare them into doing something stupid. 20% bear markets are also pretty routine, coming along roughly 1 year out of 4. Corrections and bear markets are generally over pretty quickly, even the ones that turn into financial crises. The 2008 bear market, from peak to trough, lasted 17 months; it only felt like a lifetime.

The real enemy of investors is not these fairly routine 10 or 20% downturns. The real enemy is the bear market that is associated with a recession or crisis, the one that knocks your equity block down by 40 or 50%. And actually, it isn’t even the depth that is the real enemy. For most investors the enemy is time. Whether you are a younger investor still accumulating assets or a pre-retiree about to depend on your nest egg for income or a retiree already doing so, bear markets eat up your most precious commodity – time. Recovering from large drawdowns when you are young is obviously easier – if you stick to a plan and don’t get laid off in the recession that caused it. But if you are about to retire, a bear market may mean you have to keep working for a few more years, putting a little tarnish on your golden years. If you are already retired it may mean something even more devastating – running out of money before you run out of years.

So, is this already a bear market? If we are measuring it for the S&P 500 in terms of price the answer is no. But in terms of time? I think, for a lot of people, we’re already there.

In short, the trend has changed, the inflection point between trending higher and trending lower is long gone. If you’re still looking for it, I’m sorry to be the one to tell you but you missed it.”

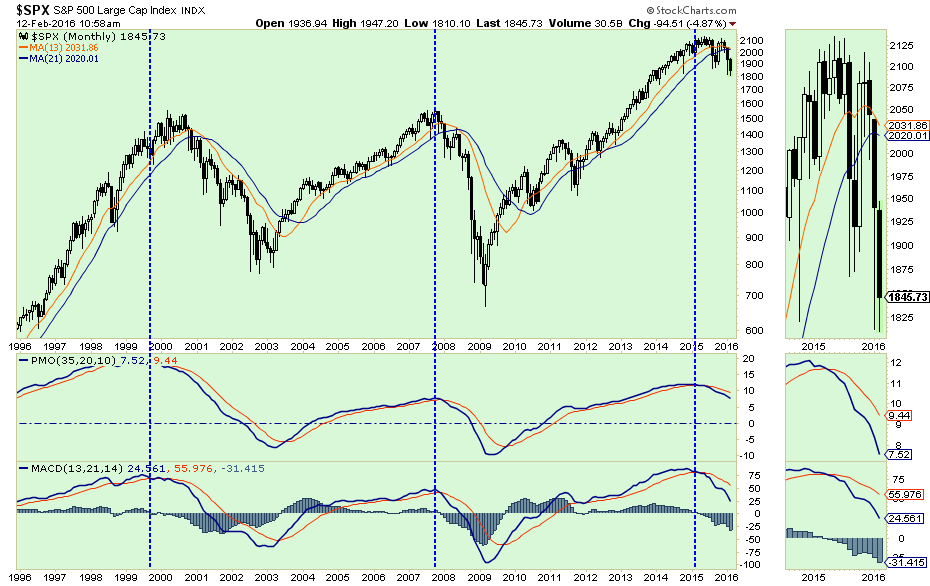

The chart below shows what Joe is talking about:

Notice that prior to both previous bull market peaks, price momentum turned from positive to negative. Likewise, at almost the exact peak, as NOW, the 13-Month moving average changed from a positive to a negative slope.

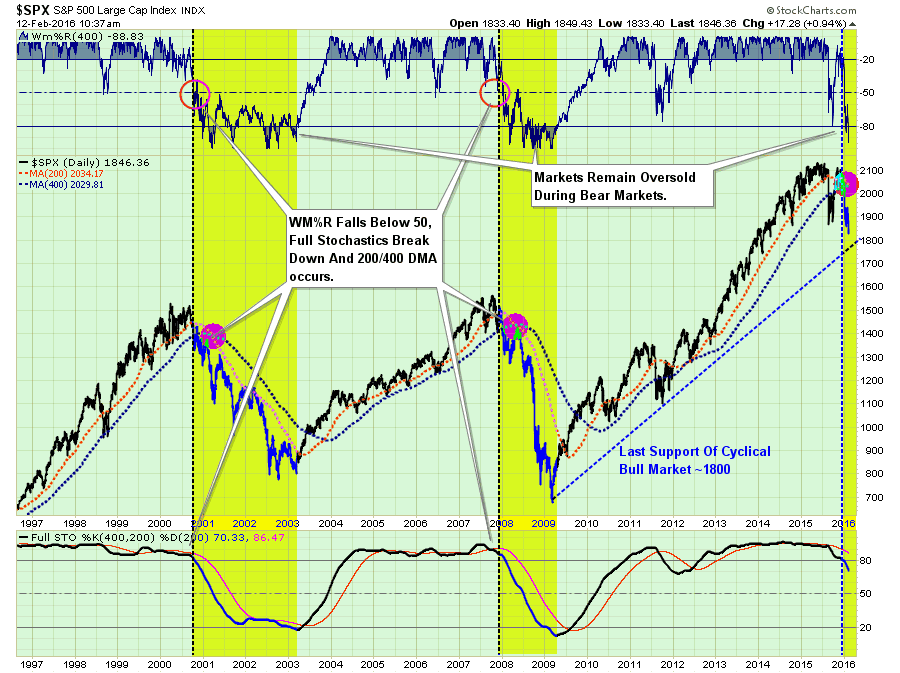

Let’s step back and take a look at the longer-term development and we can see the same behavior. The chart below is the 200-400 day moving average crossover I have discussed previously.

Importantly, as I have annotated, at the peak of the previous two bull markets, both the long-term Wm%R and Full Stochastics registered a trend change which was ultimately confirmed by the 200-dma crossing below the 400-dma. You were given plenty of warning to exit the markets BEFORE losing 20% of your money to validate the onset of a bear market.

(Notice that during the correction in 2012, the registered sell signals of the Wm%R and Full Stochastics were never confirmed by a 200-400 dma crossover.)

Currently, both primary sell signals are in place and with only a 5-point spread between the 200 and 400 dma, the confirmation of a bear market will be registered in the days ahead UNLESS there is a rapid rise towards old all-time highs. Given the current fundamental, technical and economic backdrop there is little reason to expect such a sharp rise to occur.

63% CHANCE OF LOSS IN 2016

However, let me add a bit of statistical analysis to the discussion from my new friend Salil Mehta from the Statistical Ideas blog:

“A good chunk of Wall Street strategists have yet again quickly changed their minds on their 8% 2016 forecasts (markets are instead DOWN 8%.) Now that’s a 12-month commitment!

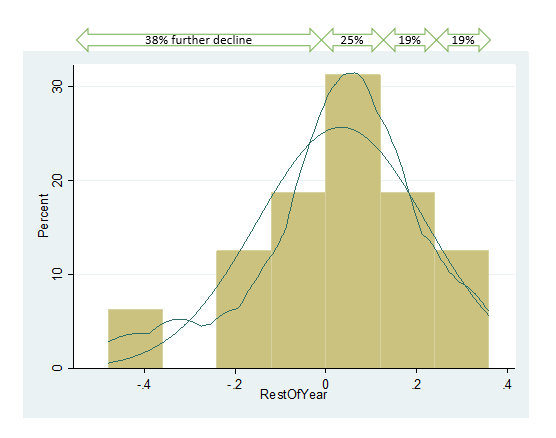

The 16% gap (8% fantasy minus -8% reality) predicts nothing about the future, and anyway, the gap is in the middle of the recent pack! So let’s explore all of the 10.5-month returns (from mid-February through December), from year 2000 onwards. The evidence shows that there is an awesome 63% chance for a negative 2016 (as illustrated below, 38 percentage points of which are due to additional negative returns from here).

But what on earth could these cunning “strategists” possibly say now that would be of interest? Nothing intelligent: the same inaccurate story for >20 years, which is a twice as high, 8% annualized from these depressed values. Equally sad, NONE are guessing that markets will go down further.”

As he concludes:

“Get used to more of this. It’s like a fortune cookie that never changes.”

He is absolutely right. As I have addressed so many times in the past, whenever you hear the words “we like this long-term,” “long-term returns,” or “over X-period the average rate of return has been…” – RUN!

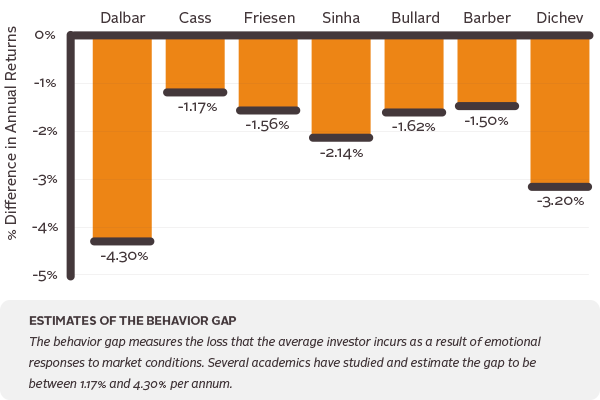

Investing for the “long-term” is a very nice premise on the surface. The problem is that psychology and genetically, you can not invest that way. You are ultimately ruled by the 4-F’s: Feed, Flee, Fight, and Have Sex. When markets crash enough. most individuals don’t kick back and have a burger. They are generally either looking to sell or punch someone. You may think you can ride the waves of the market…but you can’t. Repeated studies all show the same outcome in the end. As noted by Meb Faber last week:

The reason for this under performance, despite the best of intentions to be a long-term investor, was best summed up by Mike Tyson:

“Everyone has a plan until they get punched in the face.”

You may believe you can weather the ups and downs in the market, but when you lose 30, 40 or 50% of your money, plans change.

REDUCING RISK, LOOKING FOR OPPORTUNITY

This is a potentially confusing point for investors. How could we be reducing risk on one-hand but looking for opportunity on the other? Good question. Let me explain.

Investors always make some fairly common mistakes in their portfolio management:

- They buy something without a target to sell (target gain or stop loss).

- They assume if they sell something they can never buy it again.

- If they sell something at a loss, it is now forbidden fruit.

- If they sell something at a gain, and it goes higher, they jump back in.

- By not selling a loser they don’t have to admit they were wrong.

- By not taking gains in winners, it confirms their “genius,” until it reverses to a loss.

- Etc., so forth, and so on.

These are all emotionally driven responses. Most bad habits of investors, individuals and professionals, revolve around their “ego.” This is particularly the case of professionals who ostensibly believe they are “smarter they the average bear.”

As a portfolio manager my job is actually very simple: Avoid major draw downs.

By doing just this one thing you can literally outperform the market over the long-term.

- NO…you will not beat the market from one year to the next which is a stupid goal anyway.

- NO…you will not sell at the peaks and buy at the bottoms.

- NO…you will not have regular appearances on CNBC.

- YES…you will achieve your long-term goals.

With this in mind, last week I stated:

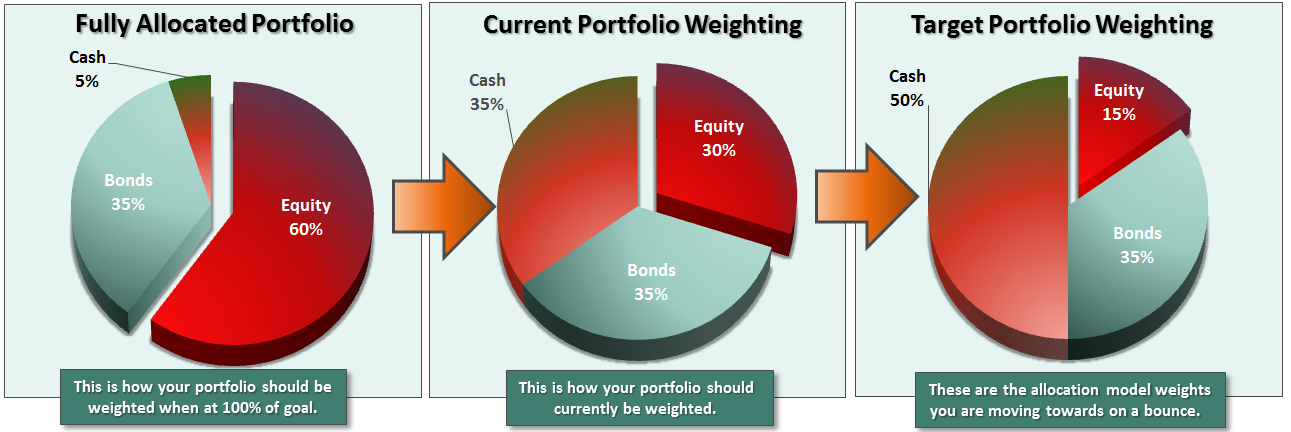

“The problem is that the expected rally was much less than previously anticipated. Therefore, ANY RALLY in the next week, OR A BREAK below the recent lows, requires that the allocation model moves to its final target levels of 25% exposure as shown below.

The current market environment is NOT conducive to an overweight allocation to equity risk currently.”

Therefore, if you have not done so as yet, on any rally this coming week reduce equity exposure in portfolios to target levels.

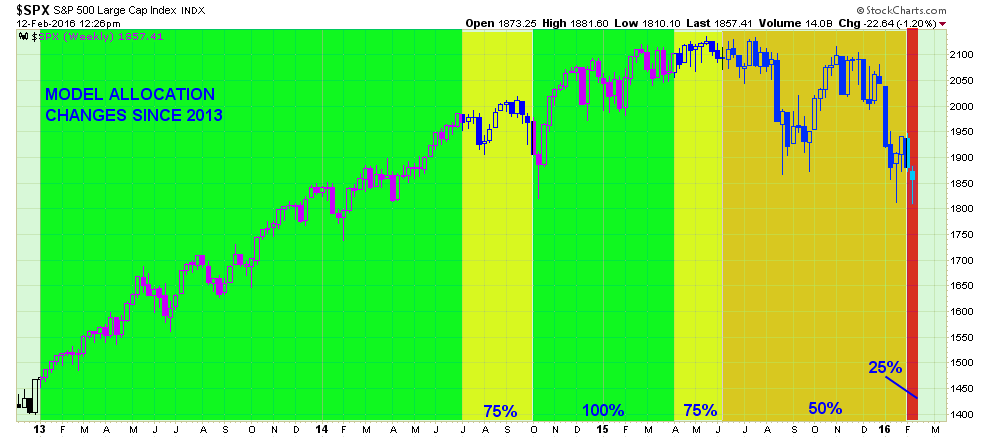

The next chart tracks the changes I have been discussing since the beginning of 2013 just in case you are a newer reader.

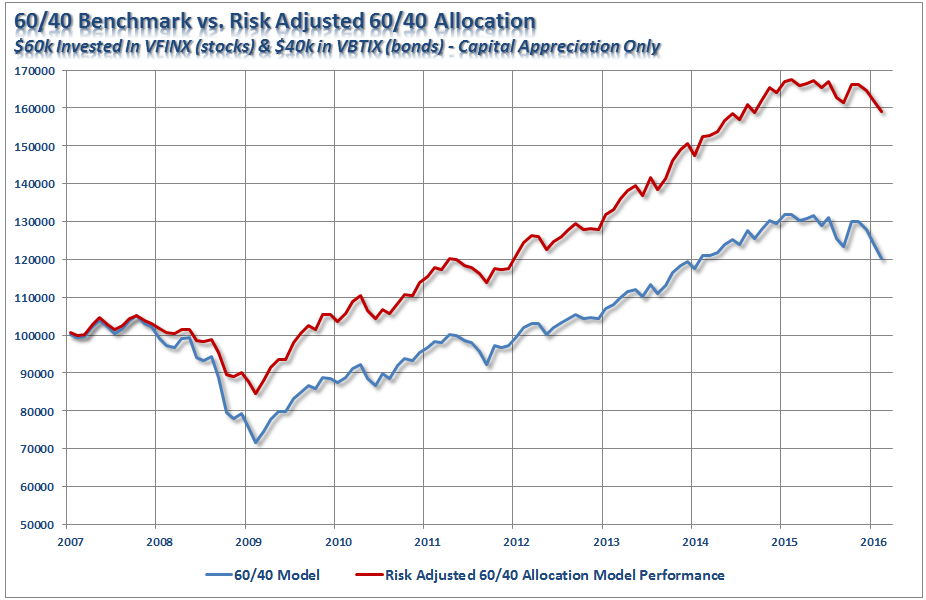

The next chart tracks the changes going back to 2007 of a hypothetical 60/40 stock/bond allocation versus the same model adjusted for the changes to manage downside risk.

As you will notice, not surprisingly, the bulk of the outperformance over the long-term was generated in 2008.

By reducing portfolio risk further this week, it now gives me cash, and substantially lower volatility, with which I can start looking for opportunities.

That’s right, I am suggesting selling into any rally over the next few days to further reduce portfolio risk. Importantly, I said reduce risk. I did not say eliminate it. With the market oversold short-term, and the Federal Reserve an unknown wild card, I do not want to be completely out of equities just in case “possibilities” overtake “probabilities.”

Like playing the lottery, there is an almost non-existent possibility I could pick the winning combination. The probabilities are heavily weighted against that outcome. By reducing risk, I can take my time to look for higher reward-to-risk opportunities to reinvest capital in the future.

If I am wrong, and the market doesn’t decline further as expected, when the market regains it “bullish step,” I can start buying again with a slightly higher relative degree of safety.

If I am right, and the market does have a further bear market correction, I will be able to reinvest capital at substantially reduced valuations down the rode.

{kind=link}