Fed Stops Profits Recession

Over the last several months, I have discussed the ongoing profits recession as reported by the Bureau of Economic Analysis. To wit:

“As Jeremy Grantham once stated:

‘Profit margins are probably the most mean-reverting series in finance, and if profit margins do not mean-revert, then something has gone badly wrong with capitalism. If high profits do not attract competition, there is something wrong with the system, and it is not functioning properly.’

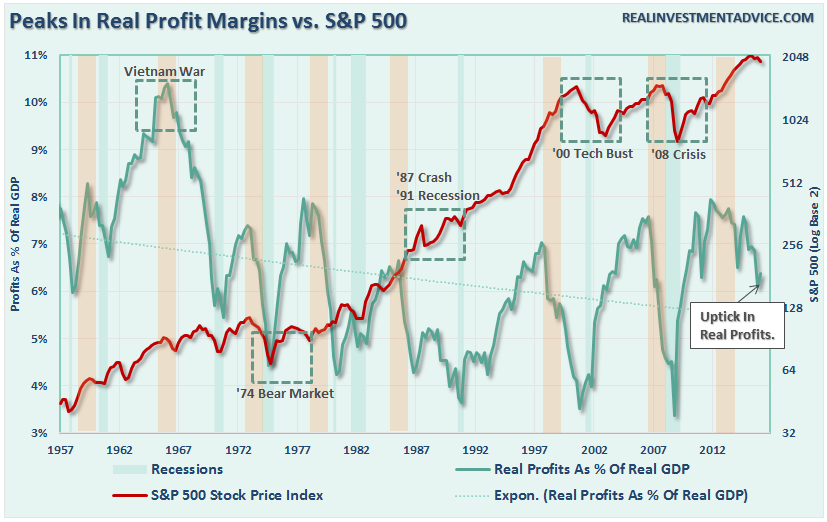

Grantham is correct. As shown, when we look at inflation-adjusted profit margins as a percentage of inflation-adjusted GDP we see a clear process of mean reverting activity over time.”

“Corporate profit margins have physical constraints. Out of each dollar of revenue created there are costs such as infrastructure, R&D, wages, etc. Currently, one of the biggest beneficiaries to expanding profit margins has been the suppression of employment and wage growth and artificially suppressed interest rates that have significantly lowered borrowing costs. Should either of the issues change in the future, the impact to profit margins will likely be significant.”

I remind you of this point because Wolf Richter brought forth a valuable piece of insight into the understanding of corporate profits are reported by the BEA.

“But there’s a detail – a huge detail – that the media conveniently forgot to point out: whose profits are included in “corporate profits.” The BEA tells us (emphasis added):

These organizations consist of all entities required to file federal corporate tax returns, including mutual financial institutions and cooperatives subject to federal income tax; nonprofit organizations that primarily serve business;Federal Reserve banks; and federally sponsored credit agencies.

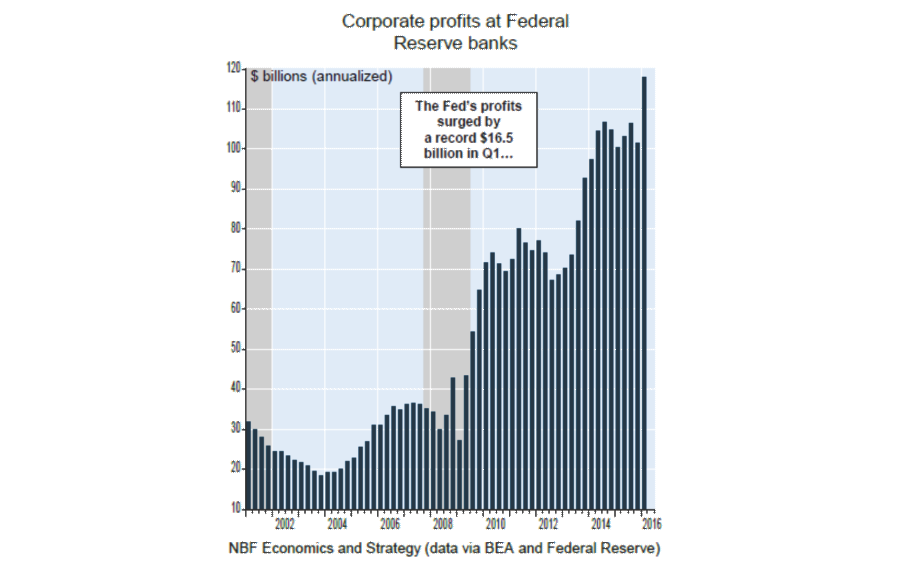

Ah yes, the Federal Reserve Banks (FRB), which include the 12 regional Federal Reserve Banks, such as the New York Fed. They’re private banks, owned by the largest financial institutions in their respective districts. And as private banks, their consolidated profits are added to US financial sector profits, and thus overall corporate profits, along with those from Goldman Sachs, JP Morgan, and your local bank down the street.”

Here is the problem, the profits provided by the Fed Reserve banks skew the analysis of profitability by actual operating companies. As noted by Wolf:

“For the first quarter, the Federal Reserve Banks reported a consolidated profit that had jumped 11% from a year earlier to a record $24.9 billion!

And this magic profit was added to the BEA’s measure of “corporate profits.” Total corporate profits ticked up $8.1 billion in the first quarter, including the Fed’s magic $24.9 billion. And without the Fed’s magic profits?”

The addition of $24.9 billion in profits from the Federal Reserve are simply recycled back to the Treasury. They do NOT circulate back into the economy boosting economic growth, higher wages or stronger consumption. More importantly, the Fed balance sheet has been skewing corporate profits to an ever increasing degree since the end of the “financial crisis.”

Importantly, while the media cheered the slight increase in profits in Q1 as a “sign of the end of the profits recession,” had it not been for the addition of the Fed, profits would have been negative for a 3rd consecutive quarter.

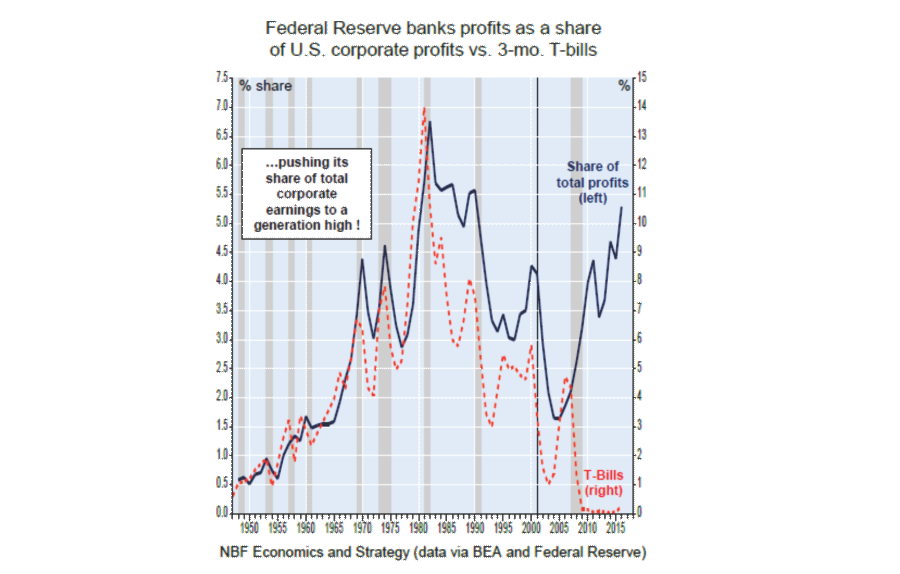

“In fact, on an annualized basis, the Fed’s magic profits accounted for 27.2% of US financial sector profits and for 5.3% of total US corporate profits (blue line in the chart below), ‘the highest level in a generation.’”

This is easy enough to understand, an improvement in corporate profits driven by a recycling of interest payments between the Fed and the Treasury is not a sign of a healthy economy.

Of course, the media will continue to ignore what is happening beneath the surface until it is far too late to matter.

Corporate Debt Surges

But let’s stay with this idea of corporate profitability for a moment. As I discussed previously, there is a difference between profits driven by organic economic growth and artificially derived profits. To wit:

“However, not surprisingly, shortly after I published the article I received numerous emails citing low interest rates, accounting rule changes, and debt-funded buybacks all as reasons why “this time is different.” While such could possibly be true, it is worth noting that each of these supports are both artificial and finite in nature.

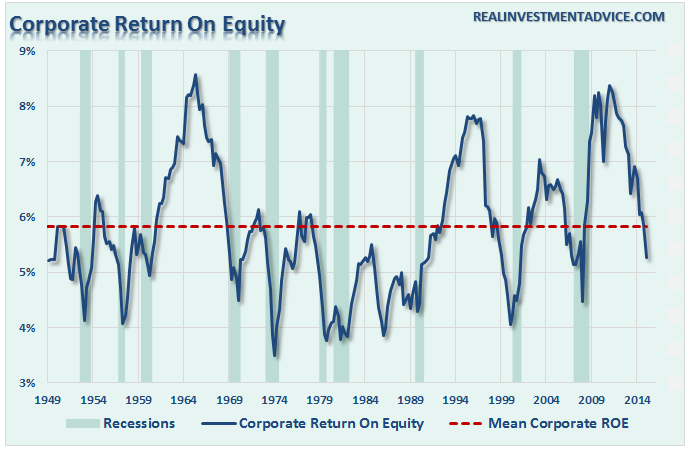

These actions, as suggested above, are limited in nature. For a while, these devices kept ROE elevated, however, the efficacy of those actions has now been reached.”

“Importantly, profit margins and ROE are reasonably well-correlated which is what creates the perception that profit margins mean-revert. However, ROE is a better indicator of what is happening inside of corporate balance sheets more so than just profit margins. The current collapse in ROE is likely sending a much darker message about corporate health than profit margins currently.”

Since debt is a primary component of ROE, it should be noted that the collapse in ROE is representative of the increasing levels of debt to fund stock buybacks and dividend issuances. Of course, it is those debt-funded stock buybacks in particular that have continued to obfuscate the deterioration that is occurring below the surface.

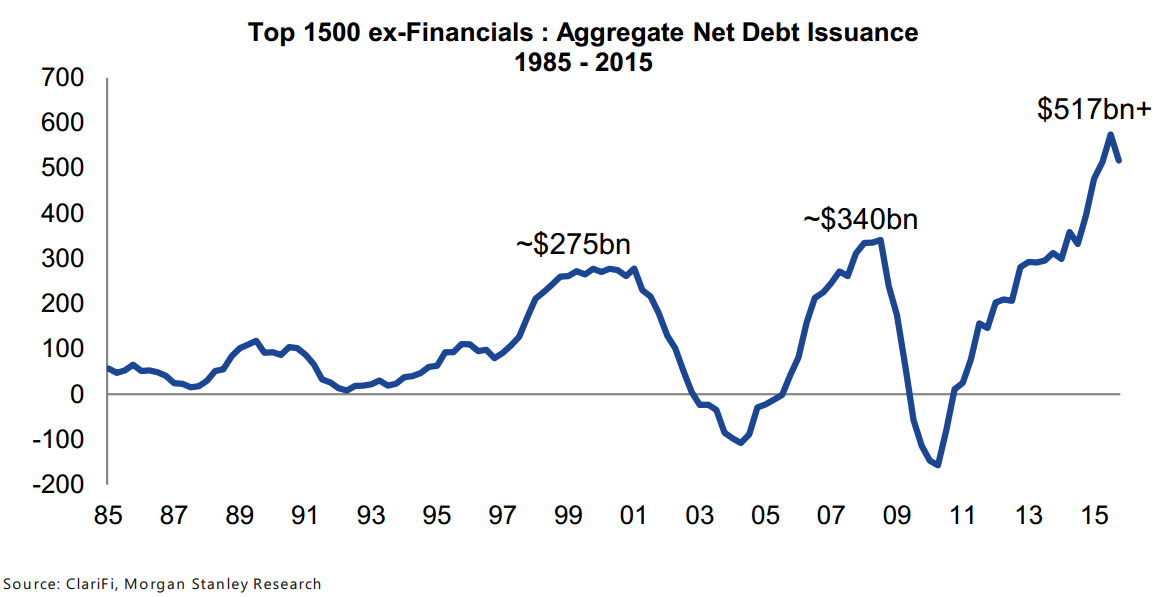

Over the past 12-months, US corporations have added a massive $517 billion in new debt to their balance sheets which is the second highest level ever.

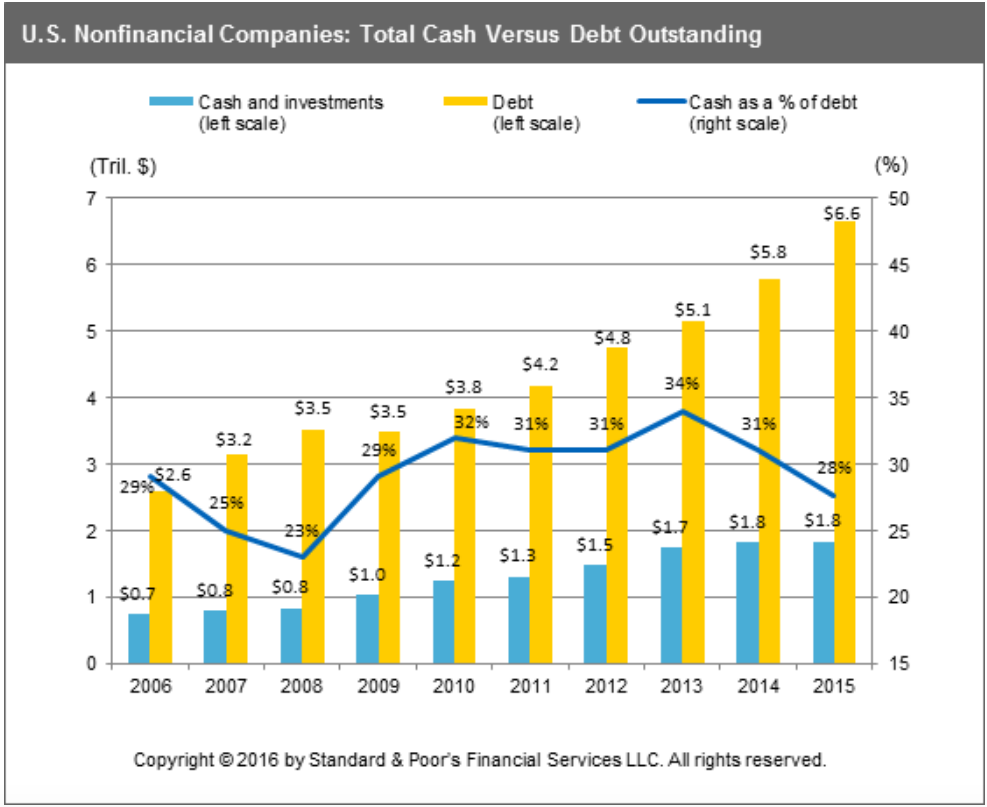

While companies do have extremely high levels of cash currently, as noted in the chart below, the majority of that cash is held in overseas operations and is not readily available to pay down debt levels should a problem develop. Furthermore, the net cash to debt levels has deteriorated markedly over the last two years in particular as the drive to buy back shares to boost bottom line earnings results has been the “go to” option for revenue-starved companies.

According to a new report from Andrew Chang and David Tesher of S&P Global Ratings.

“At the same time, the imbalance between cash and debt outstanding we reported on last year has gotten even worse: Debt outstanding increased 50x that of cash in 2015.

Total debt rose by roughly $850 billion to $6.6 trillion last year, dwarfing the 1% cash growth ($17 billion).

Removing the top 25 cash holders from the equation paints an even more concerning picture: Total debt rose $730 billion in 2015, while cash declined by $40 billion.”

Historically speaking, it is unlikely that with reported earnings early in the reversion process that we will see a sharp recovery in the second half of the year as currently expected by the majority of mainstream analysts. As long as the Fed remains accommodative, the deviation between fundamentals and fantasy will continue to stretch to extremes. The end result of which has never “been different this time.”

The Next 10-Years Of Low Returns

A couple of years ago, I began discussing the rising probabilities of a decade, or more, of low returns which was based on commentary at that time by Research Affiliates.

In their research paper, they discussed the impact of “secular stagnation” which would lead to lower future market returns over the next decade. How low you ask?

How about 1% kind of low?

“But Lance, the markets has returned 10% on average over the last century, so RA is probably going to be wrong.”

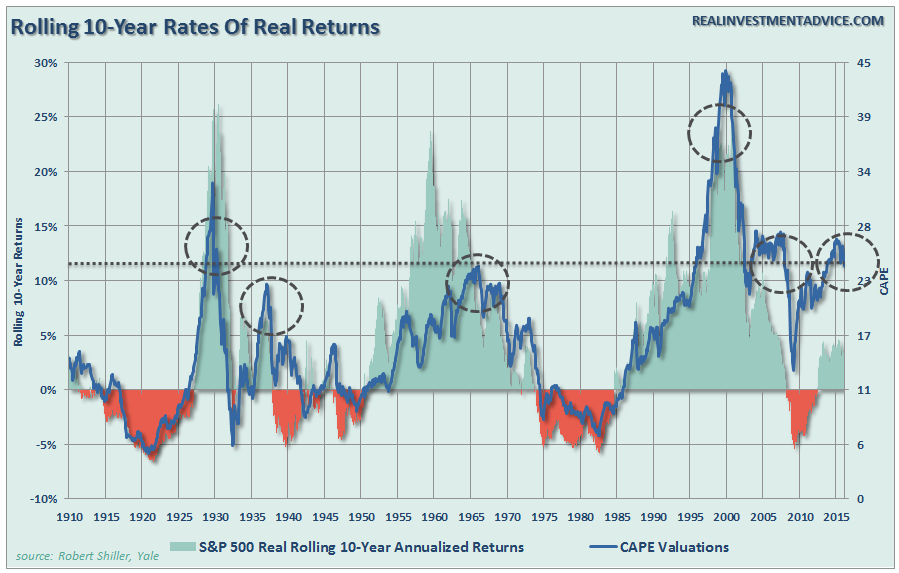

Before you dismiss RA’s comments, it is important to put them into some context. When low rates of return are discussed, it is not meant that each year will be low but that the return for the entire period will be low. The chart below shows 10-year rolling REAL, inflation-adjusted, returns in the markets. (Important note: Many advisors/analysts often pen that the market has never had a 10 or 20-year negative return. That is only on a nominal basis and should be disregarded as inflation must be included in the debate.)

However, we can also calculate low future returns with math:

Capital gains from markets are primarily a function of market capitalization, nominal economic growth plus the dividend yield.

(1+nominal GDP growth)*(normal market cap to GDP ratio / actual market cap to GDP ratio)^(1/10)-1+(dividend yield)

Therefore, IF we assume that real GDP could maintain 2% annualized growth in the future, with no recessions, AND IF current market cap/GDP stays flat at 1, AND IF the current dividend yield of roughly 2% remains, we get forward returns of:

(1.02)*(.8/1)^(1/10)-1+.02 = 1.7%

But there are a “whole lotta ifs” in that assumption. More importantly, if we assume that inflation remains stagnant at 2%, as the Fed hopes, this would mean a real rate of return of -0.3%. This is certainly not what investors are hoping for.

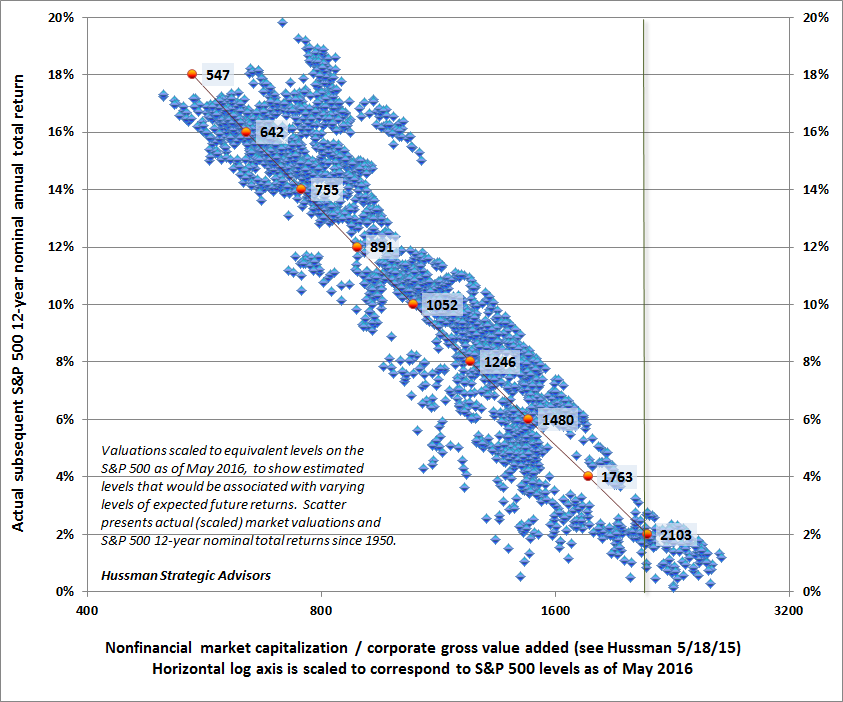

John Hussman just recently penned a similar perspective on prospective 10-12 year returns.

“Simply put, if investors view expected 10-12 year S&P 500 total returns in the 0-2% range as ‘fair,’ and believe these expected returns are acceptable compensation for a likely interim retreat in the range of 40-55% over the completion of the current market cycle, it’s reasonable to say that the S&P 500 is ‘fairly valued.’ Understand, however, that this is exactly what investors are saying when they assert that current stock prices are ‘justified’ by low interest rates.”

Just some things to think about.

Lance Roberts

Lance Roberts is a Chief Portfolio Strategist/Economist for Clarity Financial. He is also the host of “The Lance Roberts Show” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, and Linked-In