The European mess is coming more into view, and in almost every case that is a negative outcome. There really isn’t much going right in Europe right now, belying everything that was said, done or proclaimed only a year ago.

Italian unemployment unexpectedly rose to a record high that’s more than double the German rate, keeping alive concerns about the diverging growth outlook in the euro area.

The jobless rate increased to 13.4 percent from a revised 13.3 percent in October, while separate data showed the euro-region rate at 11.5 percent. The reports contrast with data from Germany showing unemployment there fell to the lowest in more than two decades last month.

I highly doubt that Italy’s retrenching was “unexpected” as weakness has been obvious in the Eurozone for months now. If it wasn’t enough that credit markets are so completely distorted as to be unrecognizable to fundamental tenets of finance, then at least observing the desperation with which the ECB has operated since June would be a clue. And that raises a fundamental question about mainstream views on monetary economics, as expressed below by the New York Times in merely observing, detached, the final coming of “negative inflation.”

But the question raised by many economists is whether the European Central Bank has waited too long to act, and whether its arsenal is powerful enough to address the eurozone’s fundamental problem — a dearth of demand from businesses and consumers for goods and services.

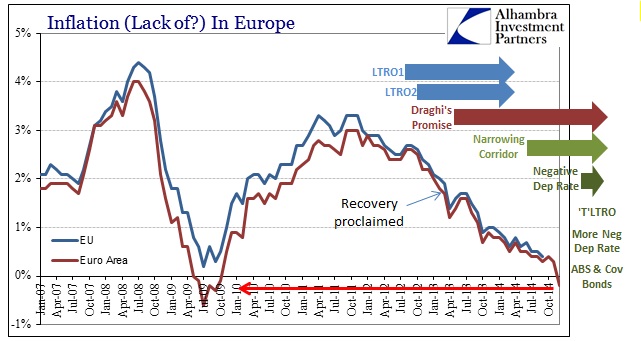

Have not the economists noticed the constant attention on Mario Draghi this year? I find it hard to believe that everything the ECB has done to this point has slipped unnoticed even to the narrow gaze of “economists.” Rather, they likely wish that nobody would notice how everything, which has been a constant and unnatural noise emanating from that balance sheet, has simply failed to this point.

Plotting Eurozone “inflation” shows absolutely no imprint of the ECB anywhere, so maybe unfamiliar observers would be forgiven for missing all the fuss; none of the trillions in euros have mattered and that is the main point to which “economists” wish to plead ignorance (on your behalf).

The second part of that NYT quote may actually be more problematic, as if the ECB could invoke “demand” out of monetary nothingness. Aggregate demand adherents, who encompass the entire orthodox complex and nearly every major central bank (with one evolving), certainly believe that increasing credit is tantamount to conjuring “demand.” To that end, “fixing” the banking system was paramount, but we see unequivocally that there is no reciprocation, at all.

The entire theory of monetarism is coming undone in spectacular and empirical fashion, which leaves the entire status quo exposed. All that is left in defense is the same old refrain of “it wasn’t big enough.” That’s great for those in the ivory towers blinding themselves to the reality of a lost generation of Italians, Spaniards, French and now even Germans; a listing to which even the FOMC is worried may yet add Americans.

Why anyone ever expected a different outcome is due solely to unrepentant ideology, since these central banks are following almost exactly the Japanese “model.” The global economy is just following along as money dies. Though Greece will be blamed as contagion, it will ultimately be proved as Japanification by monetary proxy.