The word “unexpectedly” has made its appearance in Japan with the latest quarterly GDP release. Economists had forecast between +2.2% and +2.5%, so -1.6% counts for an “outlier” to commentary. This result, following a quarter where GDP already fell 7.3%, is nothing short of atrocious and leaves no doubt the disastrous shape to which Japan has befallen. As I said last week, this should have been very much expected not only by the flurry of activity in the Abe government (hints at both delaying the next tax increase and calling a snap election before economic dissatisfaction rises to US-type levels) and the panic in the BoJ, but just plain common sense based on what has transpired in the past eighteen months of QQE.

Already the long knives are sharpened for the tax change, giving voice, no doubt, to the reemergence of Keynesian doctrine that despises all fiscal sanity but especially when the economy is reversing, when that was simply the final straw placed onto an already “inflation” burdened Japanese camel.

Japan’s economy has plunged into a shock recession after shrinking by 0.4pc in the third quarter.

The economic contraction was spurred by the introduction of a sales tax increase earlier this year that is thought to have strangled consumer spending and is likely to delay Japanese prime minister Shinzo Abe’s plans to introduce a further increase to the sales tax in October next year. [emphasis added]

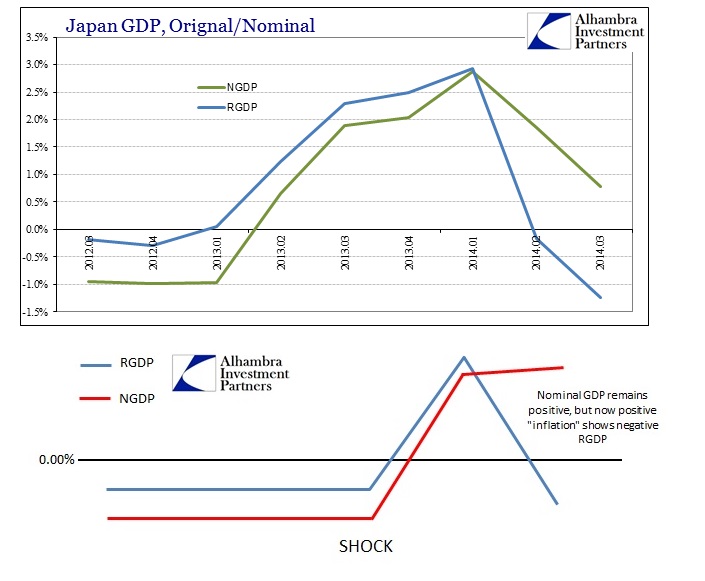

Orthodox theory about “inflation” as an economic elixir continues to be backward. Economists somehow think that by creating greater inflation expectations that consumers (and businesses) will bring forward activity, “spurring” a burst that will lead to follow-on activity and then a functioning economy. Perhaps in mathematical modeling that is what it looks like when the variables are all pre-ordained to that direction, but there is no real economic recovery to follow a period where consumers and businesses are scared into acting contrary to their own perceptions. You cannot build an economy by the preponderance of a negative factor.

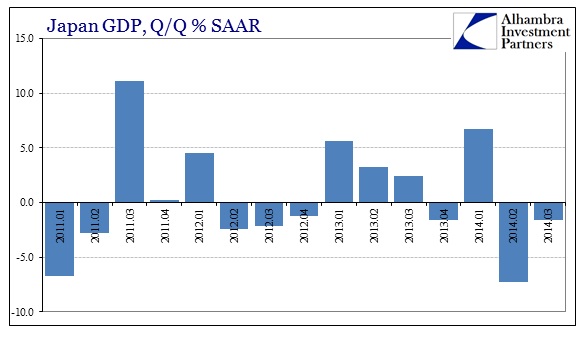

It is that point where Q1 in Japan was not salutary toward the recovery idea, but instead indicated massive problems. The fact that Q1 activity “surged” proved just how wary Japanese consumers (in particular) were ahead of the increase. A healthy economy would pay only minimal attention to the tax change, with very small amplitude before and after. An economy posed upon the precipice would do the opposite, as consumers and businesses that “pull forward” an immense proportion of potential future activity are expressing extremely dour sentiment toward future abilities.

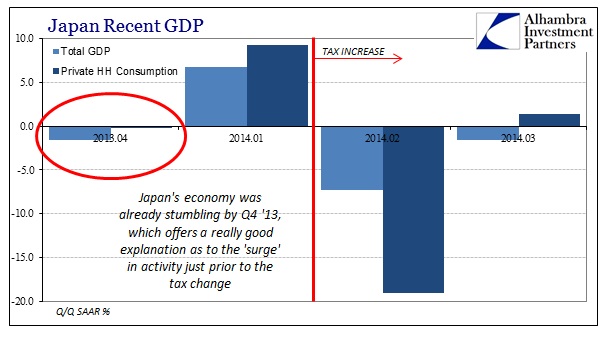

That is exactly what happened in Japan, which some are taking as blame unto the tax change. But any read of even GDP shows that Japan was already falling into recession by Q4 2013:

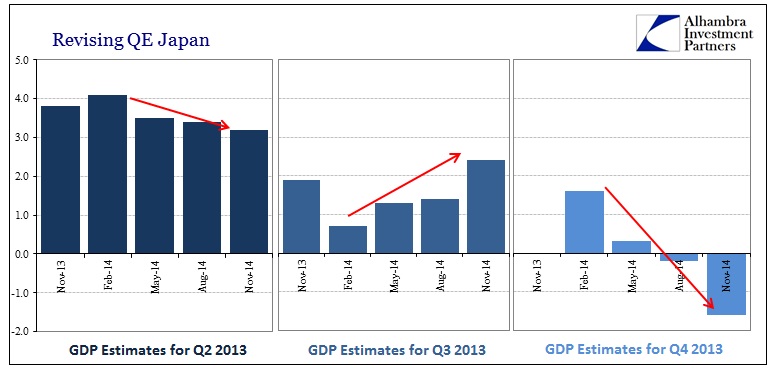

Confirmation of that has been obscured by the constant downward revisions to GDP for Q4, but even in its first release it had already disappointed in that it failed “follow through” from Q3 and thus headed in the wrong direction into the tax change; regardless of the ultimate revisions. In that respect, the downward revisions, taking Q4 ’13 from +1.6% in it its first estimate in February to -1.6% as of the latest figures, are only confirming what we knew to be the case from Q1’s damning “surge.”

Judging by the last four quarters, the recession in Japan seems to have begun during the last three months of 2013 – not at the start of the tax increase.

The reason for that is relatively straightforward, as the Bank of Japan as the primary tool of Abenomics got what it wanted, and then some:

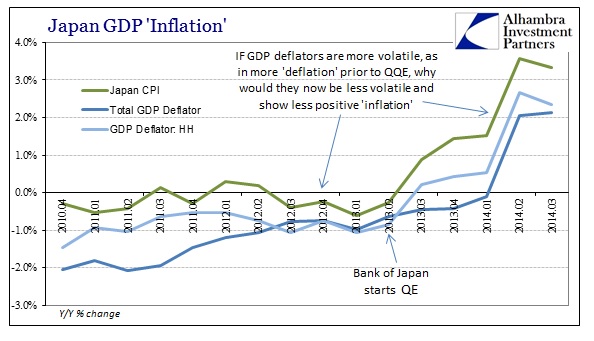

While the overall GDP deflator did not actually turn positive until Q1, in contrast to the deflator of Household Consumption, that only suggests that GDP is, as it always seems to, undercounting “inflation” as harmful to economic activity. Somehow these GDP deflators continue to estimate less inflation than the CPI when the tendency to “over”-estimate “deflation” from the same deflators suggested the opposite. In other words, if the GDP deflators were more volatile toward price estimation when prices were “negative”, the same should hold for when prices are “positive”, as now.

Regardless, the timing of the turn toward positive “inflation” of whatever level of debasement and thus negative GDP (Q4) more than suggests, empirically, when this “unexpected” recession actually began and to what causation. To that end, the Household and consumption figures were truly alarming in the GDP subsets, but that too should have been expected from the Household income accounts that have been warning since January (again the Q4 ’13 timing).

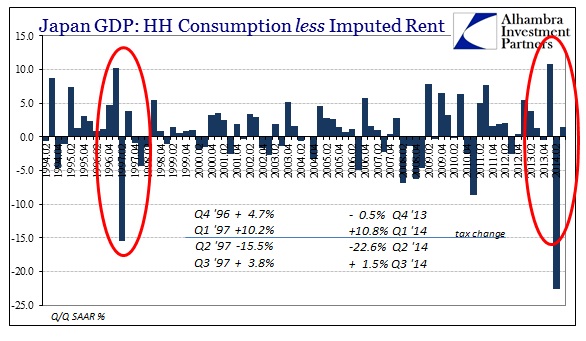

After falling almost 23% in Q2 (SAAR), household consumption only rebounded by a tiny 1.5%? There isn’t much commentary needed except to suggest that depression in context. The last time Japan turned to a relatively small measure of fiscal discipline was, of course, 1997. The recession that followed (again, not driven by the tax increase itself) was dire not just in scope and degree, but in cementing the idea that Japan needed “radical” monetary measures to get out of “deflation.” That recession also precipitated the Asian flu crisis that destroyed the Asian “tiger” mentality and spurred a global movement toward financialism (as Asian nations piled up “reserves”, cheered by economists then, but now scorned by the very same; almost as if orthodox economics can’t decide what actually “works”).

As you can see above, the current track of pure Household spending (ex imputations of owner implied rent) is much, much worse than even 1997. The economy started from a worse position, collapsed further and has rebounded far less.

Taken together, none of what is happening in Japan is “unexpected” as the signs have all been there since at least Q4 2013, if not 1997. Failing all that data, there was always plain common sense about “inflation”: