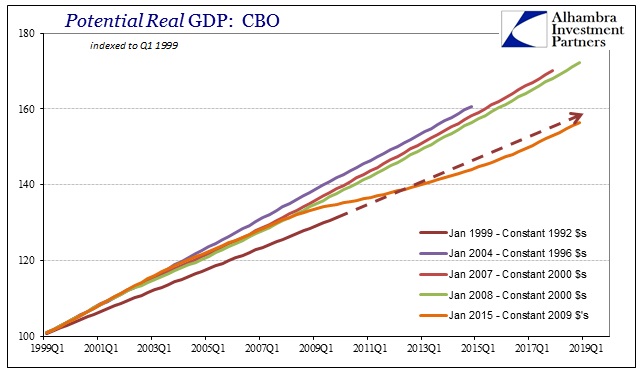

In looking through the CBO’s litany of economic projections, past and present, I wrote yesterday that the major economic problem started to become clear by what was missing. The main orthodox models all view economic potential in much the same fashion, as if the economy exists completely upon a curve of inflation and employment, whereby the intersection of those two directs the most constructive meaning. It isn’t just the models, however, that are flawed by seeing true economic work under those terms. Actual, orthodox theory is one of “aggregate demand” which, similarly, cannot grasp an economy as it actually exists.

Economists view the economy through statistics, which I have charged numerous times renders them “experts” of nothing more than math, certainly not of business interactions in the capitalist tradition. From that philosophical foundation and perspective, the economy appears almost if not fully mechanical rather than the living organism that it really is. Therefore, as a machine, an asset bubble makes sense while at the very same time individual people’s recoiling horror of them does not. Janet Yellen, as part of the newish Yellen Doctrine, wants you to be completely comfortable with asset bubbles as simply an extended tool of monetary policy through more naked monetarism; she cannot understand why you don’t or will never sign up for that with unrestrained vigor and just trust her and the FOMC’s prowess about the results.

Aggregate demand will simply see GDP as the correct economic expression, meaning that no matter how it is achieved it is “correct.” This is spending for the sake of spending, especially by government and especially by government that borrows “free money.” The most vocal and visible proponent of this Keynesian/monetarist fusion is Paul Krugman, but he is not alone and is, in reality, of very little difference to Ben Bernanke or Janet Yellen. They may quibble about minor issues here and there, but the basis for that discussion is always the mechanical view.

In September 2011, Krugman demonstrated very well how this is supposed to work. Writing about, of all things, ozone regulation, Dr. Krugman was distraught not just at the environmental indignity but the lost economic opportunity. He was actually proposing greater and expensive regulation as “stimulus.”

As some of us keep trying to point out, the United States is in a liquidity trap: private spending is inadequate to achieve full employment, and with short-term interest rates close to zero, conventional monetary policy is exhausted.

This puts us in a world of topsy-turvy, in which many of the usual rules of economics cease to hold. Thrift leads to lower investment; wage cuts reduce employment; even higher productivity can be a bad thing. And the broken windows fallacy ceases to be a fallacy: something that forces firms to replace capital, even if that something seemingly makes them poorer, can stimulate spending and raise employment. Indeed, in the absence of effective policy, that’s how recovery eventually happens: as Keynes put it, a slump goes on until “the shortage of capital through use, decay and obsolescence” gets firms spending again to replace their plant and equipment.

There is some real truth to his “how recovery eventually happens.” The form of recession often is amplified by the reverse of what is proposed above, as businesses in a downturn begin to put off necessary capital expenditures (as do consumers who take back and delay discretionary impulses). So it makes some very basic sense in getting a recovery started by “helping” businesses with getting back to a more normal capital expenditures footing; to resume spending that was previously put off.

And now you can see why tighter ozone regulation would actually have created jobs: it would have forced firms to spend on upgrading or replacing equipment, helping to boost demand. Yes, it would have cost money — but that’s the point! And with corporations sitting on lots of idle cash, the money spent would not, to any significant extent, come at the expense of other investment.

Even with that basic truth, you can start to see, in full view, why this is utter nonsense. I don’t need to rehash the broken windows fallacy, which Krugman actually says is no longer applicable because of some “liquidity trap”, only to point out how this economic view is so very incomplete. He writes that “in the absence of effective policy” that is where recovery comes from, and so it does not matter that further regulatory burden is actually a burden as all that matters is spending and transactions for the sake of spending and transactions (the housing bubble “works” in the same respect); as economists will be quick to point out, that spending is someone else’s income; i.e., redistribution. So if you won’t spend on your own, the government should find ways to force it so that “idle cash” no longer is.

But none of that is what actually creates a recovery in the first place. Conspicuously absent from his discussion, which is typically brief, is the idea that “idle cash” doesn’t actually exist. Underconsumption theory was superseded and recast by bank balance sheet construction more than half a century ago (he doesn’t know how “money” is created in the eurodollar/wholesale system). Recoveries are not even so much monetary as they are, again, organic. Redistribution only attempts to mimic the processes, as to “fool” businesses and consumers into thinking that whatever caused a recession is no longer so dangerous and immediate.

That is also common between the fiscal version of redistribution as its monetary compliment. The aim of ZIRP and QE’s is to fool financial agents into seeing the numbers and prices of assets and financial indications as they would during more healthy conditions (a steeper yield curve, more “behaved” VaR, etc.). In short, policy constructs the visible façade of recovery in the expectation that businesses and consumers will then fill it out beyond, a mechanical response to only noticeable changes. In that way, the fiscal view and the monetary view are supposed to be highly complimentary, as the government redistribution creates spending transactions financed by the monetary, central bank redistribution through asset prices and debt (modern “money”).

Recovery is actually none of that, as what drives actual spending apart from forced redistribution is always opportunity; and that is not something that can be faked or reduced into mechanical, spreadsheet formality. In Krugman’s ozone fantasy, he takes no account of the offsetting impacts upon the businesses under the thumb of new regulations; they might, indeed, actually update equipment but will also cut back on something else. On net, spending does become someone else’s income but at the expense of some other business. Worse, the spending that does take place does so not on economic considerations which will offer sustained advance but rather arbitrarily by diktat; and what is cut back is as likely a truer economic factor that would have offered greater long-term support.

On net, the effects may already be negative as arbitrary spending displaces real and existing economic activity (broken windows fallacy), but there are also further effects on unrelated business. Upon seeing these companies forced to address such “stimulus”, businesses elsewhere undoubtedly start to factor that arbitrary process as increasing in likelihood for their own efforts. In other words, if government is going to get the recovery started by costly ozone regulations, they will not likely stop there, having a greatly diminishing effect on overall, perceived opportunity. You cannot create positive economic momentum by widespread preponderance of highly negative factors and costs. It is almost childishly naive to expect that all this would occur in a vacuum, that business in general would be so unaware and unaffected.

In an economic system awash and saturated with just such thinking, you can start to appreciate how and why arbitrary mandates may instead actually dispel more organic trends. Again, the statistician economist does not care about how and why transactions takes place, only considering the raw volume. To him, transactions that accumulate thus signal recovery where they, in fact, only suggest further decay at just delayed toward some point in the future. This is seen more recently upon healthcare spending, which is undoubtedly one reason for the current recession in consumerism.

It matters a great deal the channels and pathways of activity, as not all activity is a perfect substitute and government-drawn redistribution is almost always far more inefficient:

If, however, the circus because of the increase in attendance, is forced by the government to radically up its insurance outlays, eradicating much of the new profit potential, that would lead further economic circulation outside of the circus and toward the insurance company. If the insurance company had to hire new underwriters and investigators to service the new policies and limits, then this redistribution on net is similar enough to also be economically useful. There is, though, a major difference in that demand for labor shifts from entertainers (a particular specialty) to demand for finance types (another specialty). So redistribution is not neutral and should be taken into account at least qualitatively.

But in reality, the insurance company hiring is not going to be the same as the circus hiring since the new policies are likely to flow instead to the insurance company’s bottom line (which is why they are predisposed to lobby government so heavily). There may be a few new hires, but nothing on the level of what the circus might have done with the same amount of profit. In this case, economic circulation from increased “demand” for the circus now flows into an insurance company’s profits which are either reinvested in an asset “market” or distributed to the owners. The economic channel in this manner is much less efficient toward actual economic gains, i.e., true wealth and labor utilization.

That is the pathology, in banking rather than insurance, of the housing bubble – there is a great difference when one set of transactions is forced or induced instead of the natural course. Once that forced (or that taken under asset inflation) spending takes place, then what? There is a temporary burst of artificial activity which the beneficiary of that arbitrary redistribution views as similarly temporary. When the ozone regulations run their course, so does the redistribution, a fact that the beneficiary is quite well aware of meaning that the economy is not fooled by artificial opportunity in sharp contrast to actual and natural opportunity (this was “proved”, as if it needed to be, by economists studying the ARRA itself among school district recipients of federal grants).

The problem of mainstream economics, in general and generic terms, is its overriding tendency to want to fake recoveries and do nothing more, expecting that such trickery amounts to if not the exact same thing then at least close enough. That is as much because of viewing the economy as a series of mundane, uninteresting and not meaningful transactions – a huge misapprehension of how an economy actually works. The economy is not just a series of transactions strung together by arbitrary function, but rather an indecipherable and complex, living organism where there is decentralized and dispersed meaning behind what occurs that can never be commanded, let alone understood, by central planning on a granular level.

It is beyond weird and unseemly that it has to be pointed out to economists, taken in the main as experts on the economy, that recovery by increased cost doesn’t work! Similarly, the steepest yield curve imaginable is not in any way the same thing as opportunity. Unfortunately, economic and financial agents, the regular people that have to live under these theories, are not dumb enough to fall for any of it. Economists believe that their negative pressures are better than nothing only because they cannot fathom that they are negative pressures, calling into question which side is actually playing the fool.