When something like the truly freakish chart below appears, you’d think that even the Wall Street gamblers would get their collective heads out of the sand.

The fact that in September 2017 Austria was able to issue a 100-year bond at a mere 2.1% yield was crazy enough. After all, the old Austria (Austro-Hungarian Empire) disappeared exactly 100 years ago at the Versailles Conference; the rump state left behind was nearly crushed by Hitler in the 1930s and the Soviet Union in the 1950’s; and for the last 70-years inflation has averaged 2% at least, while the welfare state keeps growing and taxes keep rising.

So why so-called “investors” purchased a 100-year bond with the prospect of virtually no yield after inflation and taxes and a reasonable doubt as to whether the Austrian state would survive to 2117 was always a bit of a mystery.

But it could perhaps be explained by the Greater Fool theory. That is, there wasn’t much yield to be had anywhere else in Europe, and a smart asset manager could always collect the 2.1% yield and get out of Dodge at the first sign of credit weakening, rising inflation or default troubles by dumping this dubious paper on the next in-rotation mullets.

That was then, and as they say on late night TV, there’s more. Much more!

In the the interim, the price of this EUR 3.5 billion beauty soared by 60% from the issue price, forcing the already meager yield down to just 1.12% by late June. So, not surprisingly, the Austrian government didn’t need any special prompting: It reopened the issue and sold another EUR 1.25 billion tranche due 2117 for a yield barely above 1.0%.

Even then, the madness was just getting up a head of steam. As the amount of subzero debt in the world soared from $10 trillion to $15 trillion during the last 60 days, the price of the Austrian bond climbed sharply to nearly 186% of par, meaning that the current yield is now well below 1.00%, but more importantly, the bonfires of speculator stupidity are now sure to ignite.

That is to say, if the nation of Austria and the solvency of its government manage to survive until 2117, the current holders and all their heirs and assigns and next in rotation mullets are guaranteed to collectively loose the entire 86% premium embodied in today’s price—-since even a solvent Austria would only redeem the bond at par. Of course, that guaranteed principal loss would wipe out approximately the next 40 years worth of interest—-even if you don’t care about inflation, taxes and the present value of payments 100-years out in the bye-and-bye.

But here’s the more incendiary point. The bond’s price is now going parabolic, as is evident in the right-hand side of the chart. That’s because there is massive convexity in ultra long-dated paper, meaning that just a few basis points of yield change will cause a very large change in price.

For instance, if the central banks of the world manage to drive average global yields another 50 basis points lower by next August, the bond’s price will rise to about 244%. And just easy peasy, a speculator who bought the original issue in September 2017 would have booked a 150% profit (including interest). On a bond!

Moreover, if he funded the purchase on margin or repo, the gain would be orders of magnitude higher.

That’s why they are buying this junk. It’s a price-chasing speculative mania that has gone absolutely bonkers in all of the fixed income markets of the world, of which the Austria 100-year bond is only the leading edge.

And that gets to the topic at hand. Keynesian central bankers and their Wall Street apologists want you to believe that subzero debt isn’t crazy at all, and certainly not a consequence of their own massive bond buying.

Instead, they have invented absolute tommyrot to explain the otherwise inexplicable. To wit, the bogus claim that the world is suffering from a massive “savings glut” and that subzero yields are simply Mr. Market at work clearing that decks of supply and demand.

Likewise, Mr. Market is also supposedly discounting a very weak recessionary global economy ahead, thereby driving down yields in anticipation of faltering demand for borrowed money and sinking inflation rates.

In other words, this race to the yield bottom is supposedly rational—-the pricing out of totally new conditions that have emerged in the global economy and fixed income markets.

Well, if you want to contemplate “rational”, just consider this. Were global interest rates to rise just 1.0% on average—-back to where they were less than a year ago—the Austria bond sitting up there in the nosebleed section of financial history at 185.75 would plunge to just 115 for nearly a 40% wipeout!

Needless to say, that would happen not decades from now, but next year; and not after an unprecedented financial conflagration, but just with a return to interest rates that prevailed well less than one year back.

That’s right. The 10-year UST closed at a 1.65% yield today, but as recently as February 11 it had yielded 2.65%.

Likewise, the German 10-year bund closed at negative 0.59%—crazy enough itself—but was one percent higher at +0.41% in October 2018. And same story goes with the British 10-year gilt which has moved from a 1.49% yield last October to just 0.49% today.

Needless to say, the 100-year Austrian bond is not some kind of one-of-a-kind freakish side show in the far back of the financial circus. As the grid below shows, there are now trillions of long-dated bonds that are trading at subzero yields, and which will positively crash in price when the current bond mania ends.

This has happened very rapidly. As recently as early 2015, there was less than $2 trillion of investment grade bonds trading at subzero yields, and by late 2017/early 2018 the figure was still generally less than $8 trillion.

But in recent months, it has gone parabolic, and that fact alone demolishes the Wall Street rationalizations. That is, there is no “savings glut” to begin with—-but even the modest savings rates now evident among the major world economies have changed very little since 2015 and hardly at all during the past year of soaring subzero yielders on the global market.

So the savings rate cannot even begin to explain the chart below.

In any event, here is the culprit. During the 15 year period between 2003 and 2018, there was indeed a “glut”, but it was one of central bank bond-buying, not honest-to-goodness real money savings out of current production and income.

In fact, the central banks collectively jammed their big fat thumbs on the scale of global supply and demand for savings and borrowings to the tune of $22 trillion. That is, $22 trillion of “demand” for government bonds and other securities that was funded by digital credits issued to the selling bond dealers that had been snatched from thin monetary air.

Not only has that saturated the markets with trillions of excess liquidity than can slosh into bond-buying in an instant in response to a risk-off headline, but more importantly, it has taught speculators a powerful lesion: Namely, to buy what central banks are buying or signaling the will be soon buying because that is literally the greatest front-running opportunity in recorded history.

And that’s why bond prices have gone parabolic in recent weeks and months, and why the mountain of subzero debt on global markets have been soaring by upwards of a trillion dollars in one or two days.

Just review the Austrian 100-year bond chart above because in slightly exaggerated form it demonstrates the powerful trading windfalls that result from central banks driving down interest rates in their futile attempts to stimulate sustainable growth, incomes and jobs. To wit, its cause longer-duration bond prices to soar, and turns fixed income investing on its head.

Instead of a venue for long-horizon investors to find safety and modest yield, the central banks have turned the bond pits into gambling forums where yields are irrelevant and short-term capital appreciation is the name of the game.

Except. Except. If you insist on buying Beyond Meat Inc at 125X sales or even a high flyer like Chipotle at 56X earnings, you can dream that much of the known world will soon become Vegan or go bonkers for an over-priced Burrito Bowl, but not so with these high-flying premium bonds.

Everywhere and always bonds will return to par at redemption, and collectively the traders and speculators who today are pleased to call themselves investors are going to loose their shirts.

That much is guaranteed. The only thing at issue is how soon the bloodbath comes, and how violently the financial terror spreads from the bond markets to the rest of the financial system

Combined Global Central Bank Balance Sheets—-Shrinkage For First Time In Modern History

As to the savings glut, that is simply risible nonsense. The chart below tells you all you need to know because it displays the US net savings rate in the most accurate manner possible. That is, it combines household savings plus corporate savings (i.e. retained earnings) plus government sector dis-savings, and compares that sum to national income.

That’s the most robust measure of “savings” because it represents the net sum left from current period income that can be used for investment, and it has been heading south for many decades.

At the current 2.1% level, it stands at a mere fraction of the 8-10% of national income level which prevailed during the heyday of American prosperity during the 1960s and later.

Nor is it the case, that US national savings have nearly vanished, but no matter because there is an even greater surplus in the rest of the world. But that’s blatant hogwash, too.

Take the case of Europe, where the entire yield curve of countries like Germany and Netherlands is trading at subzero levels, and in even the socialist dystopia of France yields up to 15-years are negative and even its 50-year debt trades at only 0.81%.

Self-evidently, the ECB manic bond-buying, which now amounts to $3 trillion just since 2015 and according to Draghi is fixing to restart after finally pausing only in December, has basically crushed investment grade yields in the Eurozone. There is actually more than a dozen junk bonds trading at subzero, as well.

Yet Mario Draghi recently had the gall to insist that ultra loose monetary policy and NIRP are,

……… “not the problem, but a symptom of an underlying problem” caused by a “global excess of savings” and a lack of appetite for investment……This excess — dubbed as the “global savings glut” by Ben Bernanke, former US Federal Reserve chairman — lay behind a historical decline in interest rates in recent decades, the ECB president said.

Nor did Draghi even bother to blame it soley on the allegedly savings-obsessed Chinese girls working for 12 hours per day in the Foxcon factories assembling iPhones. Said Europe’s mad money printer, Europe also has the disease and when it comes to the savings glut,

The single currency area was “also a protagonist…….”

Actually, that’s a bald faced lie. The household savings rate in the eurozone has been declining ever since the inception of the single currency. And that long-term erosion has continued on a downward trend line ever since Draghi issued his “whatever it takes” ukase in August 2012.

To be sure, double-talking central bankers like Draghi slip in some statistical subterfuge, claiming “current account surpluses” are the same thing as “national savings”.

Actually, they are nothing of the kind; current account surpluses and deficits are an accounting identity within the world’s Keynesian GDP accounting schemes, and for all nations combined they perforce add to zero save for statistical discrepancies.

In fact, current account surpluses and deficits are a function of central bank credit and FX policies and their impact on domestic wages, prices and costs. Chronic current account surpluses result from pegging exchange rates below economic levels and thereby repressing domestic wages and prices, and chronic deficits from the opposite.

Stated differently, what central bankers claim to be “excess savings” generated by households and businesses, which need to be punished for their sins, are actually deformations of world trade and capital flows that are rooted in the machination of central bankers themselves.

That much is evident in Draghi’s own numbers. He chides Germany and the eurozone for fueling the savings glut as represented by 5% and 3% of GDP current account surpluses, respectively. But that’s a case of the pot calling the kettle black, if there ever was one.

During the 14 years before Draghi’s mid-2012 “whatever it takes” ukase, which meant that he was fixing to trash the then prevailing exchange rate of 1.30-1.40 dollars per euro, the eurozone did not have a current account surplus. The surplus has only emerged beggar-thy-neighbor style since Draghi trashed the currency.

What Draghi cites as the problem—a current account surplus—that he is fixing is mainly his own creation!

That is, it is a result of the 20% currency depreciation the ECB effected under his leadership, and also the temporary improvement in Europe’s terms of trade owing to the global oil and commodities glut. And even in the latter case it is central banker action that originally led to the cheap credit boom of the last two decades and resulting worldwide over-investment in energy, mining, manufacturing and transportation capacity.

In any event, the eurozone surpluses since 2011 shown below do not represent consumers and business failing to spend enough and hoarding their cash. To the contrary, these accounting surpluses are just another phase of the world’s massively deformed system of global trade and capital flows. The latter, in turn, is the fruit of a rotten regime of central bank falsification of money and capital markets.

In fact, when savings are honestly measured, there is not a single major DM economy in the world that has not experienced a severe decline in its savings rate over the last several decades. The Canadian household savings rate, for example, has literally dropped rate off the charts, and now stands at just 1.1%.

Likewise, Japan’s much vaunted high saving households back in its pre-1990 boom times have literally disappeared from the face of the earth. Yet this baleful development occurred just when Japan needed to be building a considerable savings nest egg for the decades ahead when it will essentially morph into a giant retirement colony.

The deep secular decline of household savings rates throughout the DM world is in itself the tip-off that central banks have drastically deformed the financial system, and are now telling the proverbial Big Lie about a phony “savings glut” in order to justify their continued savage assault on depositors. That’s because under any historical rule of sound money, the kind of investment boom experienced by the EM world during the last two decades would have been accompanied by the upsurge of a large savings surplus in the DM economies.

During the great global growth and industrialization boom between 1870 and 1914, for example, Great Britain, France, Holland and, to a lesser degree, Germany were huge exporters of capital. By contrast, the emerging markets of the day——the United States, Argentina, Russia, India, Australia etc.——-were major capital importers.

That made tremendous economic sense. The advanced economies of the day earned trade surpluses exporting machinery, rolling stock, steel and chemicals and consumer manufactures, and then reinvested these surpluses in loans and investments in ships, mines, railroads, factories, ports and public infrastructure in the developing economies.

The lynch-pin of this virtuous circle, of course, was common global money. That is, currencies that had a constant weight in gold, and which, accordingly, were convertible at fixed rates over long stretches of time. English investors and insurance companies, for example, invested in sterling denominated bonds issued by foreign borrowers because they knew the bonds were good as gold, and that their only real risk was borrower defaults on interest or principal.

Today’s world of printing press money has turned the logic of gold standard capitalism upside down. Accordingly, during the last several decades the east Asian manufacturers and petro-economies have purportedly become varacious savers and capital exporters, while the most advanced economy on the planet has become a giant capital importers. Indeed, Keynesian economists and so-called conservative monetarists alike have proclaimed these huge, chronic US current account surpluses to be a wonderful thing.

No it isn’t. Donald Trump is right—–even if for the wrong reason.

The US has borrowed approximately $8 trillion from the rest of the world since the 1970’s not pursuant to the laws of economics, as the Keynesian/monetarist consensus proclaims. Instead, the unbroken string of giant current account deficits shown below——-the basic measure of annual borrowing from abroad——were accumulated in violation of the laws of sound money; and were, in fact, enabled by Richard Nixon’s abandonment of the dollar’s convertibility to a fixed weight of gold in August 1971.

In any event, even the EM economies are not giant excess savers, as Keynesian propagandists currently argue. The Red Ponzi, for example, has run its printing presses at warp-speed for more than a quarter century. This plucked from thin air central bank credit, in turn, fueled a massive spree of domestic industrial, infrastructure and housing investment, which reached freakish extremes at upwards of 50% of GDP.

In the Keynesian GDP accounting scheme, of course, that made it appear that the hundreds of millions of Chinese workers who were being flushed from the rice paddies into China’s spanking new factors where they worked for a few dollars per hour or even less, where actually gluttonous savers.

Yet that’s an accounting illusion. When China massive mountain of debt grew from $2 trillion to $40 trillion during the last quarter century, the first round GDP effect was ultra high investment spending and off-setting business profits and household wages on the income side of the GDP ledgers.

But once removed, that “income” merely reprsented the conversion of central bank credit and the soaring bank loans it enabled into cash flow; in ordinary economic terms, it was “printed”, not earned.

That is to say, stop the Red Ponzi’s massive annual borrowing spree and investment would plummet. In turn, incomes (especially corporate profits and wages in the factory, housing and infrastructure sectors) would tumble and the illusion of high “savings” rates in the GDP accounts would essentially evaporate.

China’s Central Bank Balance Sheet Has Increased by Nearly 10X Since The Year 2000

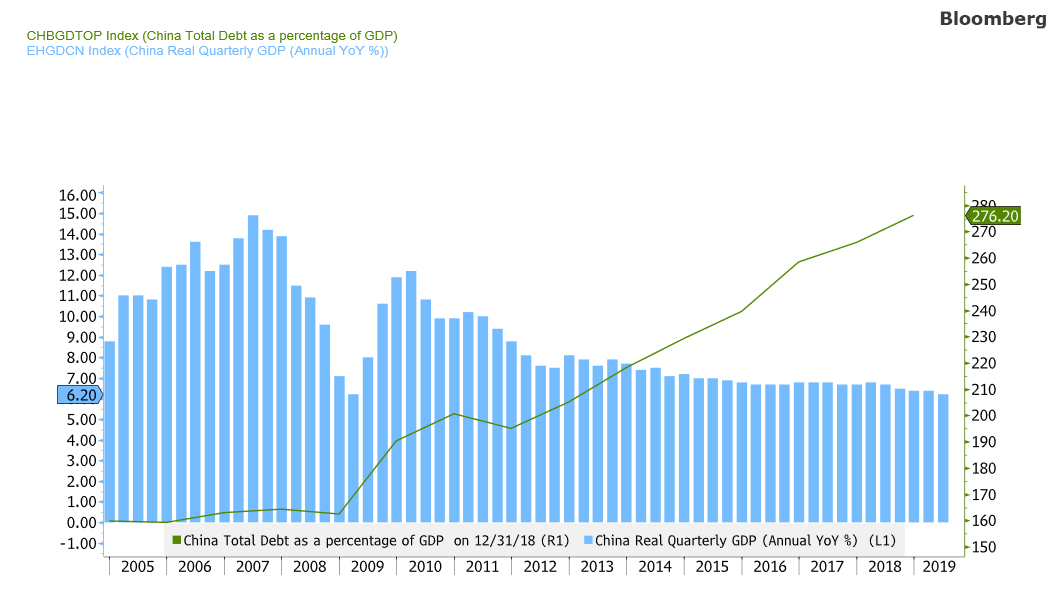

The truth is, the end game of the so-called savings glut is already coming into view in the Red Ponzi. As shown below, the debt and investment driven growth rate (flow) is steadily falling, even as the stock of debt (green line) relative to GDP climbs ever higher.

Undoubtedly, China extended period of debt driven investment growth allowed it to print superior GDP growth numbers. But those numbers were not indicative of historically unprecedented savings glut in a backwards developing economy. The chart only tracks the greatest (and most unsustainable) economic Ponzi in recorded history.

Indeed, if the workers of China were really gluttonous savers, why would they be borrowing hand-over-fist?

Yet in just in the last 15 years, the debt-disposable income ratio has nearly quadruped.

Soaring Chinese Household Debt Ratio

The truth is, there is no savings glut in the world whatsoever. Instead, there is a massive glut of central bank driven distortions and price falsifications in the financial markets that have resulted in the absurdity of 100-year Austrian bonds trading at 187% of par.

And that kind of “glut” is not the least bit comforting; it’s a flashing red neon sign warning that the egregious financial bubbles generated by Keynesian central bankers are nearing their sell-by dates.