By Tyler Durden at ZeroHedge

ROK: Better than CAT as a barometer of macroeconomic/industrial trends

All industrial equipment uses semiconductors, and ROK (Rockwell Automation) is the premier industrial automation focused semiconductor company.

Factories and mines are hostile environments: lots of dust, heat, chemicals, liquids and vibrations. Less than ideal conditions for delicate components like semiconductors. But increased automation means more semiconductors, and ROK specializes in making hardy components.

ROK as best barometer

- Breadth of industrial customer base: hard to find a company that touches more capital intensive projects.

- Upstream in the demand chain: ROK demand comes in before CAT demand. In fact, that CAT extractor needed ROK chips

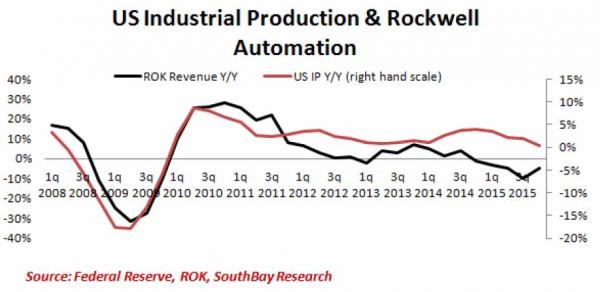

Correlation to US Industrial Production

ROK revenues strongly correlate to the US Industrial Production. That’s because much of the business is cyclical.

The advantage comes with ROK’s forward guidance: it’s 1:1 with developments in the manufacturing space and with regional growth.

The latest data says: US is deteriorating rapidly and so is China.

Latest Earnings: Bad News

Nothing pretty on today’s earnings call

3QCY Revenue dropped (-10%)

FY2016 Sales guidance lowered to -4% y/y

“As we progressed through the quarter, conditions softened. And September was especially weak, particularly in the U.S. product businesses….September typically is the strongest month of the year.”

– Keith Norbusch, ROK CEO

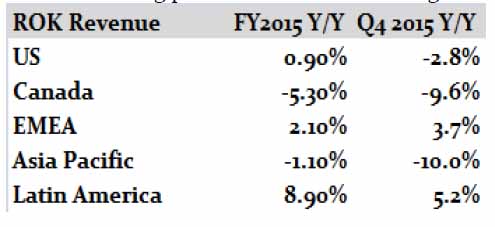

- Canada, Latin America, US: Exposure to commodities is the general trend. The pace and timing of the slowdown reflects the lag in capital intensive projects. This means that the worst has not hit yet and the pain will continue at a faster pace into 1Q 2016.

- Asia Pacific (aka China): Collapse.

- EMEA: Good news as signs of a bottom are in place. Maybe.

Forward Guidance

“There appears to be a general slowdown in U.S. industrial customer spending, both capital and operating spending”

– Theodore Crandall, ROK CFO

Secular trends remain healthy (industrial growth continues) but near-term customers are pushing out spending. And there is no visibility.

Our view: producers are still adapting to China’s real level of demand.

At this stage, small cuts in spending (CAPEX & OPEX) until we get to 1Q 2016 and clearer visibility to Chinese demand. This is driving poor visibility.

When does it change? MAYBE in 12 months. Maybe. And that’s based on nothing but hope. There is no customer ordering or data that ROK uses to base their 2H 2016 call for improving conditions.

“we’re not expecting to see sequential growth until the second half of the year (2016)”

– Theodore Crandall, ROK CFO

Every manufacturer is looking at two options.

- Plan A: Hold steady. Stop hiring, stop CAPEX

- Plan B: Cut CAPEX, Cut Payrolls, Cut Orders

Plan B is ready to go starting in January, pending customer order outlook.

The silver lining:

Per the ROK CFO, weaker sales means lower commissions, which equals a margin and EPS tailwind! (That was actually said on the earnings call.)

Goodbye wage inflation.

Source: The Most Important Earnings Report You Should Know About – ZeroHedge