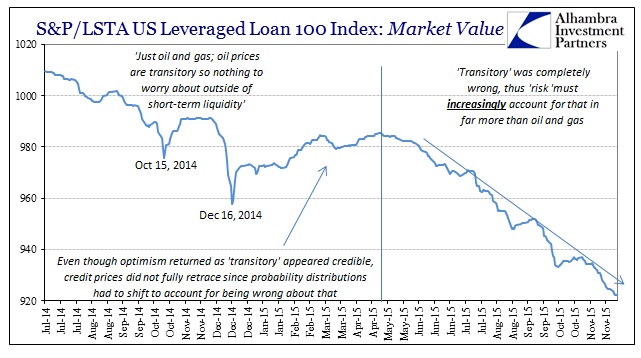

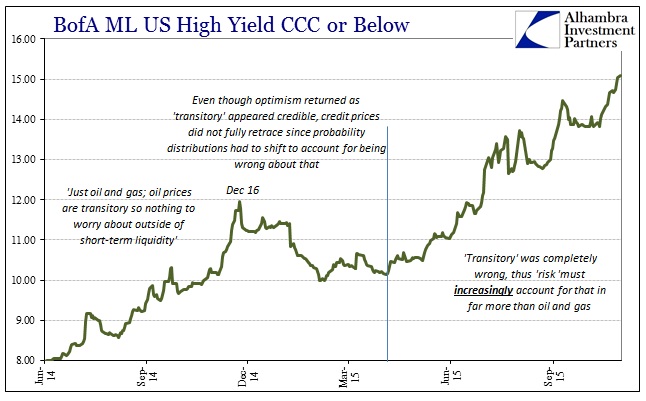

On December 11, 2014, spot WTI closed at $60.01, down sharply from $76.52 the week before that Thanksgiving. In the space of only a few weeks, oil prices had collapsed far more than anyone thought possible; and yet there was very little urgency to the outcome. Economists, in particular, parroted throughout the media, were quick to assert both a supply “glut” as well as how very beneficial low oil prices were in macro terms for consumers. Paradoxically, Janet Yellen’s increasing use of the word “transitory” meant that on one side the decline in oil prices wasn’t meant to last even though on the other that meant the consumer “benefit” would not either. Thus, in orthodox terms it was better that oil prices would return to oppressive levels and therefore any consumer aid was just the silver lining for the interim.

The word “transitory” would define, then, not just oil prices themselves but an entire array of market balances and economic interpretations that come from oil being the economic center of even a services economy. In terms of assets, junk and high yield corporates were uniquely bombarded by the “unexpected” oil crash, leaving many investors to lighten up in what was a great shift in probabilities and perceptions – better to sell a little just in case Yellen got it wrong.

Even though oil fell below $50 spot WTI as soon as January 6, 2015, and then even flirted with the $30’s not long after, by the middle of the year WTI was back above $55 and even intermittently in the very low $60s. For many, far too many, that seemed as if Yellen had it right and that junk bonds were being overly cautious even when the prior year’s selloff (to December 16) was being limited in commentary to just the oil sector. By mid-year, oil and gas were back within the dominant narrative:

Fear has given way to greed in risky US energy bonds. After last year’s oil crash pummelled the US energy industry and sparked fears over a slew of corporate defaults, yield-hungry investors have returned to pick up bargains from the detritus.

As oil prices stabilised around the $50 per barrel mark, and prospective returns on other corporate debt — let alone government bonds — have remained paltry, investors have become somewhat more positive.

That was published in April and contained, despite the more optimistic tone, a rather stark warning about those probability distributions that were tested at the outset of this year:

While US junk bonds are on the whole attractive, “energy bonds still look too rich”, argues James Swanson, chief investment strategist at MFS, which manages about $445bn. “Many of these companies cannot outlive a two-year bear market [in oil].”

As with macro themes, the narrative would shift only in the smallest possible increments. In the middle of 2014 there was nothing but clear sailing for anything and everything; by the start of 2015, it was still a great environment but now with a little trouble limited to the oil and gas sector. Despite everything that has occurred since then, that remains the conventional association of junk and corporate debt that gets more and more pummeled by the day – don’t worry, it’s only oil.

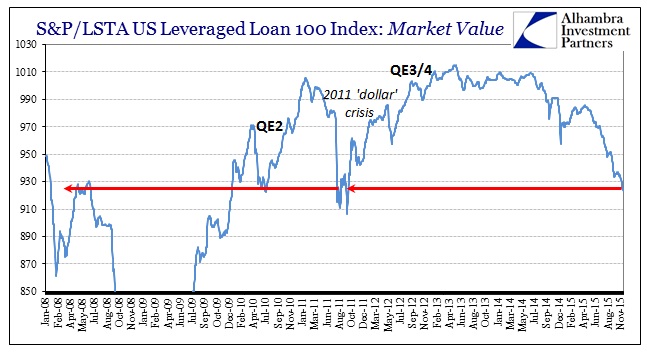

It is becoming much more difficult to argue as such with the junk bubble being pared back now to comparisons with 2011. Thus, at this belated point, convention is once more being altered by market prices and the “dollar” reality that pushed them. Reluctantly, oil is being more and more written off (goodbye to “transitory”) while the “risk probability” re-evaluation is now being forced deeper into the fuller corporate space.

While the pain in the junk bond sector has been concentrated in commodity linked industries — junk-rated metal and mining, independent energy and oilfield services paper have fallen by more than a tenth this year — other areas of the market have also come under pressure, including aerospace and defence, pharmaceuticals and chemicals companies.

“The flight from energy and the reluctance to step back in even at today’s highly distressed levels among investors has been stark,” says Michael Contopoulos, a strategist with BofA Merrill Lynch. “Even the erstwhile ‘safer’ places to hide may not make the cut going forward.”

The internals of the junk market are atrocious and getting worse on a widespread basis, with spreads blowing out in almost every sector:

The average bid of LCD’s flow-name high-yield bonds fell 132 bps in today’s reading, to 89.03% of par, yielding 10.58%, from 90.35% of par, yielding 10.05%, on Nov. 19. Performance within the 15-bond sample was deeply negative, with 12 decliners against two gainers and a lone constituent unchanged.

Today’s decline is a seventh-consecutive observation in the red, and it pushes the average deeper below the previous four-year low of 91.98 recorded on Sept. 29. As such, the current reading that has finally pierced the 90 threshold is now a fresh 49-month low, or a level not seen since 87.93 on Oct. 4, 2011…

As for yield in the flow-name sample, the plunge in the average price—with many names falling into the 80s and a couple of others more deeply distressed—has prompted a surge in the average yield to worst. Today’s gain is 53 bps, to 10.58%, for a 2.92% ballooning over the trailing four week. This is a 13-month high and level not visited since 10.70% recorded on June 10, 2010.

The average option-adjusted spread to worst pushed outward by 47 bps in today’s reading, to T+791, for a net widening of 167 bps dating back four weeks. That level represents a wide not seen since the reading at T+804 on Sept. 23, 2010. [emphasis added]

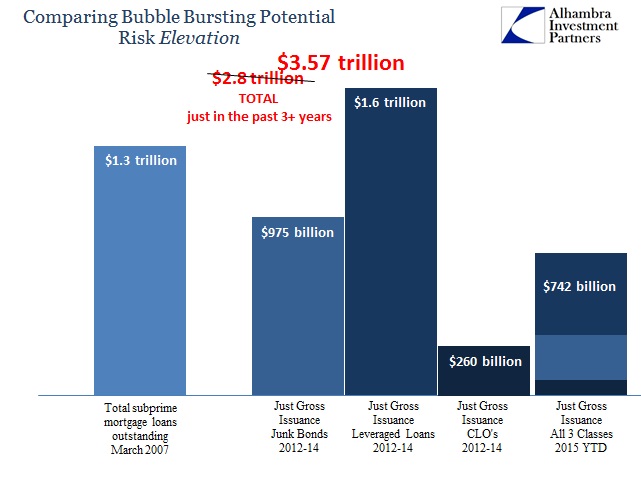

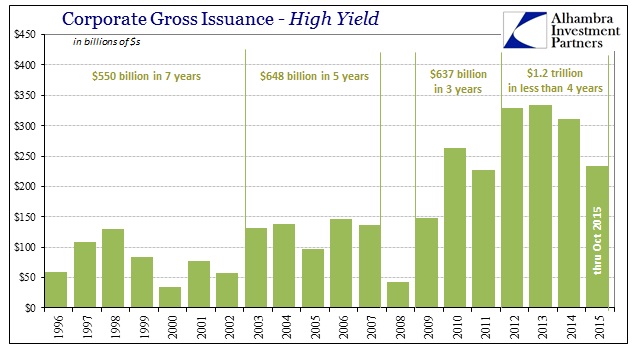

This deeper contraction in risk positioning and liquidity is actually understated by a huge degree. Prices and spreads might be comparable to 2011 and 2010, and even, now, early 2008, but that doesn’t account for the huge gross balloon in issuance since 2012 and especially QE3. Between 2009 and 2011 (inclusive), cumulative gross issuance for just junk bonds was about $640 billion. From 2012 through October 2015, cumulative gross was $1.2 trillion. Not only was issuance almost double, the prices and spreads for all that volume were absorbed by the “market” at increasingly lower levels.

Unfortunately, that imbalance works, as always in credit cycles, beyond simply junk and high yield. Investment grade corporate issuance, gross, was $2.3 trillion for 2009, 2010 and 2011, while $4.3 trillion 2012 and forward. Again, that huge increase was floated at increasingly more “reach for yield” price depredation. As even IG spreads have risen this year, particularly in July and August, that supplies price and funding pain far and wide (stretching into much deeper wholesale factors that most cannot fathom). There is increasingly very little margin for error in both liquidity/funding terms and as an economic account.

In that respect, oil and gas were simply the leading edge of what is becoming a universal distaste. But since junk is quite illiquid in pricing, that leaves the system quite vulnerable to these kinds of narrow windows; only a smattering of tradable issues are used to set proxy prices for whole swaths of more hidden but ballooned volume of this “stuff.” While commentary may try to assure itself that it is “just oil and gas”, spread decomposition holds no such luxury and thus has to account for that sector, too. That leaves invisible prices under modeled constraints “forced” to adjust to even the oil and gas sector’s liquidity variant and now risk parameters; in other words, the liquidity “premium” being “charged” to higher spreads in oil and gas becomes more and more the setting for spread variables in other industries even if there isn’t an immediately outward increase in risk.

That is why, along with “dollar” liquidity, there is no “bargain hunting” past July in stark contrast to the prior pattern.

The problem for all these other non-energy industries is thus quite obvious in November 2015 when “transitory” has so spectacularly failed. Simple extrapolation reveals that risk given that the same reassurances issued more broadly by economists and policymakers. Further, economic risks have, in fact, increased especially after August, which means altering positional behavior even where asset managers and funding firms still believe macro risks minimal (no recession). In short, you don’t have to believe in the worst downside to begin adjusting allocations and margin (both funding and safety) because you have to now assume a greater probability of being wrong – just like oil and gas already is and has been.

With “reach for yield” perpetrating a stretched boundary for absorbing such a reversal, any such shift is asymmetric and almost immediately self-reinforcing. Throw in the avalanche of gross issuance and the cascade pushes beyond reach. The behavior of junk prices in November suggests perhaps exhibiting beyond that point. In total, then, junk bonds are not just a limited and temporary problem but a widespread and still growing problem with broad macro and market implications. After all, where did all those trillions go on either side (liability in terms of corporate uses; asset in terms of who is holding the bag) of the ledger?

The difference here with continued complacency and the ability to abjectly ignore the disruption is just that visibility. At the end of the housing bubble everybody knew it was happening because it was everywhere, even to the point that banks were forced to display it in ongoing write-downs. Economists were then as now downplaying the significance because that is what they do; their models are literally (mathematically) incapable of examining even the possibility of inflection. In this junk bubble, which is much larger in terms of actual size and, more importantly, penetration (the public actually owns a great and direct share of this junk via ETF’s and mutual funds vs. the subprime disaster which was almost exclusively institutional and thus indirect), there has yet to be an open breakout of defaults and visible losses. However, these junk prices and especially the trajectory of them in 2014/2015 prefigure that reassurance in increasingly limited application.

The junk market has already come to grips with a much worse fate than is appreciated even by those charged with examining it. As is plain from any such inspection shorn of orthodox tendencies, the trends are not in any way related to monetary policy nor the mainstream economic interpretation that supposedly runs it. They are, in fact, increasingly, violently emphatic in the contrary. As WTI prepares to end 2015 as it started, with oil spending almost the whole time at or near $40, these huge markets have already turned toward, and priced, the suddenly fertile ground for what else Janet Yellen has wrong.