Back in January and even into February, the idea of recession seemed no longer so far-fetched. The FOMC and orthodox economists had been claiming since late 2014 that the only economic fate was “full employment” and the satisfying economic conditions that accompany it. Instead, the latter half of 2015 turned uncomfortably close to the “impossible” nightmare scenario. What was totally unrealistic by 2014’s standards was suddenly very, very real and quite close.

Then as quickly as it seemed to rush on, markets abruptly shifted and the world suddenly appeared much less dark. Having flirted with recession and escaped that fate, the mainstream assumes that “it” is all over and that prior expectations should only resume. The message now is that it was far too close for comfort, but thankfully it is now all in the past.

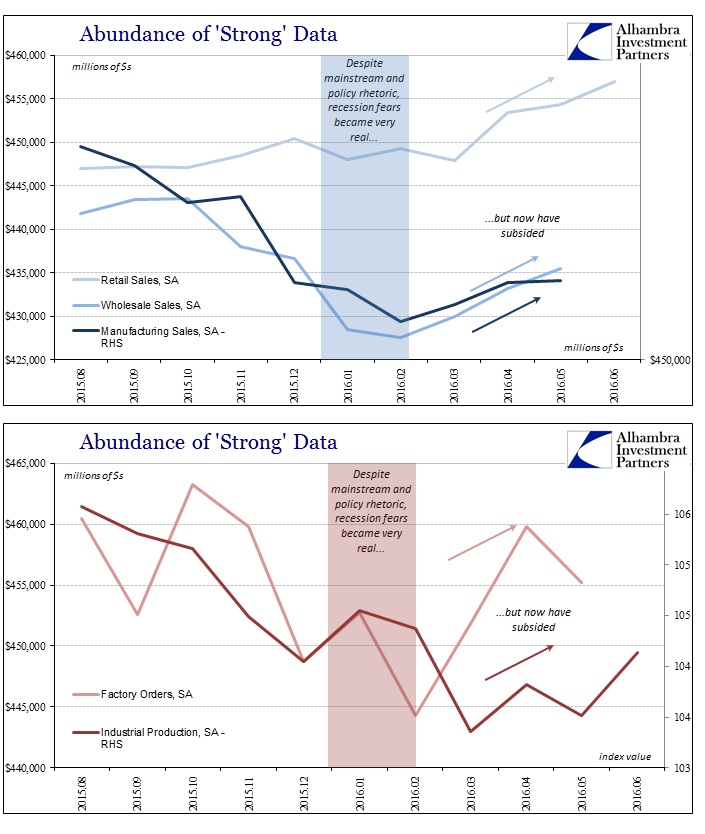

This binary arrangement has clearly colored recent analysis, and as such it has led to really unhinged commentary. Bloomberg reports today that the dollar index is rising again as currency markets reassess the Fed’s potential stance in light of “strong data.” The most recent updates in economic accounts, according to Bloomberg, suggest that the US economy is “set to continue to expanding.” If it isn’t recession, all must be well.

“There’s certainly a growing crowd of investors that are warming up to the notion that the abundance of strong U.S. economic data may light a fire under the Fed and lead to a surprise rate hike by year-end,” Stephen Innes, a senior trader at Oanda Corp. in Singapore, said in an e-mailed note.

You can understand the basis for it only somewhat, but “abundance of strong U.S. economic data” is pushing very close to wishful blindness. There is no arguing that the US economy seems better than it was to start the year, but that is not in any way the same as “strong” anything. It can only come out that way under the narrowest of context, usually this binary assumption.

It is only under this most recent comparison that the possibility arises. The most that can be said is the US economy as of right now appears to have avoided the straight-line drop into recession. Extrapolating that into anything more, as economists do constantly, relies on outdated assumptions. But the impulse, which is tantalizing on its own, has been amplified this year because of the renewed presence of central banks and the rekindling of romantic notions about monetary policy. I wrote this morning (subscription required):

If there is a difference this year as opposed to the past two, it is perhaps that central banks are more active than they have been since 2012; and that includes rumors. That was the clear verdict of January/February as opposed even to last August. The market was deeply shaken and central bankers were shocked into becoming aware that they were losing credibility and their grip. They have responded. Markets, really “markets”, have, too, even though there is no reasonable basis to literally buy what central banks are selling – except emotion.

In addition, there is this seasonality at work that for now favors that emotion. The world in a slightly more tangible way seems much better than it was to start the year (just as 2015, 2014, 2011, etc.). But “better” is still a relative term; there is relief being expressed that what seemed like a possible recession in January has passed but that is the wrong analysis; the wrong type of analysis even. Being caught in the same economy and its repeating seasonality is not cause for relief and a burst of optimism, just as it wasn’t last year, and certain parts of the markets get that.

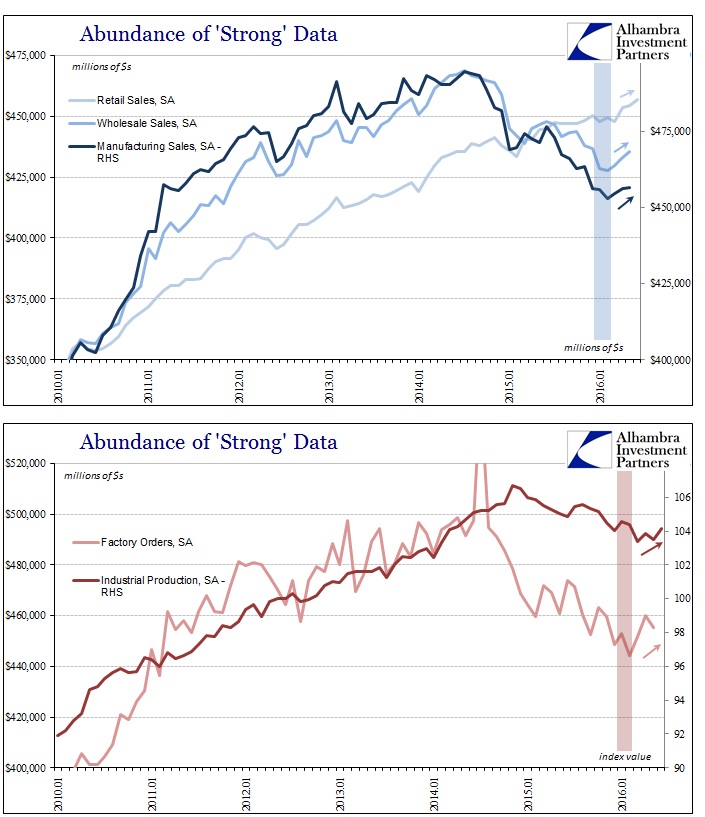

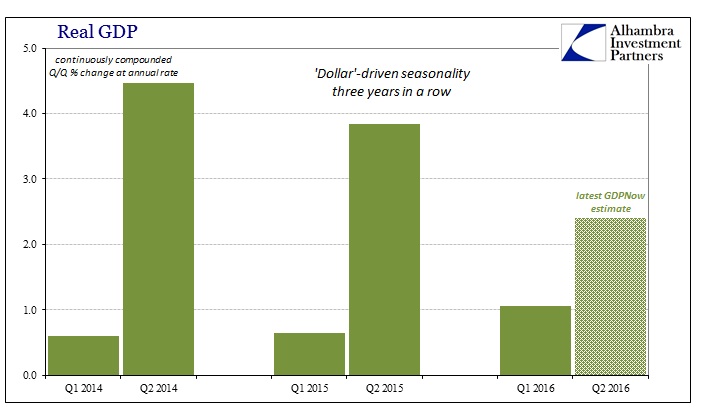

From any reasonable perspective, there is no “strong” data anywhere. The word is attached because of the selective comparison to earlier in the year plus the possibility of renewed monetary hope. Thus, the word “strong” is not actually derived from the data but rather the bias of the commentary using it (as if that was surprising). The binary question is irrelevant, as is (and has been) monetary policy.

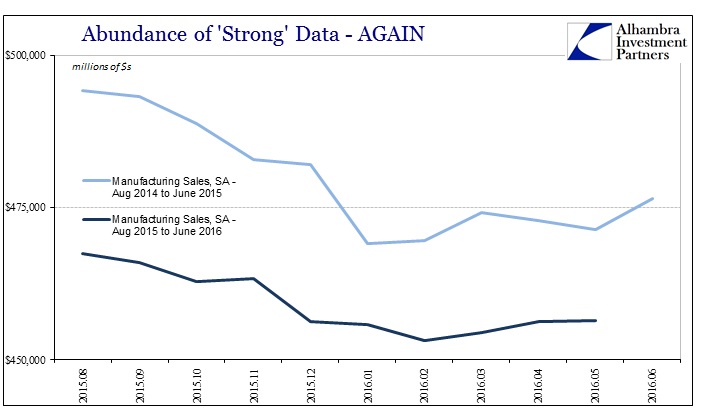

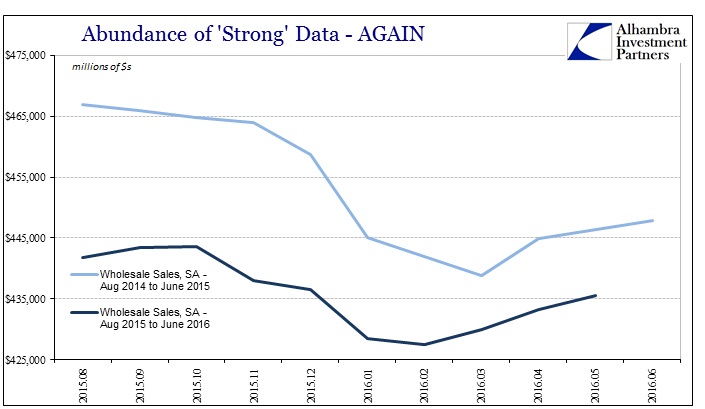

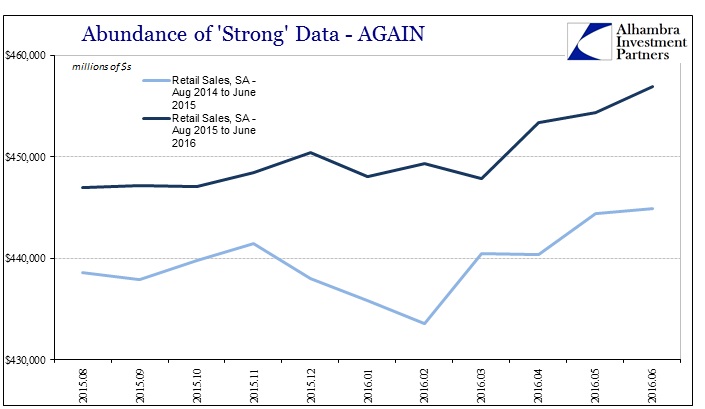

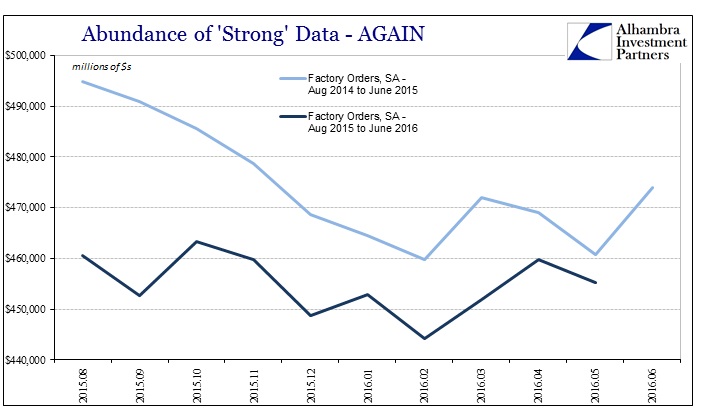

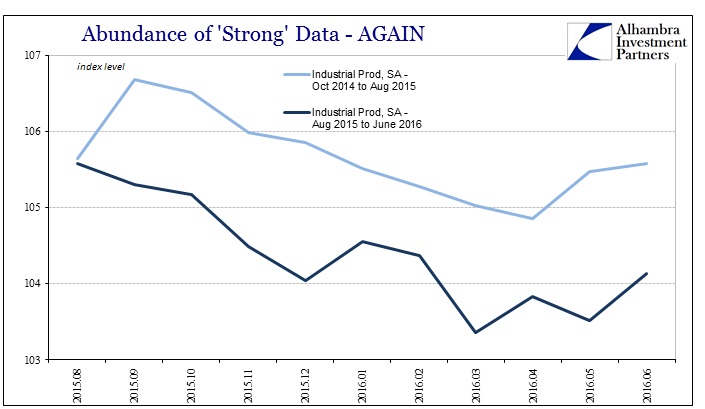

It is the same mistake that was made at this very same time last year. And indeed, we find repetition in all these same data series. Like 2016, 2015 started with shock and concern before yielding to “strong” data in the late winter and especially spring. That seasonality of last year has only been repeated, which does not argue against recession it only shows that the same economic trends that surprised and shocked late last year are quite likely still at work. From that perspective, the correct qualification for 2016 is not “strong” but “concerning” – that it would still happen again for the third year in a row.

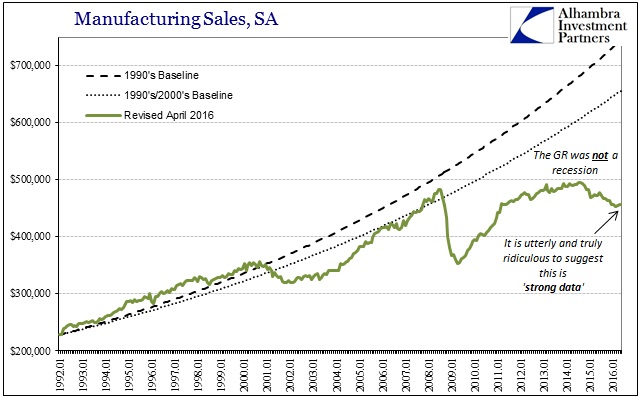

It is unstable growth more like stagnation, a term more suitably derived from wider, more appropriate context. The “strong” turnaround of 2016 fades very quickly in comparison to both the seasonal repetition and what the overall data actually indicates the past two years. There is very little positive here.

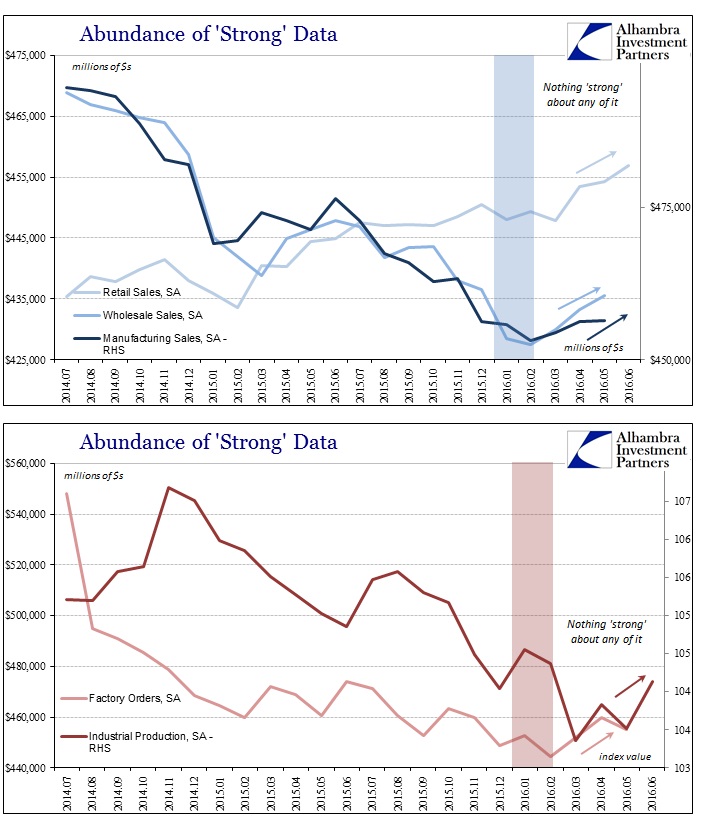

As hard as it may be to understand in orthodox terms, recession in late 2015 or early 2016 would actually have been a more hopeful outcome; at least that might have indicated some cyclical characteristics, suggesting at least the possibility of breaking out of this stagnation. Instead, it is quite clear that the economic conditions prevalent since 2011 and 2012 remain steadfast in their slow, steady and time consuming attrition/erosion.

These charts only demonstrate chronic malfunction, which is what this year’s renewed spring “rebound” confirms. Again, the only way the word “strong” can apply is if it is misapplied through emotion about central banking being more active this year. That is, however, not a view of the economy as it is, rather it is more of wishing for the economy as it “should be” – but never is. This view extends beyond the “goods economy”, as even statistics like GDP and the Establishment Survey are more like manufacturing accounts than is likely to be admitted.

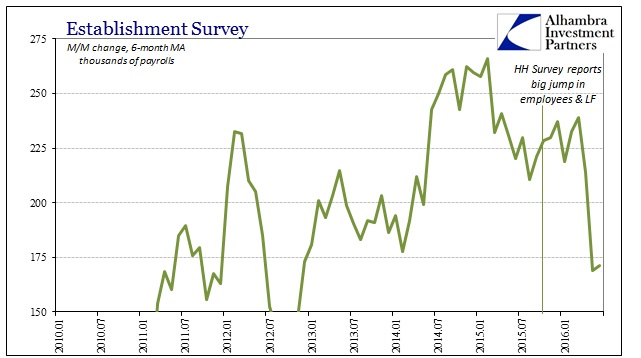

In terms of GDP, we don’t yet know what the first estimate for Q2 will ultimately be (that’s next week, pending also benchmark revisions) but as of right now the Atlanta Fed’s GDPNow model suggests 2.4%. That is more than double the 1.07% currently figured for Q1. While that might seem consistent with the idea of “better growth” ahead, it is instead more concerning from the more relevant context of “dollar”-driven seasonality. In other words, we have seen this same pattern now for three consecutive years, and each year the Q2 “rebound” actually gets smaller.

If the 2.4% guess for Q2 is close, that would mean 2016’s spring bounce back is only a little more than half of what it was in 2014 (when Q2 GDP jumped to nearly 4.5%) and down significantly from just last year. This view of GDP outside of the binary optionality is far more consistent with all the data included above from manufacturing and industry – the stagnation, instability in GDP terms, is getting worse not better.

The Establishment Survey would seem to agree even if the highly variable monthly headline was so much more emotionally satisfying for June than May. Overall, the trend in that particularly data point is also worse, not better.

The idea of “strong data” or even an economic turnaround itself is grounded only in misconception. It is the emotion of relief where there are only two economic settings – recession or not. Since the economy appeared to escape that fate in the spring, the driving assumption is that it is clear sailing from here, a hope further buoyed by the memory loss accompanying more active central banks.

Viewing the economy and all this data from the different perspective beyond traditional cyclicality leads to far different interpretations and expectations. The economy is not “strong” or even really rebounding; it is only still captured by contraction and stagnation of a variety increasingly distinct from recession and cyclicality. Under these terms, renewed monetary policy emphasis is not a source of hope but an expression of desperation. There is a great deal of that in the rush to call all of this an “abundance of strong data.”