Well…she did it. After eleven years of maintaining emergency rates in order to boost asset prices, valuations, speculative debt accumulation back to pre-financial crisis levels, Janet Yellen officially hiked rates this past week.

More interesting was that while banks are getting paid more on excessive reserves, and hiked the lending rates, they have not offered to share any of their new found income with savers. Of course, that revelation should not really surprise anyone at this point.

However, as I discussed earlier this week, there is a nagging question as to why they would raise interest rates at this late juncture in the economic cycle.

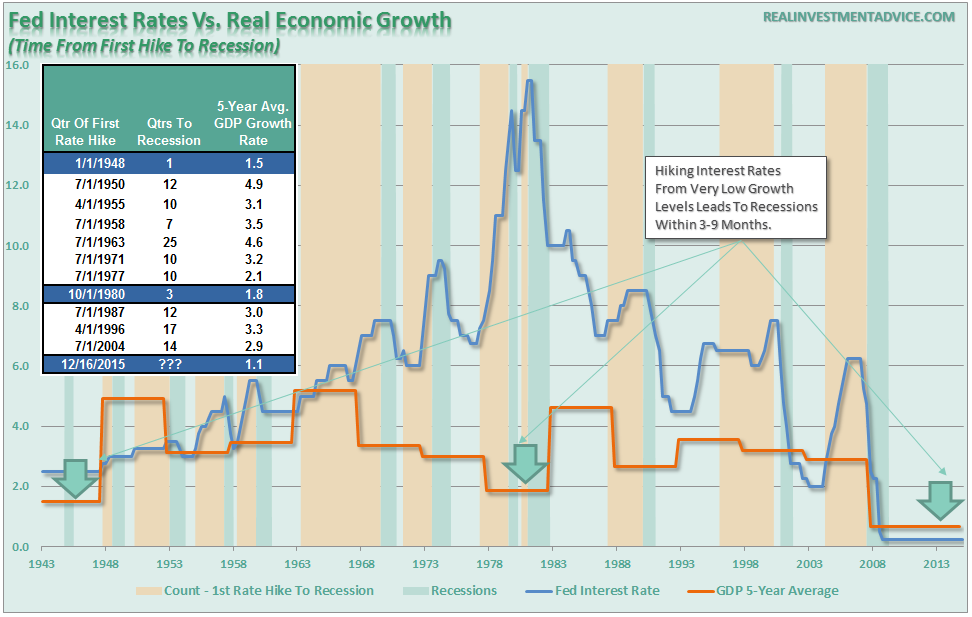

“With economic growth currently running at THE LOWEST average growth rate in American history, the time frame between the first rate and next recession will not be long.

However, as I have stated many times in the past, it is quite likely the Fed is already well aware that we are very late in the current economic cycle. For them, the worst of all possible outcomes is being caught at the “zero bound” of interest rates when the next recession begins which removes one of the more effective policy tools at their disposal.

For investors, there is little “reward” in the current environment for taking on excess exposure to risk assets. The deteriorating junk bond market, declining profitability and weak economic underpinnings suggest that the clock has already begun ticking. The only question is how much time is left.

This week’s reading list is a compilation of opinions on the Federal Reserve’s latest actions and the myriad of potential outcomes that are expected. How you choose will be very important, so choose wisely.

1) Yellen, You’re Nuts by Karl Denninger via Market Ticker

“The effective fed-funds rate has been running at 0.15% for a bit now. To ‘raise rates’ to 0.25% the net change in system liquidity required is about 60%.

This is math folks. It’s the reason The Fed has a monstrous balance sheet; they had to in order to influence rates the way they wanted to on the way down. But to reverse that policy you must unwind that which you did in exactly the same sort of fashion.

So how much does The Fed have to drain themselves? I don’t know and neither do they. But that they have to reduce the amount of the ‘overfill’ in the liquidity pool by some 60% isn’t conjecture, it’s arithmetic.

We’ll see if the EFF actually moves in coming days as they “desire” and where the drain comes from. But this much is certain: If the rate does move, the drain will have occurred somewhere.”

But Also Read: Fed Raises Key Rates by Binyamin Appelbaum via NY Times

2) Yellen Takes A Huge Gamble by Ambrose Evans-Pritchard via The Telegraph

“The global policy graveyard is littered with central bankers who raised interest rates too soon, only to retreat after tipping their economies back into recession or after having misjudged the powerful deflationary forces in the post-Lehman world.”

But Also Read: Fed Finally Raises Rates, Pent-Up Risks Emerge by Greg Ip via WSJ

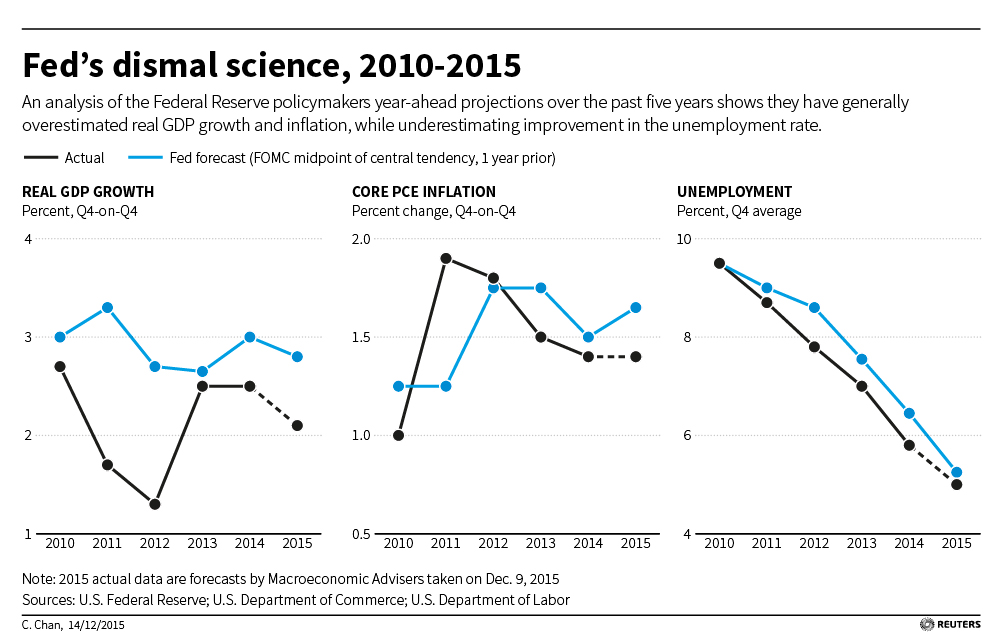

3) Overoptimistic Fed Strains Credibility On Forecasts by Lindsay Dunsmuir via Reuters

“But Fed policymakers have a mixed record in predicting the nation’s economic health, casting doubt on their ability to set a rate path that will keep one of the longest-running yet most anemic recoveries in modern history on track.

An analysis of the rate-setters’ year-ahead projections over the past five years shows they have generally overestimated real GDP growth and inflation, while underestimating improvement in the unemployment rate.”

But Also Read: A Fight For The Soul Of The Fed by Jeff Spross via The Week

4) Rate Hike Marks Start Of Correction by Michael Gayed via Market Watch

“Several signs are flashing red, indicating that a correction may be about to begin just as the Fed begins hiking rates. The zero-interest-rate policy has created massive distortions and a surprisingly large number of false positives when tracking historically proven leading indicators of corrections and volatility.

Perhaps the time has come for the bull market in risk management to make a comeback as the Fed slowly takes the punchbowl away. Regardless of one’s opinion, quantitative inter-market relationships which over time have shown their worth are signaling to watch out.”

But Also Read: How The Fed Just Launched The Next Bear Market by Tyler Durden via Zero Hedge

5) Rate Hike And The Potential For Recession by Edward Harrison via Credit Writedowns

“So let me give you a scenario here. In an environment in which earnings are shrinking and oil prices are declining, capital investment gets cut. And then the question becomes how much residential investment and consumer consumption growth can overcome this factor.

In a Goldilocks scenario low rate lock-in behavior causes borrowers to pull forward their borrowing decision, pushing up credit growth while the energy sector works through its malaise and the baton is passed to wage growth to do the heavy lifting of maintaining consumer spending . That’s what the Fed hopes will happen.

In a worst case scenario, the real economy effects of the oil sector and the earnings slowdown hit the frothy commercial real estate and REIT sector, which in turn begin the widening of the contagion begun by energy high yield. Combine this with the sudden stop to lower quality energy credits I believe is inevitable and you likely have stall speed – or even recession. And that’s where subprime auto ABS, student loan securitization and US munis come into the picture for the US domestic economy. Those markets get hit in recession.”

But Also Read: Rate Hike Will Help The Economy by Drew Greenblatt via Inc.

MUST READS

- Record Outflows Slam Debt Funds by Tyler Durden via Zero Hedge

- The Collapse Of The Galactic Economy by Jed Rosenberg via Bloomberg

- The US Has A Serious Start-up Slump by Robert Samuelson via Real Clear Markets

- Every Central Bank Has Regretted Hiking Rates by Matt O’Brien via The Atlantic

- Paul Ryan Throws In A $1.1 T Towel by Stephen Bannon via Brietbart

- Seven Thoughts On The Markets by Axel Merk via Aleph Blog

- Unintended Consequence Of Negative Rates by Wolf Richter via Wolf Street

- The Fed’s Real Policy Error by John Hussman via Hussman Funds

- Is This A Replay Of 2008 by Paul La Monica via CNN Money

- When The End Of The Bubble Begins by David Stockman via Contra Corner

“Where are the customer’s yachts?” – Fred Schwed, Jr.

Question, comments, suggestions – please email me.

Lance Roberts

Lance Roberts is a Chief Portfolio Strategist/Economist for Clarity Financial. He is also the host of “The Lance Roberts Show” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, and Linked-In