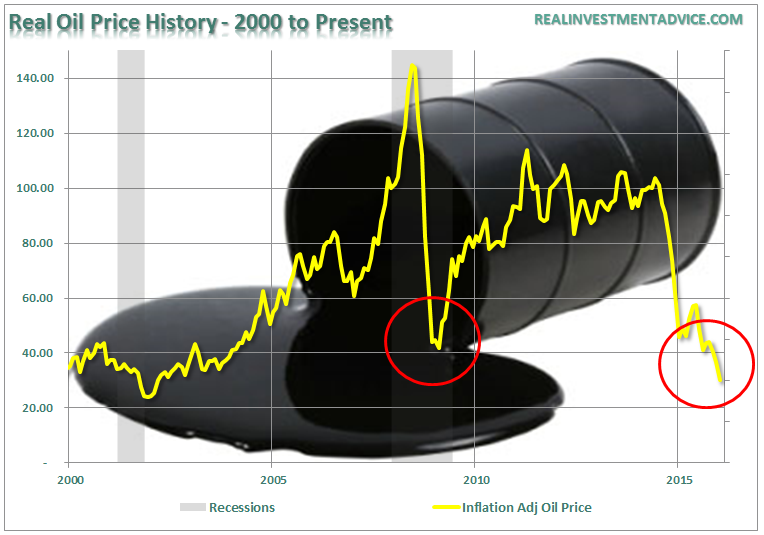

There is much hope in the financial markets, with individual investors and oil company employees that oil prices will rise in the months ahead. Many point to the 2008 commodity crash as THE example as to why the oil price decline is likely temporary.

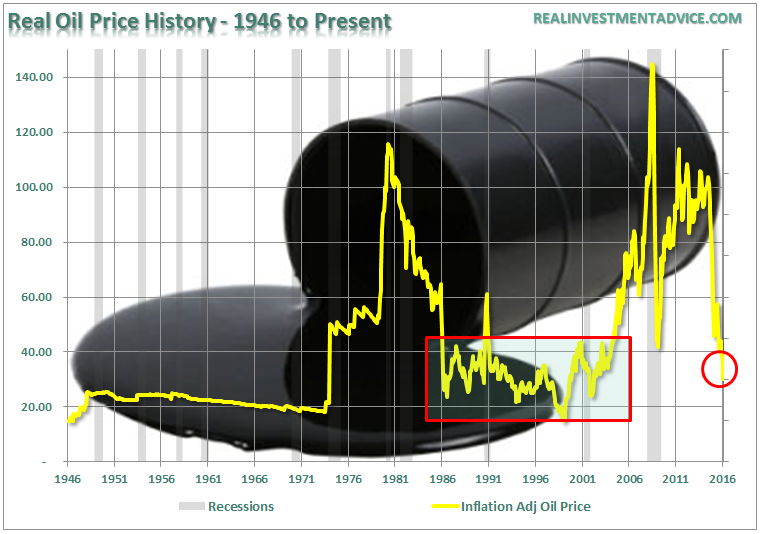

However, if we look back further in history we see another situation where the crash in commodity prices marked an extremely long period of oil price suppression.

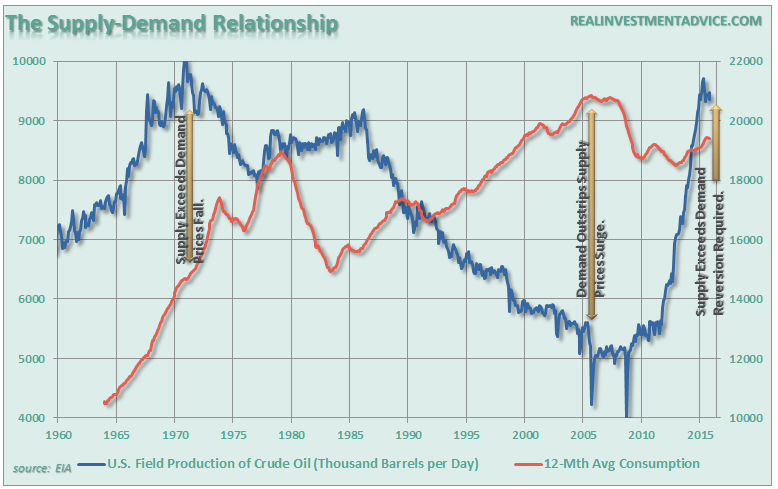

What was the difference? It was the supply to demand imbalance.

In 2008, when prices crashed, the supply of into the marketplace had hit an all time low while global demand was at an all-time high. The fears of “peak oil” were still a recent memory as the financial crisis took hold pushing prices to the lowest levels seen in years.

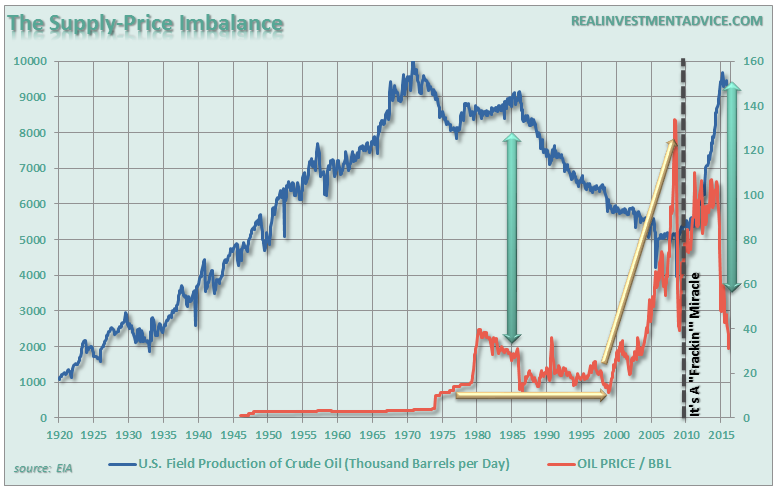

This supply-demand imbalance, combined with suppressed commodity prices, was the perfect cocktail for a surge in prices as the “fracking miracle” came into focus. The surge of supply alleviated the fears of oil company stability and investors rushed back into energy-related companies to “feast” on the buffet of accelerating profitability into the infinite future.

Banks also saw the advantages and were all too ready to lend out money for drilling of speculative wells. As investors gobbled up equity shares, the oil companies chased ever potential shale field in the U.S. in hopes to push stock prices higher. It worked…for a while.

The problem is now the supply-demand imbalance has reverted. With supply now back at levels not seen since the 1970’s, and demand waning due to a debt-cycle driven global economic deflationary cycle, the dynamics for a sharp rise in prices in the months to come is unlikely.

However, this is just assuming that current supply remains status quo. The problem, as I have discussed in the past, is that while the U.S. is curtailing CapEx and some production, it is being offset by production from China, Russia, and now Iran. According to the NYT:

“And yet, after many Western sanctions against Iran were lifted over the weekend, Iranian oil officials said they would quickly be ramping up exports by 500,000 barrels a day. Iranian production has been about 2.9 million barrels a day, with much of that oil sold to customers in Asia. Iran also consumes a lot of its crude domestically.”

The NYT goes on to address the problem with demand.

“One big uncertainty is how demand for oil will fare. Slowing growth in China has been a factor in falling demand. And the recent turmoil in the financial markets that began in China but that has spread globally has raised questions about whether underlying economic weakness around the world could become worse — with even growth in the United States beginning to slow.”

The supply-demand problem is not likely to be resolved over the course of a few months. The current dynamics of the financial markets, global economies and the current level of supply is more akin to that of the early-1980’s. Even is OPEC does reduce output, along with the U.S., it is unlikely to rapidly reduce the level of supply currently. Since oil production, at any price, is the major part of the revenue streams of energy-related companies, it is unlikely they will dramatically gut their production in the short-term. Therefore, it is quite likely that low oil prices are likely to be with us for quite some time.

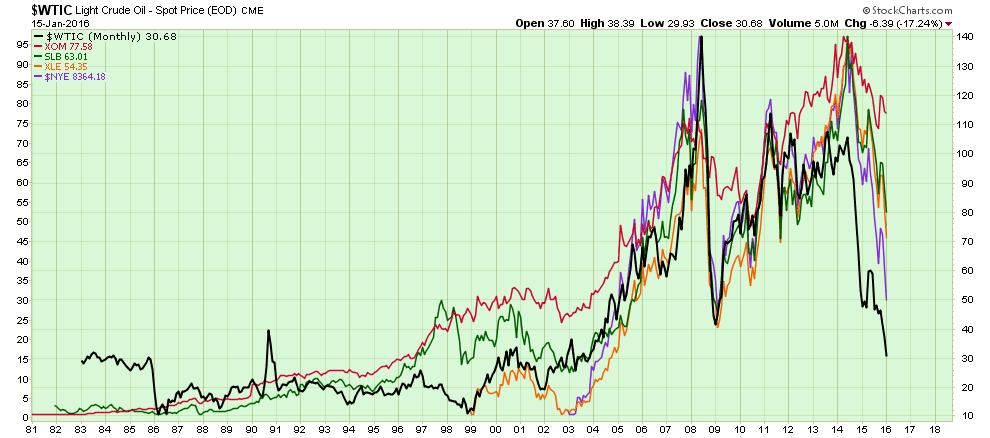

As shown in the chart below, the correlation between oil companies and the commodity price have become extremely correlated since the turn of the century. (I have used XOM and SLB as a proxy for refiners and drillers going back to the early 80’s. XLE is added for recent history)

It is quite likely that oil prices will eventually stabilize in the $30-40 range as the markets come to grips with recent volatility. From that point, the markets will likely shift their focus to supply glut and what that entails for the future.

From an investment standpoint, energy companies will likely present a good opportunity at lower price levels in the not so distant future. However, investors should realize that forward returns may return to more muted levels as supply continues to weigh on prices and profitability in the future.

Just something to consider.

Lance Roberts

Lance Roberts is a Chief Portfolio Strategist/Economist for Clarity Financial. He is also the host of “The Lance Roberts Show” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter and Linked-In