Friday’s Wall Street Journal headlines on retail sales were ebullient.

Car Buyers, Online Shoppers Lifted U.S. Retail Sales in December

Spending at restaurants helped with 0.6% gain over holiday season

The text of their reporting was equally enthusiastic.

American consumers finished last year spending at a solid pace, splurging on cars and pouring money into online shopping during the holidays, a sign the economy is on a steady footing as the country prepares for a change in the presidency.

Sales at U.S. retailers rose 0.6% in December from a month earlier, the eighth monthly increase in nine months, helping to extend the economy’s long expansion. Retail sales rose 3.3% in all of 2016, faster than the prior year’s gain of 2.3% and similar to the underlying trend during the expansion.

The report went on to give the presumed reasons for the apparent rise.

Several trends are aligning to support spending. Worker wages have grown more quickly over the past year after a long period of stagnant growth, with average hourly earnings up 2.9% in December from a year earlier, Labor Department figures show. At the same time, living costs—particularly for everyday items such as gasoline—continue to grow modestly, giving people more money for shopping and travel.

Unfortunately, as usual, it missed the mark on factuality. The statement about wage growth is simply not correct.

Then there’s the issue of seasonal adjustment (SA).Like all mainstream outlets the Journal reports only the seasonally adjusted numbers. That number is an attempt to statistically manipulate the data to remove seasonal patterns. We have repeatedly seen how the SA data is often wide of the mark in representing the trend. The initial release often misrepresents the state of the trend entirely. That’s why the government repeatedly revises the data for the current month, not just over the next 2 months, but for 5 years after the fact. They continually fit the SA data to the actual data over time.

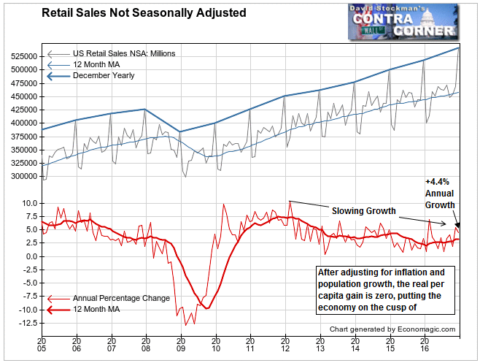

Here are the facts, using the actual, not seasonally adjusted data. We measure how the current period did by comparing the annual growth rate looking back a few months. We also use the current month to month change and compare that to recent past years. That shows us how the current month did relative to its usual monthly performance.

December nominal retail sales rose 15.5% from November. Obviously December is the biggest month for retail sales and always has a big jump versus November. In this case, the current December gain was below 2015’s, which had a gain of 16.6%. That suggests a bit of deceleration in the trend. However, the current monthly gain was near the average gain of 15.2% since the beginning of the recovery in December 2009. Is “average” any reason for the media’s enthusiasm?

The annual growth rate was 4.4%, including price increases ( inflation). Again, that was a little slower than November’s annual growth rate of 5.4%. It was slightly better than prior months. But it was well below the strongest growth of 2015 which occurred in February at +6.9%. And it continued a pattern of declining momentum in effect since 2012.

There’s scant evidence of significant weakening in the trend in 2016. But neither does the data suggest any improvement consistent with the Wall Street Journal’s cheerleading.

None of the reported data accounts for, or even mentions the inflation component. We have shown in other reports how the popular CPI measure understates actual consumer inflation. We can make a judgment on real sales using the Flyover CPI developed by David Stockman.

The Flyover CPI tells us that CPI has typically understated actual consumer inflation by approximately 1% per year in recent years. In both September and October the Flyover CPI showed inflation at 3.6%. CPI growth for those 2 months were reported at 1.5% and 1.6%, while November was at 1.7%.

The gap between the CPI fantasy and reality was even worse than usual in the past 3 months. That’s largely because CPI essentially ignores housing inflation, and underweights health care costs.

If we deflate nominal sales by the Flyover CPI, suddenly the reported gains look far less impressive. The real, inflation adjusted annual increase, is probably around +0.8%.

That’s virtually the same is US population growth. That means that on an inflation adjusted, per capita basis, retail sales have not increased one iota in the past 12 months. Any weakening from this point would suggest recession. It would take the media and the markets many months to figure that out.

Meanwhile, we’ll be on the lookout for it, and will be prepared to get the jump on the trend when it does reverse.