As I noted yesterday, the FOMC press conference on Wednesday made one thing abundantly clear; the Fed has lost control of the narrative and their credibility.

“The problem stems from the Fed’s ongoing adherence to “data dependency.” Last December, when the Fed Funds rate was increased, the Fed discussed the potential for further rate hikes in 2016 as inflation and employment data strengthened.

However, in March, with employment and inflationary data improving combined with a strong rebound in the financial markets, the Fed opted to ignore their data and focus on “global risks” to hold rates steady.

The problem for Ms. Yellen is while she was waiting to find the “perfect balance” of domestic growth and global stability, global economic weakness has now begun to destabilize domestic growth and employment.”

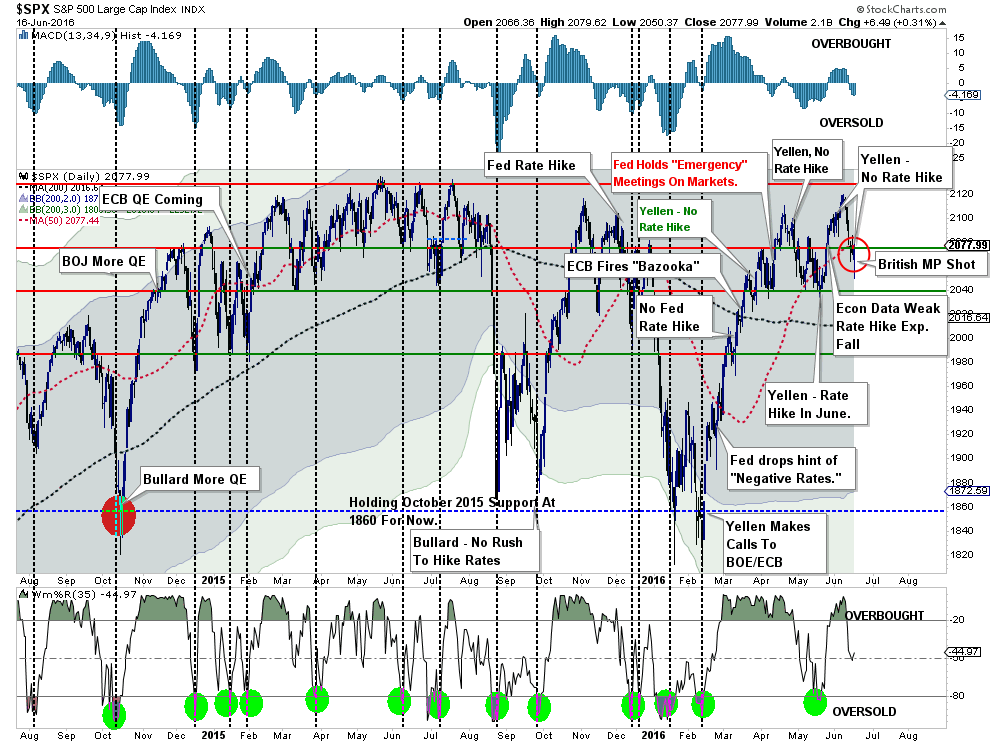

This point should not be taken lightly. In the past, the markets have responded positively to the idea the Fed would not be able to increase rates keeping monetary accommodation high. This time, Mr. Market was not so friendly and the markets were off 20 points yesterday morning approaching a retest of the 2040 support level.

The unfortunate assassination of British MP Jo Cox quickly reversed the sell-off yesterday as fears of a “Brexit” were temporarily suspended.

As I noted in the Technical Update, (click here to subscribe for free e-delivery) the 2040 support level is now critically important. A violation of that low would break very important support which would likely lead to a deeper market correction.

“This isn’t the time to be overly complacent, but it is also not the time to panic. Emotional decision making always leads to the worst outcomes. Maintain a focus on ‘what is’ rather that what you ‘hope’ it to be.”

Lastly, as an interesting side note, I have been writing for the last couple of years that economic growth has likely been overstated. The reason was quite simple, the underlying economic data did not support the BEA’s estimates of growth. Not surprisingly, the BEA has just announced they will trim 2% off of GDP next month.

“According to BEA’s newest data, real GDP was overstated by about $125 billion from 2007 through 2008, during the period leading into the start of the Great Recession. But the overstatement shrank to about $70 billion in 2009.

During 2012 and 2013, when the U.S. economy had what some have referred to as a micro-recession, the overstatement of real GDP growth ballooned to about $275 billion. Despite over $100 billion in revisions to real GDP growth in 2014 and 2015, the overstatement continued to grow to $324 billion, or 2 percent of GDP.”

Of course, this explains why many of the numbers just “didn’t add up.” Importantly, the current decline in corporate profits and collapse in return on equity suggest the current economic backdrop is far weaker than currently reported. Next year’s negative revisions to GDP will reveal this to be the case and that a recession will likely have started in the latter half of this year.

“What is behind me is not important.” – Michael Sarrazin, Gumball Rally

Here is your reading list for the weekend.

CENTRAL BANKING

- Vanity Of Central Bankers by Danielle DiMartino-Booth via Money Strong

- Janet Whiffs Again – Take Cover Now by David Stockman via ContraCorner

- The One Chart Showing How The Fed Lost by Tyler Durden via ZeroHedge

- Fed Eyes Lasting Impediments To Economic Growth by Sam Fleming via FT

- Quantitative Easing – Good, Bad & Ugly by Axel Merk, Merk Investments

- Consumer Goods Inflation vs. BLS vs Fed Fantasy by Lee Adler via ContraClub

- $12 Trillion In QE & Lowest Rates In 5000 Years by Jeff Cox via CNBC

- The Fed Reserve’s Second 100 Years by Alex J Pollock via AEI

- A Japan-Style Slump May Be Best-Case by Satyajit Das via Bloomberg

- Why The Fed Chickened Out…Again by John Crudele via NY Post

THE MARKET, ECONOMY & BONDS

- We’re Headed For 1938 Again by Bob Bryan via BI

- BEA To Revise Down GDP By 2% by Chriss Street via Breitbart

- Bonds Outside Norms Back 500 Years by Chris Ciovacco via Ciovacco Capital

- Too Many Stocks In Decline by Luke Kawa via Bloomberg

- Now Is Your Last Chance To Dump Bonds by Howard Gold via MarketWatch

- 10 Facts About US Economy by Heather Long via CNN Money

- 15-Facts Show US Economic Troubles by Michael Snyder via Economic Collapse

- Recession Concerns Growing Again by Joe Calhoun via Alhambra Partners

- Bond Market Sends A Warning by Michael Kahn via Barron’s

- Breakout In Bonds by Greg Harmon via Dragonfly Capital

- Why Soros Bet Not Far-Fetched by Mohamed El-Erian via Barron’s

- Smart Money Buying Bonds by Bryce Coward via GaveKal Capital

- Which Labor Market Data To Believe by Binyamin Appelbaum via Upshot

- 34-Year Tailwind For Stocks Is Over by Chuck Jones via Forbes

MUST WATCH VIDEO

John Oliver On Retirement Plans

INTERESTING READS

- Sherlock Holmes On Investing by Morgan Housel via Motley Fool

- Ignore The Hype, Few Shortages Of Skilled Workers by Fabius Maximus

- Businesses Running Out Of People To Hire? by Caroline Baum via MarketWatch

- Henry Kravis: Worry About The Downside by Jason Kelly via Bloomberg

- Just Not Adding Up by Eric Parnell via Seeking Alpha

- Asset Returns & Global Economy by Tiho via Short Side Of Long

- 6 Events Could Make Soros Bet A Winner by Mohamed El-Erian via Bloomberg

- Dead Companies Walking by Scott Fearon via Tumblr

- An Unprecedented Jump In The VIX by Dana Lyons via Tumblr

- Why Soros Is Bearish by Jesse Felder via The Felder Report

Questions, comments, suggestions – please email me.

Lance Roberts

Lance Roberts is a Chief Portfolio Strategist/Economist for Clarity Financial. He is also the host of “The Lance Roberts Show” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report”. Follow Lance on Facebook, Twitter, and Linked-In